Welcome to our weekend Technical Recap. Wayne takes a look at the market moves for the week as Friday’s turbulent session expressed a bit of a FOMO moment going into the closing bell. While the major averages came off of their lows around midday, they rallied mightily into the close and in earnest, it’s been a FOMO environment for much of the last 2 weeks. Why do we say this? The S&P 500 has been positive in the last hour of trading for 7 straight days. And that last half hour of trading with that big uplift in the major indices… Wayne discusses the element of short covering at play and what it could portend regarding the week ahead. Please click the link to review the Weekend Technical Recap .

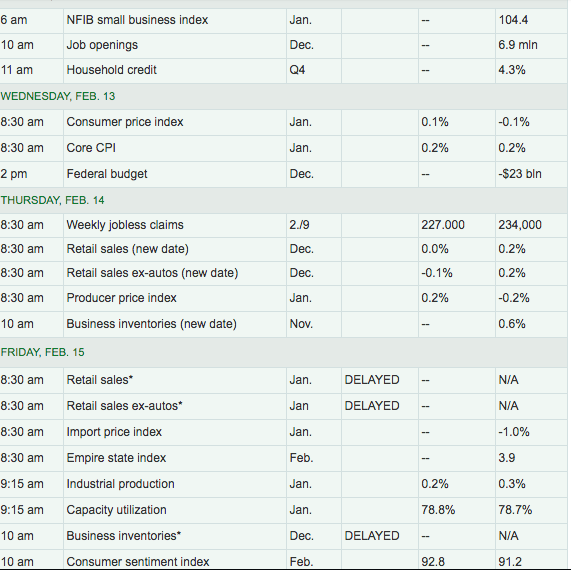

In terms of Finom Group’s fundamental market outlook, we encourage readers and followers to subscribe to our Weekly Research Report. Within this week’s report titled “S&P 500 Turned Away At Overhead Resistance: Macro-Mud Remains“, we discuss fund flows, the S&P 500 having been rejected near its 200-DMA and macro-fundamentals that includes everything in the geopolitical realm to corporate earnings. With that being said, the majority of the Industry Groups that make up the S&P have been struggling to retake their 200-DMAs. The chart below shows the historical percentage of Industry Groups above the 200-DMA on a daily basis going back to 2014. Back in early January, this reading cratered all the way down to 4.3% when the only group above its 200-DMA was Household and Personal Products. In the month since then, we have seen the percentage slowly climb higher.

While the percentage was close to 50% earlier this week, as the market has declined it also pulled back to the current level of 37.5%. In other words, the market still has a lot of work to do before this reading starts to look healthy again.

As we prepare to kick-off the trading week this Monday morning, equity futures are pointing to a positive open on Wall Street and on the heels of a strong return of trading in China. Having said that, the positive reflection for opening trade is also met with a more sanguine tone out of the International Monetary Fund on Sunday evening.

“The bottom-line — we see an economy that is growing more slowly than we had anticipated,” IMF Managing Director Christine Lagarde told the World Government Summit in Dubai.

Last month, the IMF lowered its global economic growth forecast for this year from 3.7% to 3.5 percent. Lagarde cited what she called “four clouds” as the main factors undermining the global economy and warned that a “storm” might strike.

The risks include “trade tensions and tariff escalations, financial tightening, uncertainty related to (the) Brexit outcome and spillover impact and an accelerated slowdown of the Chinese economy“, she said.

With U.S. trade delegates having wrapped-up talks with Chinese trade delegates in Washington in the previous week, they now head to China to continue with trade talks in an effort to strike a deal that would prove to lower the temperature on global trade protectionist activities. In speaking specifically on the trade feud and current stage of talks between the U.S. and China, Lagarde offered the following:

“We have no idea how it is going to pan out and what we know is that it is already beginning to have an effect on trade, on confidence and on markets,” she said.”

With respect to the week ahead, economic data will prove a plenty during the course of the trading week. Monthly retail sales and CPI will likely be keenly watched by investors who desire a better read on the state of the economy and consumer.

One aspect of market correlations that we continue to lend a watchful eye remains with the U.S. Dollar and how it relates to corporate results. Coming from a strong USD rally in the back half of 2018, we entered 2019 with a positive dip in the USD. We suggest the weakening of the USD to be a positive as it lends itself favorably to those 40% of corporate revenues that are achieved overseas. A stronger USD puts pressure on those revenues and thus pressures overall results. It should be noted, however, that in past cycles, corporate earnings negatively impacted by Forex headwinds have managed to be dismissed by investors who largely viewed the situation as transitory. Nonetheless, the early year dip in the USD has managed to find buyers as indicated in the chart below.

We largely blame the strength of the USD on weakening global growth, mainly the uncertainty surrounding the deceleration in economic activity within the Euro Zone and China regions. It would likely demand resolution on the trade front and Brexit to weaken the USD going forward, something that many analysts and strategists have pegged their respective USD forecast in 2019.

Tags: DXY SPX VIX SPY DJIA IWM QQQ TNX

{kind=link}