Monday markets proved to pick up right where Friday left off with a continued surge in stock prices. The rally didn’t show itself in the safe way that the majority of the relief rally since March 24th though. No, on Monday breadth was strong, tech did not lead, small-caps outperformed and the Equal-Weight S&P 500 (RSP) outperfromed the Cap-Weight S&P 500 (SPX/SPY). (Chart SPX/RSP)

While this seems a positive development, given FANG stocks were all red on the day and tech lagged, by and large, the hand-off to other sectors outperforming tech and small caps playing catch-up may simply prove that the rally is coming to an end with sector rotation headlining the advance. As an investor with very little to grasp hold of in the way of correlating/rationalizing the sizable rally off the March 23rd lows other than historical analogues, the latest surge in stocks has me raising the warning flags.

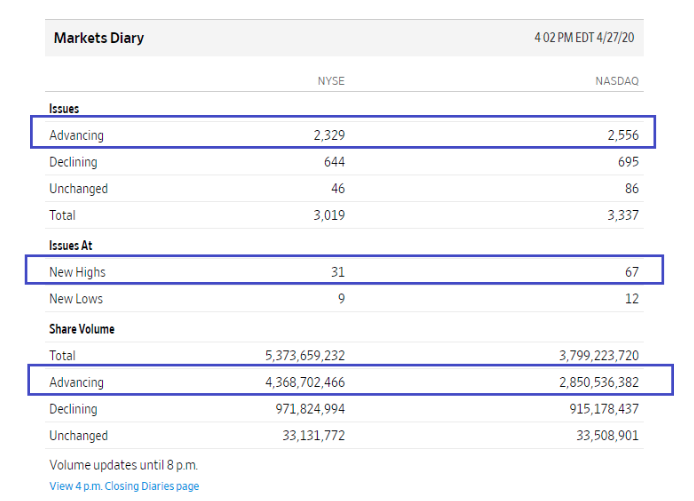

As noted above, breadth was strong and we’ve been expressing a desire to see improving breadth and especially participation from small caps, but this coming to fruition with the mega-cap FANG stocks faltering is not what I had in mind. Having said all of that, yesterday HAPPENED in the same way technical and breadth analysis always HAPPENED. Sometimes technical analysis should be realized for the art of playing “Monday morning quarterback”! We’re looking back at what already HAPPENED, which doesn’t guarantee what will happen going forward or how it will happen. It’s why I personally prefer fundamental analysis and long-term thesis building exercises for determining capital allocation. Nonetheless, here’s yesterday’s strong breadth in one table from the NYSE advancers vs. decliners, identifying market breadth on Monday.

Almost a 4:1 ratio on the A/D right, should be a net positive right? Again, it’s not hard to look at this particular breadth reading and answer yes. But man-alive there are so many different breadth metrics/market internals it cam make your head spin to analyze each one daily. It’s far easier to say, “This looks good”, and move on to price being truth! And it is after all: Price is truth, it’s not fake news whether one likes it or not. Price, like technical analysis, HAPPENED!

“But but but but wait it gets worse”! That’s one of my favorite verses from an old school rap song I loved in high school, called Slam, by the group Onyx!

And what, what, what got worse? Well, in terms of breadth not only did the NYSE A/D prove strong, really strong, but we know why it was strong. The mechanics of the market can be quite difficult to comprehend, but incredibly relevant when it comes to understanding price movement. Recall that on Friday of last week the gamma flip zone was 2,814 on the S&P 500.

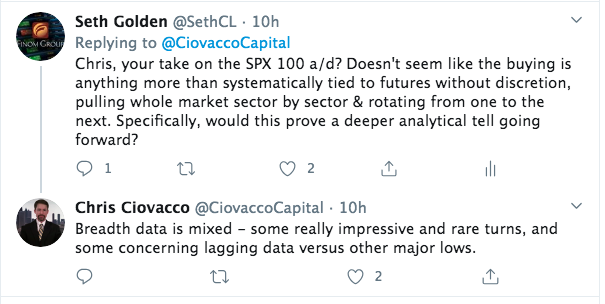

A close above this level, and we did, would potentially add to dealer delta hedging stress and find dealers buying long SPX futures. Buy long S&P 500 futures and you can also pull upward sectors within the S&P 500, by and large. How large? Well, for this we can see it through the lens of the S&P 100 breadth on the day. Through the S&P 100, we can determine market correlation levels and what was being bought! (TOS TheoTrade)

The screenshot above of the S&P 100 identifies the advancers vs. decliners at 87-13. Through the trading session it had been upwards of 94-6. In other words, “BUY EVERYTHING”! In a healthy market, a healthy economy we’d be perfectly fine with seeing this type of breadth in both the NYSE A/D and S&P 100, but in the current situations, the lack of discerning breadth identifies statistical arbitrage at works in the market whereby the moves are more mechanically aligned than a true gauge of risk appetite.

