Were you paying attention to the headlines in the after hours trading session on Wednesday? If the answer is no, you’re probably no worse off and as multiple, conflicting trade headlines proliferated across media outlets. Dow Jones equity futures fell some 300 points Wednesday evening as a report via the South China Morning Post revealed that the U,S. and China made no progress on key trade issues in two days of deputy-level talks, according to sources. What was worse, as the report notes, “the high-level talks are expected to last for only one day, with Liu He and his team now planning to leave Washington on Thursday.” This negative sentiment was later reversed. Read on…

High-level trade talks start officially today: China’s Vice Premier Liu He will be leading the Chinese delegation. Ahead of the report by the SCMP, there had been tentative evidence that China was willing to make a partial deal that would include buying more agricultural products, although leaving no room for negotiation in other sensitive issues.

About a half hour after the initial SCMP headlines broke, the White House pushed back on its reporting, suggesting it was a false narrative as outlined in the following tweet by a CNBC reporter:

Later Wednesday night, according to Bloomberg, the White House was reportedly looking at rolling out a previously agreed currency pact with China as part of an early partial deal that could also see a tariff increase next week suspended. The currency accord, which the U.S. said had been agreed to earlier this year before trade talks broke down, would be part of what the White House considers to be a first-phase agreement with Beijing. It would be followed by more negotiations on core issues like intellectual property and forced technology transfers, the people said.

Separately, the New York Times reported Wednesday night that President Donald Trump had green-lighted issuing licenses to some U.S. companies to conduct business with Chinese telecom giant Huawei Technologies. The U.S. blacklisted Huawei earlier this year, and allowing sales of non-sensitive products could help defuse trade tensions.

From Dow equity futures falling some 300 points late evening Wednesday to Thursday early morning down only 20 points; it has been a wild and hairy ride over the last 12 hours. The one thing investors know for certain, regarding trade, is that nothing is for certain. Goldman Sachs, after all the mixed signals on trade, offers the following assumption:

“Despite mixed trade policy headlines in recent days, a delay in the tariff increase planned for October 15 still looks slightly more likely than on-schedule implementation, in our view. While the obstacles to a major agreement are significant, Chinese purchases of US agricultural products, along with a few additional policy changes, appear sufficient to lead the White House to delay the tariff increase.”

It was only Wednesday morning that China officials confirmed that they were narrowing their focus for a trade deal of sorts, but still negotiating in earnest and with optimism. That sentiment found equity markets in rally mode ahead of the Fed meeting minutes release. When it was all said and done for the Wednesday trading day on Wall Street, the S&P 500 finished higher by roughly .9% on very light Holiday volume. Yom Kipor is highly followed Jewish holiday for Wall Street participants.

There is a trader’s adage, “Sell Rosh Hashanah, Buy Yom Kippur”. Many in the Wall Street community are Jewish, staying out of the stock market during the Jewish high holidays may make some sense. Jewish traders and investors wind down at rosh Hashanah, the Jewish New Year, and return after Yom Kippur, the Day of Atonement, which was yesterday.

Indeed, this year’s market weakness began just around Rosh Hashanah. Moreover, the market’s decline was halted yesterday right at trend line support, and rallied today.

