In our daily market dispatch Thursday, we discussed the bear vs. bull debate with a focus on the bear case delivered by Morgan Stanley. The firm’s chief market strategist has outlined its bearish case for a rolling bear market and offered the $1trn market cap achievement by Apple Inc. (AAPL) as highlighting the possible end of the bull market in the interim. Of course while Michael Wilson has issued his market forecast, the Morgan Stanley firm itself has raised its U.S. GDP forecast.

Wilson focused on the recent and possible peak in the Nasdaq within his weekly market notes, which we discussed in the article titled Market Debate Rises With Rates Rising & Tech Potentially Falling Out of Favor . Tech stocks have been leading the rebound in the broader S&P 500 index since the February market correction. The tech-heavy Nasdaq has achieved several new all-time highs along the way. Growth and momentum stocks are favored in a tightening rate environment despite the recent rotation into value stocks. Such rotation has been seen before, only to revert to the former trend. Nonetheless, Michael Wilson finds value orientation more favorable than tech/growth presently, even after the FANG reporting for Q2 projects strong earnings and the tech sector as a whole is expressing some of the strongest sector earnings growth. According to FactSet, the Information Technology sector is reporting the third highest (year-over-year) earnings growth of all eleven sectors at 31.7 percent. There is a great deal of earnings results-ignoring being displayed in Wilson’s market outlook, but to each his/her own as they say.

On Friday, investors will awaken to a negative outlook for trading with global equity markets largely in the red. U.S. equity futures are picking up where they left off Thursday with all three major indices in the red at the 6:00 a.m. EST hour. Not much has changed for the market outlook to express the selling pressure in the last couple of trading days on Wall Street other than the date on the calendar and a market rally that may simply be exhausted at the moment. Nonetheless, selling pressure has presented itself prior to the S&P 500 achieving a new all-time high, coming within 10 points of the previous high set back in January.

To end the trading week, the Consumer Price Index will be the main piece of economic data to be released at 8:30 a.m. EST. The CPI report is expected to show a monthly rise of 0.2%, but a hot number could present problems for the market. Having said that, Thursday’s release of the Producer Price Index was weaker than expected.

“Ian Lyngen, head of U.S. rates strategy at BMO Capital Markets, said the PPI report “takes the edge off any expectations for a strong CPI [consumer-price index report] tomorrow,” which could push yields higher.”

The market has anticipated higher inflation and rising yields for the fiscal year, and to some degree, the economy has expressed some level of increased inflation as yields have risen. The Fed is set to achieve its inflation target in 2018, but has also suggested it is willing to let inflation run a little hotter than 2% in order to achieve its symmetric goal of overall inflation. During a Thursday interview with reporters, Chicago Federal Reserve President Charles Evans implied that the central bank still expects inflation to hit the Fed’s annual target of 2% and possibly overshoot that level. He said policy makers aren’t fretting surpassing that target, describing it as “nothing to worry about.”

Switching our focus from the equity markets and the economic data for a moment, we want to refocus on Finom Group’s overall theme of covering the volatility complex. In our more recent reporting and daily recaps, Finom Group’s chief market strategist Seth Golden outlined his near term outlook for the VIX and VIX trading derivative complex. Golden denoted the slow and steady decay in the VIX has produced what it generally produces, some degree of mean reversion on the horizon. Within Finom Group’s weekly research report dated July 10,2018, Golden alerted subscribers to his outlook for the VIX as follows:

“We also foresee future bouts of volatility in the coming months that will plunge the VIX below 11% and take it above 22%, even if ever so briefly.

With one leg of Golden’s forecast coming to fruition in August, the upper end of his forecast may be forthcoming in the weeks or months to come. Having said that, Golden has also aligned the Golden Capital Portfolio to coincide with his VIX/market volatility outlook. In a recent tweet to Finom Group subscribers, Golden disseminated the reduced short-VOL exposure within the Golden Capital Portfolio as the VIX breached 11 percent, anticipating near term volatility elevating. (See screen shot from private twitter feed below)

Some of the variables that factored into Seth Golden’s forecast and decisions to reduce short-VOL exposures are noted below:

- The VIX and 20-day standard deviation was nearly 0.86. Standard deviation often declines substantially before nearly every major spike in volatility. This acts as a much better forecast of volatility spikes than other more popular techniques. For the 1st time in several months, dispersion in the VIX has declined quite a bit. The last time VIX dispersion was so low was from mid-December ’17 through mid-January ’18.