I often engage other popular intelligent investors on Twitter to gauge their thoughts on much of what I outline here for Finom Group readers and subscribers, hoping to learn something new or receive opposing perspective. As such, I engaged Chris Ciovacco with a question seeing how he generously disclosed the NYSE A/D statistical data from Monday. (See tweets below)

And there you have it. Nonetheless I would encourage investors to remember 3 things:

- Markets’ structural composition matters and, as we know, a handful of stocks can pull the whole of the market higher and lower because the S&P 500 itself is based on market cap-weightings.

- Price is truth and your welcome to fight the truth to your heart’s desire, but that’s never proven a good long-term strategy, given the power of structural composition.

- Fighting price is one thing, but fighting price with supportive monetary and fiscal policy is the equivalent of portfolio suicide. If not immediately, the poor discipline will certainly catch up with the investor.

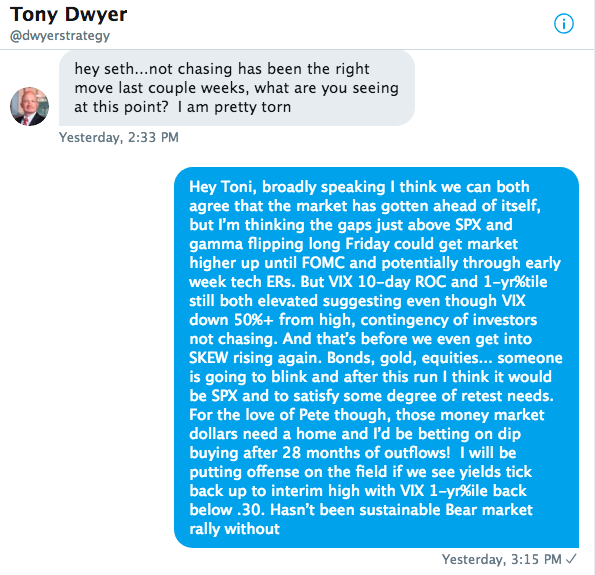

What I’ve already written may seem bearish; I get it! But, casting aside of the sentiment characterization and focus on the facts. It’s not like this Monday market move that is seemingly carrying over to Tuesday’s trading session wasn’t “expected”. In a conversation with Canaccord Genuity’s chief market strategist Tony Dwyer on Sunday, I shared my week-to-come outlook.

And seriously speaking of those money market flows folks… What are you paying these fund managers for if they aren’t doing much more than under-weighting the S&P 500 and over-weighting cash through money market, low interest funds? Nowadays, fund managing is more an art of asset gathering than actually managing the assets for greater yields as much of the assets gather simply finds its way into money market funds. You don’t have to pay a fund manager a commission for this transaction you know. You can go to your bank and do it yourself. Such a grotesque industry I tell ya!

Look, I’m not blinded by market truths and with extremely low market liquidity and more positive than negative headlines of late on the COVID-19 front, it’s quite easy to exacerbate a market move/trend, which is what we’ve seen. Does this mean you go chasing the market because of this truism and structure of markets? To answer that question I’d offer a resounding NO! Discipline wins out almost all the time! The market will and always does correct for time and/or price. Yet another truism of markets. As such, patient investors whom express sound disciplines will be reward in due time and eventually price. And then there are those investors, fund managers who choose to fight, position themselves contrary to the market price trend. One such fund manager choosing to fight the market is DoubleLine Capital’s Geffrey Gundalch.

“I’m certainly in the camp that we are not out of the woods. I think a retest of the low is very plausible,” Gundlach said on CNBC’s “Halftime Report.” “I think we’d take out the low.”