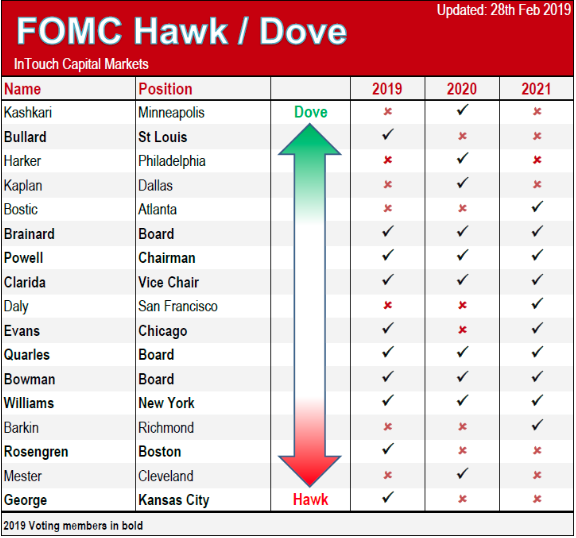

The Fed’s latest meeting minutes were released on Wednesday and they suggested a varied view on rate cuts going forward. The “dot plot” of member expectations released at the meeting showed that five members favored the Fed not approving any additional cuts this year after the most recent move, five more seeing an increase ahead, and seven wanting an additional cut.

The final tally among the 10 voting members saw three dissents from Fed presidents, Eric Rosengren of Boston and Esther George of Kansas City, who favored holding the line, and James Bullard of St. Louis who wanted a half-point cut. That marked the most dissenters since December 2014. Since then, however, Eric Rosendgren has stated he was open-minded about what he would advocate at the meeting. He said he would be focusing on data about consumers. George also seemed a bit more amenable to a future rate cut in recent statements: “Should incoming data point to a broadly weaker economy, adjusting policy may be appropriate to achieve the Federal Reserve’s mandates for maximum sustainable employment and stable prices.”

In justifying the former cut in the latest Fed minutes, Fed officials cited concerns over slowing global growth spilling into the U.S., the ramifications from the U.S-China trade war, and persistently low inflation that had been running below the Fed’s 2% target.

Members said that while they saw U.S. growth as generally solid, the forecast risks “were tilted to the downside.”

“Important factors in that assessment were that international trade tensions and foreign economic developments seemed more likely to move in directions that could have significant negative effects on the U.S. economy than to resolve more favorably than assumed,” the minutes said.

“In addition, softness in business investment and manufacturing so far this year was seen as pointing to the possibility of a more substantial slowing in economic growth than the staff projected. The risks to the inflation projection were also viewed as having a downward skew, in part because of the downside risks to the forecast for economic activity.”

Shortly after the Fed minutes were released, Citigroup offered there take on the minutes and expectations going forward:

- We expect a rate cut from the Fed this month

- Then probably at least one more cut in December … or later

- Fed outlook is not a major headwind for the USD

- The Fed will continue to react to incrementally weak data

On Wednesday, the latest Job Opening and Labor Turnover (JOLT survey) data was released. This index usually doesn’t capture a great deal of attention, but with the current expansion cycle being the longest in history, the labor market has increasingly come into focus amongst economists and investors alike.

The number of job openings nationwide fell in August for the third straight month and hit a one-and-a-half-year low, coinciding with a decline in hiring that’s taken place against the backdrop of a slowing U.S. economy. Job openings slipped to 7.05 million in August from 7.17 million in the prior month. The number of job openings has gradually declined since hitting an all-time high of 7.63 million at the start of 2019

Openings fell the most in manufacturing and information services such as media and public relations, the Labor Department said Wednesday. The share of people who left jobs on their own, known as the quits rate, slipped to 2.6% in August from 2.7% among private-sector employees.

At present, it’s really hard to rationalize that the U.S. economy can produce recession while job openings are still near cyclical highs. Nonetheless, this is the question Logan Hohtashami asked in a recent blog post. “Can the U.S. really have a job loss recession while openings are still way above hires? We didn’t have this happen in the previous cycle, no matter how tight the labor market got, and we didn’t have this happen earlier in this cycle when jobs were growing.“

“In theory, job openings have to go a lot lower before we really can wave a red flag here. It has to get to a level that we saw earlier in this expansion. Or maybe this time it’s different, perhaps you can have a job loss recession with elevated levels of openings? For me to really believe that I need to see the evidence, hence why I am trying to bring this up right now.”

