All three major averages fell in the Thursday trading session as bond yields were on the rise. The 10-year Treasury yield trended higher and tipped over 2.92% in yesterday’s trading session, which stirred up anxiety amongst investors once again. The Dow Jones Industrial Average fell 0.3% to 24,665.89. The S&P 500 lost 0.6% to 2,693.13. Both held just above their 50-day moving average despite dipping below it during the trading day. The Nasdaq Composite Index fell 0.8% to 7,238.06. Helping stocks in the final hour of trading was a Bloomberg News report citing that Deputy Attorney General Rosenstein told President Donald Trump that he wasn’t a target of special counsel Robert Mueller’s probe.

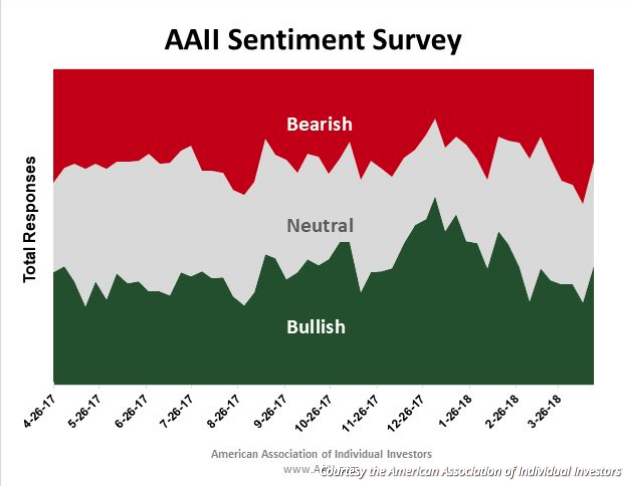

Although the month of April is finding equities moving higher thus far, it would appear that the tug-of-war between equities and bonds will persist through much of 2018. But investor sentiment is improving from a relatively low base in February and March of this year. The percentage of investors optimistic about the U.S. stock market jumped in the latest week. According to the AAII Sentiment Survey, 37.8% of investors describe themselves as bullish, meaning they expect prices will be higher six months in the future. The reading represents an eight-week high, and growth of 11.7% from the previous week. The reading is still below the long-term average of 38.5 percent.

Pessimism fell by 13.5% to 29.2% in the latest week, dropping below its long-term average of 30.5% for the first time in four weeks. Last week, the ratio of bears hit its highest level since March 2017.

Despite a strong start to the earnings season, it seems as though equities have been stuck in a rather wide trading range between the February lows and the more recent highs of mid-March. When we look at the financial sector, which kicked off earnings seasons strongly, we come to recognize that the financials sector has seen 28% blended earnings growth this quarter. Even with this strong performance most reporting bank stocks have fallen upon delivering strong earnings and revenue results. Moreover, even the financial sector Financials XLF ETF has dropped 1.5% during this reporting period and since last week. Having said that, the XLF did bounce back a little bit in yesterday’s trading session. Finom Group’s Chief Market Strategist Seth Golden believes the XLF will trend higher through April.

With regards to the Q1 2018 earnings season, we still have a long way to go and with many reports pending. As of 4/19/18 just 10% of S&P 500 companies have released reports and of those, 79% have reported profit above consensus and 12% below, according to Thomson Reuters estimates. The tech sector will begin to deliver earnings results in the coming weeks, which could tip equities in one direction or the other.