“People don’t understand the magnitude of … the social unease at least that’s going to happen when … 26 million-plus people have lost their job. We’ve lost every single job that we created since the bottom in 2009.“

The so-called bond king revealed he just initiated a short position against the stock market.

“Actually I did just put a short on the S&P at 2,863. At this level, I think the upside and downside is very poor. I don’t think it could make it to 3,000, but it could. I think downside easily to the lows or beyond … I’m not nearly where I was in February when I was very, very short.”

I’m not disagreeing with Gundlach’s sentiment or positioning here in this narrative. The risk reward on a fundamental basis does seem skewed to the downside and the upside does seem quite limited… on a fundamental basis. But as noted before, the structural aspects of markets can prove a daunting challenge for contrarian positioning. From technical perspective, the near-term outlook remains as I offered to Tony Dwyer in our Sunday conversation. The emphasis for a continuation of the technical and structural relief rally were also offered in our Weekly Research Report for Finom Group subscribers as follows:

Relative strength remains above 50, even though breadth is rather weak underneath the hood of the S&P 500. The S&P 500 Index rally has been driven by:

- A massive policy response

- Modestly better hospitalization and new cases numbers in many of the hardest-hit areas of the country

- Hope for potential treatments

- The reality that many of the large market-capitalization companies are reasonably well positioned for the current environment. Many of the mega-cap companies that led the rally are the same handful of companies that produced roughly 20% of the earnings of the S&P 500 Index in the fourth quarter of 2019.

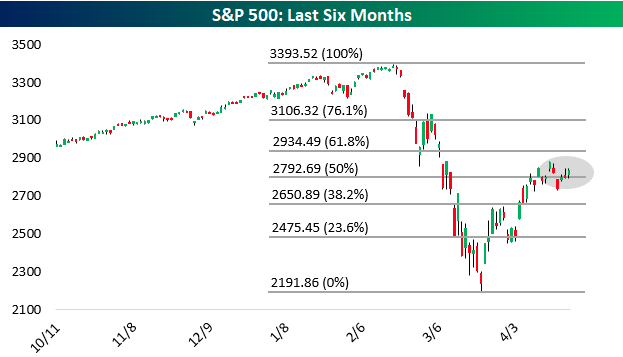

Tech earnings will need to instill confidence in investors this coming week to sustain the, now 4-week long, relief rally. Heading into the trading week, the level for the bulls to achieve is firstly going to be an algo-charged round number of 2,900. Why not 2,850? Well, remember that the VIX at ~36 signals a daily S&P 500 move of nearly 2 percent (each 16 percentage points in VIX equals 1% move in S&P 500), which from present levels means the S&P 500 is traveling above 2,850 or below 2,800 near-term. So if the 2,900 level is achieved, that would mean a scramble for the bears also.

More than likely and beyond 2,900, the next key achievement for the bulls is going to be the 61.8% fibonacci retracement level that lie ahead at 2,934.”

I would also add to this issued technical outlook for the week that the FOMC meeting on Wednesday may prove an inflection point for markets if 2,933 isn’t achieved by the scheduled press conference ahead of time. Outlooks are just that, outlooks, and not guarantees!

The market can be a confusing place for many would-be traders and investors. It’s easy to understand why most tax-paying citizens don’t invest at all, but rather take the whole of their paycheck home for living and leisure expenses. We can point to the present day and lay claim to the worst domestic recession in the modern era and since the Great Depression of the late 1920’s and early 1930’s. Yet still the market has climbed roughly 30% off the initial lows with most corporations pulling forward-looking guidance, earnings misses more significant than I can remember over the last 20 years and an economy basically “shut-in” while crude oil futures prices drop to record lows and turned negative. I can understand how the variables mentioned don’t necessarily align. But, we can’t forget or deny ourselves of fundamental market truisms, mainly that the market is a forward-looking discounting mechanism. It knew of the recession, priced it in already. How much worse can it get than a complete shuttering of the economy shy of e-commerce and spotty retail, healthcare and limited other services and retail sales? I think what many investors miss is the simplicity of $1. What do I mean by that?

If we think in terms of growth, that is all it takes to express growth; one more $1 spent within the economy each day. When you hit the bottom, essentially every $1 more that is spent when compared to yesterday is considered growth. It may not be robust growth, but it’s growth nonetheless. And that is what the market determines, the likelihood of the reopening phase for the current recession finding one more $1 a day spent delivering growth, at least.