Finom Group is of the opinion the latest JOLT survey shows undeniable slowing, but from cyclical highs and in a range that is still supportive of trend-growth GDP. The data set would need to weaken much more and into 2020 before it and other labor & employment data sent warning signals about a more imminent recession. When speaking in terms of foreshadowing a recession from any individual metric, it should be recognized that most economists won’t recognize a recession until after it’s already taken place.

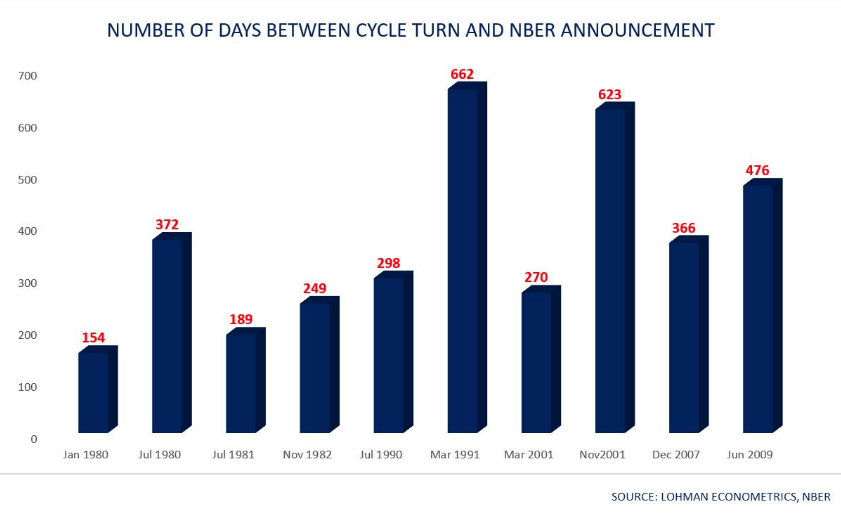

The National Bureau of Economic Research(NBER) is the private, nonprofit, nonpartisan organization charged with determining economic recessions. At present, there are likely many bearish investors claiming that the economy is already in a recession. They support this by claiming that the NBER is late to announcing recessions. We can’t deny this assertion. In fact, by the time most investors realize the economy is in a recession, it’s probably time to start buying and not the time to be selling. The NBER usually doesn’t recognize recessions until most traders have already sold.

According to the following chart that tracks NBER’s recession declarations, it took 366 days from the start of the last recession for the NBER to recognize the recession. If it wasn’t a long recession, it would have been over by then.

The chart also shows that it takes a long time for announcements that a new expansion has started.