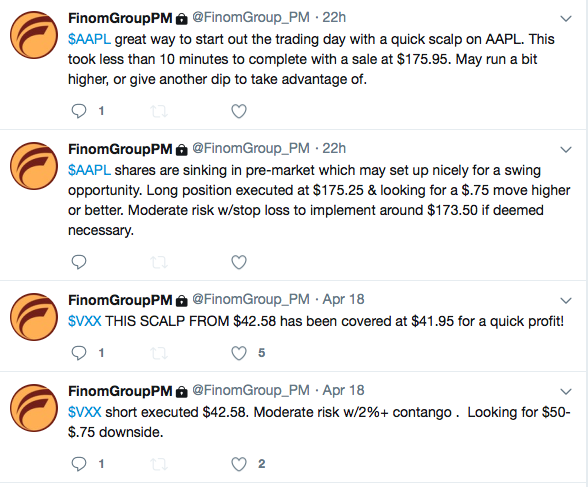

U.S. equity futures are broadly lower on Friday, following a risk-off trading session on Thursday and with most Asian markets closing lower overnight. Regardless of market conditions and/or sentiment, there is generally a trading opportunity to be found. In yesterday’s trading session, Apple Inc. (AAPL) shares came under sharp pressure. A miss and dim guidance from Taiwan Semiconductor, which pointed to a “very high-end smartphone” as part of demand softness, found shares of AAPL under pressure throughout the trading session and as other chipmakers moved lower. Taiwan Semiconductor manufacturers chips for companies like Apple and NVIDIA Corporation and said it’s facing “weak demand” from mobile customers, CNBC reported. The company guided its revenue for the second quarter to a range of $7.8 to $7.9 billion, which is short of Wall Street’s estimate of $8.8 billion. In light of this guidance from Taiwan Semiconductor, AAPL shares began falling in the pre-market yesterday. Finom Group’s Seth Golden issued a scalp trade alert as depicted below:

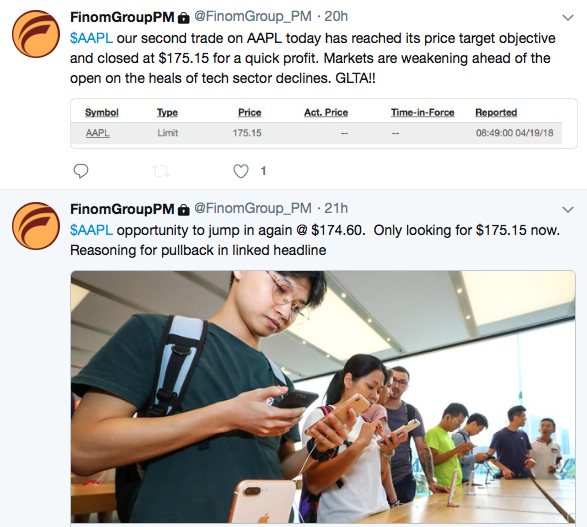

With this trade alert completed for a profit, shares of AAPL continued to fall in price. But for every further dip in price, buyers did indeed come in, even if to only momentarily lift the share price. For this reason, another trade alert was issued as depicted below:

Both trades worked out well for Finom Group participating subscribers who access our private twitter feed , but shares of AAPL didn’t perform as well and closed near the lows of the trading day. Shares of AAPL remain under pressure in the premarket Friday. Investors have seen such headlines concerning the demand for iPhones in the past. To date, none of the previous concerns were found relevant and/or accurate. We’ll have to wait and see if “this time is different” as they say. In the meantime, subscribe to finomgroup.com today and access our trade alerts in real time.

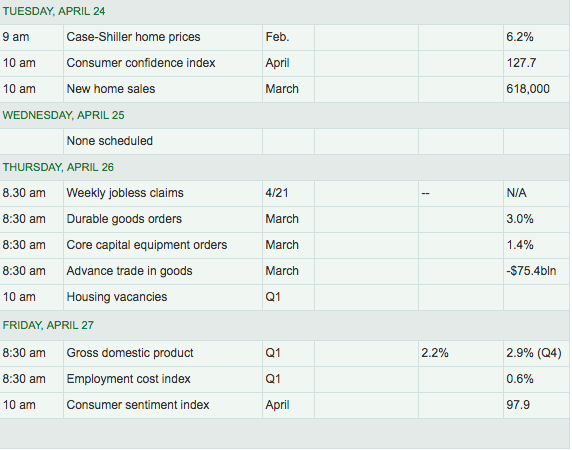

Friday comes without any significant economic data, but with equities in need of some catalyst to move higher. GE, Honeywell, SunTrust Banks, Inc., State Street Corp. and Schlumberger are all expected to report earnings ahead of the open, but none are expected to be such a catalyst for equities on the whole. As such, when we look out to next week’s slate of economic data we come to find a big piece of the state of the economy will be revealed through a reading on Gross Domestic Product (GDP).

Dribs and drabs of housing market data will proliferate throughout the week, but the headline will likely prove to come from next Friday’s GDP reading. The reading is expected to be soft, with respect to Q4 2017 GDP results. Economists polled by Factset anticipate a Q1 2018 GDP reading of 2.2% given the slow start to the year and delayed affects from the tax reform bill and tax refunds.

And with that, have a great trading day, exercising strong disciplines in a market that will eventually sort out the dichotomy between equity valuations and higher rates, relatively speaking…