In a recent blog post from Ben Carlson, the market participant identifies this truism of markets and how the irrational alignment of the economy and market is actual, rational, normal in many respects throughout history.

“There have been plenty of times in the past when the stock market is seemingly out of step with the broader economy.

The stock market showed strong gains through both World War I and World War II, possibly the most uncertain of times in the past few hundred years.“

“…economic data is backward-looking and the stock market is forward-looking. That’s easy enough to understand but the current situation still doesn’t quite feel right.

Five or six weeks ago, when most of the stay-at-home orders went into effect, you didn’t have to be a genius to realize the terrible impact this would have on the economy. This was the easiest recession to predict in history.

In past crises, you could look to certain data points for clues in the economy to guess what was coming but never something like this that was so telegraphed.

If you think you’re smarter than the market than don’t be surprised when you find out otherwise. The market seems to rather enjoy when investors plan for this move or that move; it laughs as it does the unthinkable and contrary to your plans. I think the best thing an investor/trader can do for themselves with so many unprecedented circumstances and already occurred market moves is to remain flexible and humble. If you don’t know, you don’t know. There’s no harm to come from being flexible during these uncertain and unprecedented times in society, the market and economy. One can certainly harm themselves and their portfolio by putting ego before the market, only to find the market with greater capacity to overcome ego!

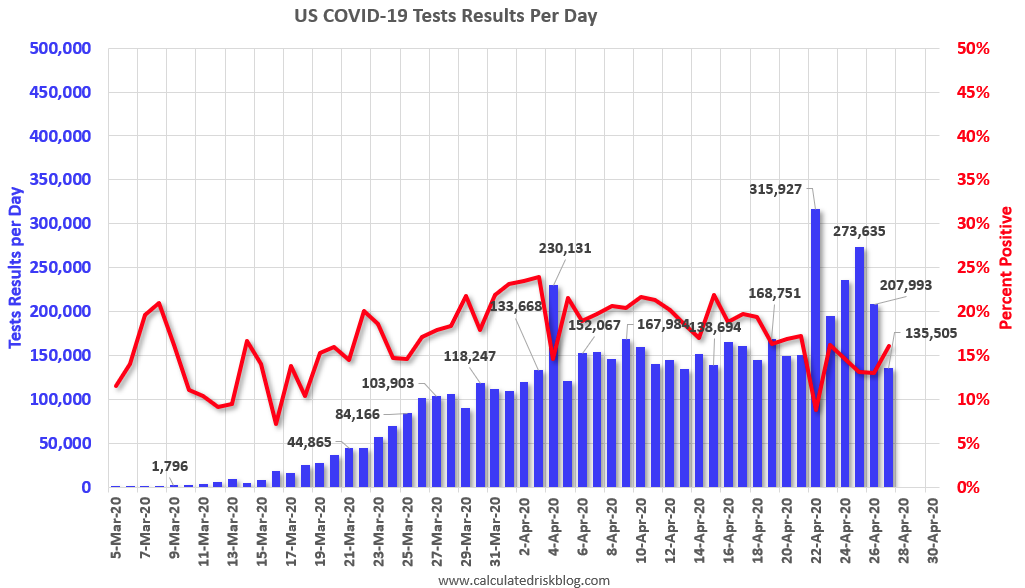

As the economy looks to reopen over the coming weeks and months, testing capacity remains front of mind and mostly desired. Talks of opening too soon and secondary spread are not the daily narrative, given the limitations on testing capacity. The Trump administration unveiled a new strategy Monday to help states ramp up their capacity to test for coronavirus, claiming most of its work is done, according to 2 new documents. But this is where we continue to see a lack of actual plans, and more defensively positioning by the White House Administration. And this is not to be political by making that statement, but rather a truth expressed by Dr. Fauci and ongoing testing capacity data at-hand.

Fauci said in a webcast hosted by the National Academy of Sciences that that the U.S. is currently averaging between 1.5 million and 2 million tests per week.

“We probably should get up to twice that as we get into the next several weeks, and I think we will,” Fauci said. “Testing is an important part of what we’re doing, but it is not the only part.”