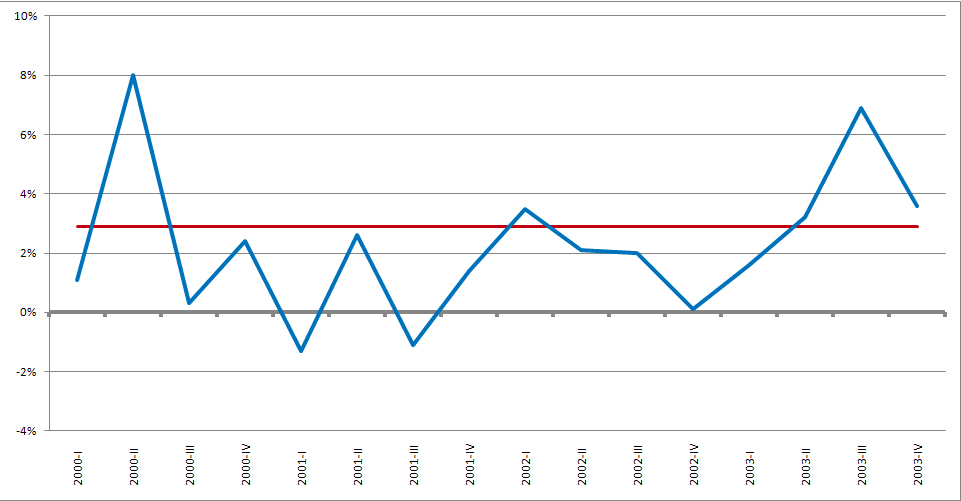

While there is no debating the 2008 recession that was a result of the Great Financial Crises, many economists and market participants have pushed back on the NBER’s classification of 2001 as a recession. According to the (NBER), the U.S. economy was in recession from March 2001 to November 2001, a period of eight months at the beginning of President George W. Bush’s term of office. However, economic conditions did not satisfy the common shorthand definition of recession, which is “a fall of a country’s real gross domestic product in two or more successive quarters”, and has led to some confusion about the procedure for determining the starting and ending dates of a recession. (Chart below of GDP from 2001-2002)

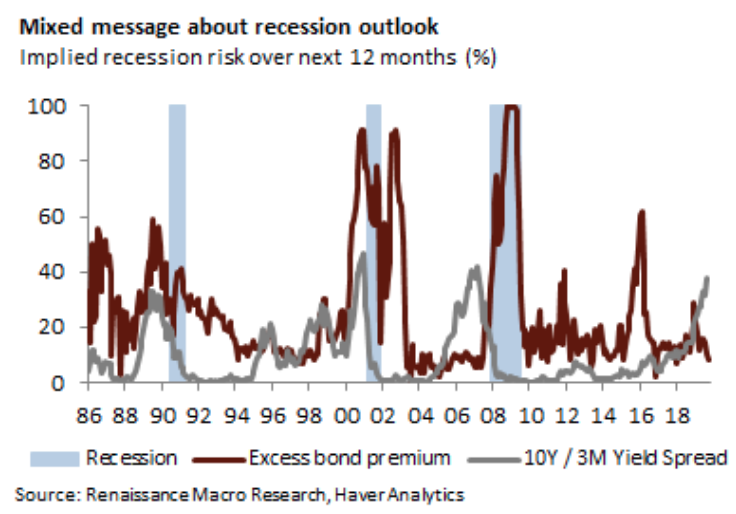

Moreover, while the Treasury market is sending a recession signal for the next 12 months, corporate credit is saying something quite different. In September, the excess bond premium, a measure of risk taking in corporate credit, implies less than a 10% chance of recession in 12 months.

Focusing our attention on the markets once again, we would suggest that yesterday’s price action was perfect, absolutely perfect. What do we mean by that, once again? As noted in a chart of the S&P 500 in our daily article on Wednesday we offered the 100-DMA resided at the 2,929 level.

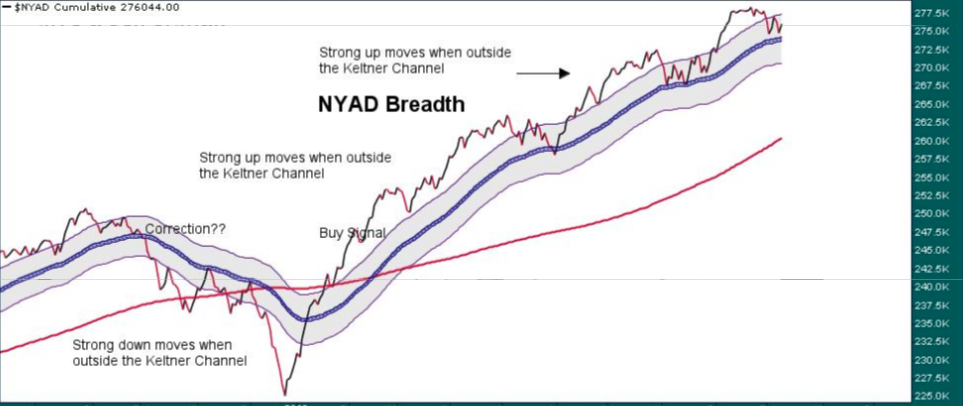

So what was the peak in the S&P 500 on Wednesday… 2,929. After achieving this feat of strength, the benchmark index was hit by headline driven algorithms that sent the index lower, but stabilizing into the closing bell. As one can see in the S&P 500 chart above, there is a good deal of Moving Average compression taking place. The strongest market moves usually occur when prices move above the compressed Moving Averages. Additionally, what we are looking at in terms of resistance is the area at 2,943, right around the 50-DMA. This really isn’t the best time to be allocating capital given the Moving Average compression and trade headlines proliferating and delivering much volatility. Having said that, we can’t deny that the NYSE A/D line is still supportive of a move higher in the S&P 500 in the interim. (Chart from David Larew)