- The Daily Sentiment Index recently dip below 10, usually signaling a near term, temporary top in equities.

- SKEW recently broke above 150, something it has only done a handful of times, which has generally found a short term low in the VIX.

- The VIX 20-day buy-to-open (BTO) call/put ratio has been rising in recent weeks, and recently clocked in at 5.5, the highest since mid-July 2017.

- The VIX has historically popped a week after its 20-day BTO call/put ratio exceeds 5.5. According to data from Schaeffer’s Quantitative Analyst Chris Prybal, the VIX has averaged a one-week gain of 9.2%, and was higher 100% of the time after signals since 2010, of which there have been six.

- Likewise, the S&P 500 Index (SPX) tends to dip after the VIX 20-day BTO call/put ratio tops 5.5.

- The 30-day implied volatility skew on VIX options is now at an annual low, suggesting near-term puts have rarely been cheaper than calls in the past year.

- Keeping it more simple: A VIX below 12 is generally found for cheap insurance, as hedge funds look to hedge there long portfolio exposure.

So now we’ll return to the markets and equity strategists’ outlook. The buy-the-dip mentality is still in favor, as earnings growth remains strong. With that in mind, a near term market pullback on matters not impeding earnings growth may continue to find dip buyers. Where some market strategists and pundits like Morgan Stanley’s Michael Wilson may be found wanting is with respect to earnings growth, coupled with the buy-the-dip mentality. Additionally, corporate buybacks are providing a floor for equities even as mutual funds have been net sellers of equities in 2018. Furthermore, one of the reasons Goldman Sachs stands in sharp contrast with Michael Wilson is partly due to central bank equity buying activities.

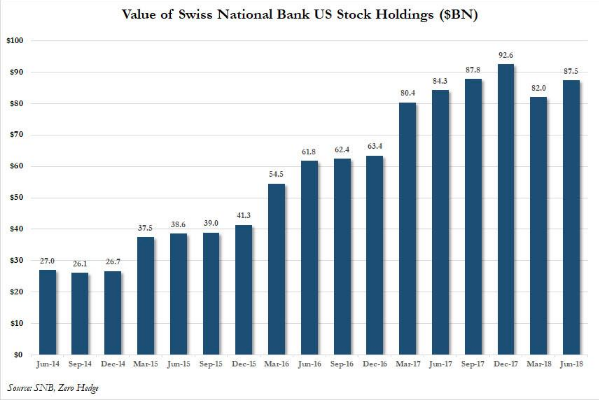

Although most central banks around the globe are draining liquidity from the equity marketplace, some are big buyers of U.S. equities. The most prevalent buying has been coming from the Suisse National Bank. The SNB just released 13F .

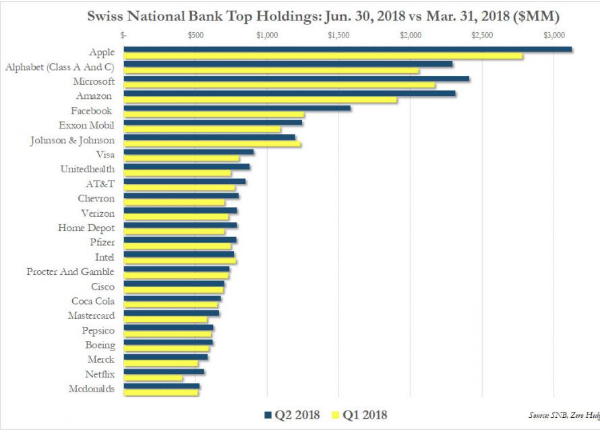

What it shows is that the Swiss central bank went on another aggressive buying spree and following a modest selloff in the first quarter. The Swiss central bank boosted its total holdings of US stocks to $87.5 billion, up 6.6% or $5.4 billion from the $82.0 billion at the end of the first quarter. Some of the largest holdings from the SNB are in the tech sector as shown below.

Goldman Sachs remains bullish on tech stocks and the Nasdaq and why wouldn’t they? With the SNB proving a massive dip buyer of U.S. tech stocks and the FANG names still providing strong growth forecasts, the fundamentals are favorable according to Goldman Sachs.

With global equities sharply negative ahead of the open on Wall Street and a key piece of economic data, the Turkish Lira plunging is stealing headlines from a strong earnings picture in the United States. So be it! After all, bears and bulls alike need to eat.

Tags: AAPL AMZN SPX VIX SPY DJIA IWM QQQ SVXY TLT TNX TVIX UVXY VMIN VXX

{kind=link}