While the NYAD chart offsets some of our concerns regarding the compressed Moving Averages of late, one chart elevates concerns for the broader market. Take a look at the VALUEG chart below. What’s the VALEUG, you might be asking?

“The Value Line Geometric Composite is an equally weighted index of about 1700 stocks. It uses a geometric average, so the daily change reflects the median stock price change. Some argue that it provides a broader and more accurate representation of the market than popular benchmarks like the S&P 500. As you can see from the chart, VALUG has been diverging from the S&P 500 as it puts in a series of lower-highs while the S&P 500 makes a series of higher-highs. This is one development that many technicians have been pointing to as a potential warning sign for the market.”

Given all the aforementioned technicals, however, the technicals are not likely going to drive the market going forward, as trade talks resume Thursday. Headlines from the fundamental trade talks will drive market activity. Expect volatility and be prepared to find headlines whipsawing markets. Regardless of the market movement, Finom Group continues to deliver winning trades to our Premium Members. Check out our latest trade below:

Finom Group continues to beneficially aid traders with a 99% trade alert hit rate in 2019.

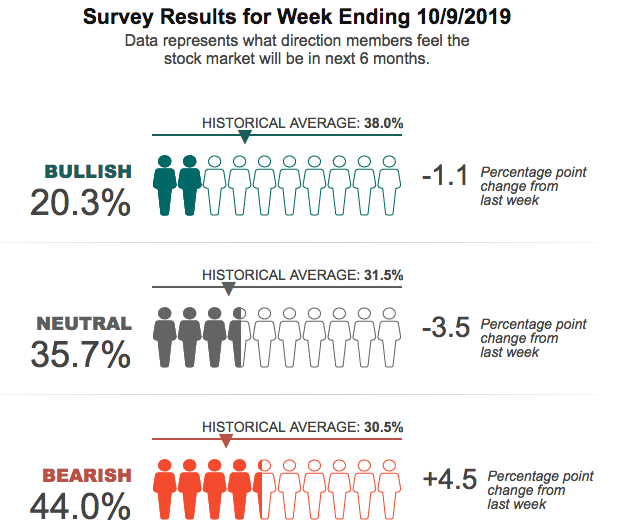

Heading into the trading day Thursday, inflation and employment data will highlight the economic calendar with CPI and Initial Jobless Claims. Neither are expected to be market moving, unless jobless claims jump mightily. Also Thursday, investors will awaken to yet another gauge of investor sentiment, which came in showing increased bearishness amongst individual investors.

According to the latest AAII survey, optimism among individual investors about the short-term direction of the stock market is at a 10-month low. Bullish sentiment, expectations that stock prices will rise over the next six months, plunged 8.0 percentage points to 21.4%. Optimism was last lower on December 12, 2018 (20.9%). Bullish sentiment is below its historical average of 38.0% for the 32nd time this year and the 20th time in 21 weeks.

Neutral sentiment, expectations that stock prices will stay essentially unchanged over the next six months, rose 1.8 percentage points to 39.2%. Neutral sentiment was last at this level on May 22, 2019. This was the fifth consecutive weekly increase. The rise keeps neutral sentiment above its historical average of 31.5% for the 19th time in 20 weeks.

Bearish sentiment, expectations that stock prices will fall over the next six months, jumped by 6.2 percentage points to 39.4%. Pessimism remains above its historical average of 30.5% for the ninth time in 11 weeks.

Bullish sentiment is back at an unusually low level for the first time in five weeks. Historically, such readings have been followed by higher-than-average and higher-than-median six- and 12-month S&P 500 index returns. This week’s drop in bullish sentiment follows the return of downside volatility to the stock market and weaker-than-expected economic reports.

Many individual investors have been monitoring trade negotiations, particularly between the U.S. and China. Also having an influence on sentiment are Washington politics, geopolitics, valuations, corporate earnings, monetary policy and interest rates.

This week’s special question asked AAII members how they expect the U.S. economy will perform over the next six to 12 months. Approximately 46% of responses we received say they believe the U.S. economy will weaken over the next six to 12 months. Many respondents cite trade issues for the expected downturn, while others expect political turmoil to negatively impact the economy. On the other hand, 31% of respondents say that they expect the economy to perform moderately well, with expected growth to remain positive but not as high as in previous years. Additionally, 23% say that they believe the U.S. economy will remain flat over the next six to 12 months as the Federal Reserve continues to adjust monetary policy.

Here is a sampling of the responses:

- “Poorly. As tariffs affect China, the world economy will suffer greatly. Our economy is part of the world and is already showing many signs of distress.”

- “It will trend downward due to all the trade disputes and reduced economic activities.”

- “Growth and inflation as measured by the government will both slow but no recession … yet.”

- “I suspect the economy to continue to grow at a 2.0% to 2.5% pace. Solid, but not fast, and not even close to the best economic growth that we have had in the past.”

- “I believe the economy will hold steady as interest rates decline.”

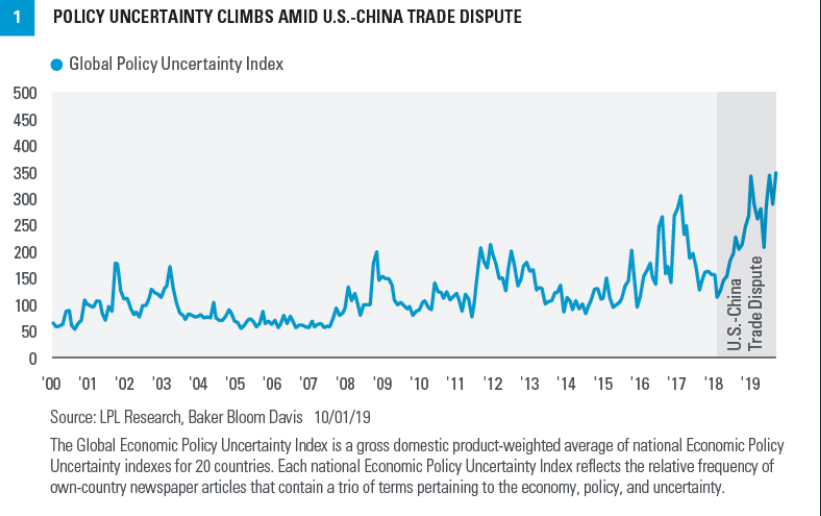

In many ways, there is a bull market in “unncertainty”.

There remains a great deal of uncertainty amongst investors and with regards to economic policy. Trade talk conclusions will go a long way toward removing the uncertainty one way or another, for better or for worse. In the latest LPL podcast, Ryan Detrick discuss economic uncertainty amongst investors and how this might be resolved.

{kind=link}

Hi Seth,

I have a couple of questions on the ISM PMI that came out last week

If c70% of US GDP is generated by the service sector, why do economists and traders focus on the Manufacturing PMI instead of the non-manufacturing? If the US is a service-led economy, then we should focus on that report. Is it to do that Manufacturing is more of a leading indicator than Non-manufacturing, which is more stable.

It sounds like the MarkIT Manufactorigin PMI has some advantages over ISM due to its larger sample size and overweighting key areas. I’m interested to understand why this report does not take equal prominence as ISM. Is it just the report is not as well known.