You need enough tests so when you’re doing what we’re trying to do right now, which is trying to ease our way back, that you can very easily identify, test, contact trace and get those who are infected out of society so they don’t infect others,” he said, adding that positive test results should account for less than 10 percent of tests administered.

Based on these comments from Dr. Fauci, the U.S. might be able to test 400,000 to 600,000 people per day in several weeks, and that would probably be sufficient for test and trace. There were 135,505 test results reported over the last 24 hours.

Moreover, here’s what the President offered to the public on Monday:

“We’re deploying the full power and strength of the federal government to help states, cities, to help local government get this plague over with.”

The first of the 2 documents, the testing overview, largely serves as a defense of the administration’s widely criticized handling of the coronavirus testing since the start of the epidemic. It outlines eight responsibilities that it says belong to the federal government, and claims to have already completed seven of these. Responsibility explanation is not a strategy, it’s a defense.

The other document, a testing “blueprint,” describes what it calls a “partnership” between states, the federal government and the private sector. The partnership it describes leaves the lion’s share of responsibility for funding, designing and executing a coronavirus testing plan to individual states. Again, outlining responsibility is not a strategy, it’s a defense without outlined actions the Administration plans to take, other than funding efforts. Maybe this is the way the Administration wants it to be, decentralized. If the state governors desire the continued independence granted through Federal separation of states and the Federal government, it seems as though that is what they are getting, no?

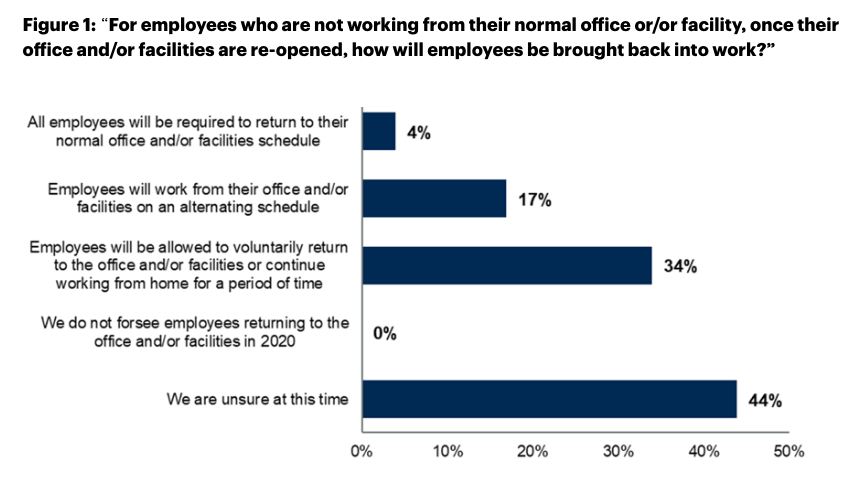

Here’s the thing, it’s all new and we likely won’t know what will come and I’m ok with that. As an investor, we simply have to accept that we don’t know sometimes and we’ll find out soon enough, with hindsight and learned experiences. Investors aren’t the only one’s not “in the know”! CFOs and CEOs are also uncertain and without a “playbook” for reopening the economy as they’ve never been confronted with this situation and these circumstances that may prove ongoing for months.

A Gartner, Inc. survey of 99 CFOs and finance leaders taken April 14-19 (positioned above), 2020* revealed that 42% of CFOs are not incorporating a second wave outbreak of COVID-19 in the financial scenarios they are building for the remainder of 2020.

Additional survey data showed that that only 8% of CFOs have a second wave factored into all their planning scenarios, and only 22% have a second wave factored into their “most likely” scenario. The lack of planning comes even as CFOs express a cautious approach as to when they will fully reopen their operations and bring employees back to their normal office routines.

“As CFOs are attempting to project revenue and profits for 2020, it’s surprising that 42% are not baking a second wave of COVID-19 into any of their scenarios” said Alexander Bant, practice vice president, research, for the Gartner Finance practice. “Our latest CFO data also reveals that most executive teams are still trying to decide what factors they should use to determine how and when to reopen their offices and facilities.”

Stay nimble, flexible, humble and let the information flow. The more information you have, the better your decision-making with your capital allocations will be. Have a team of resources at your disposal to facilitate thoughtful investing and economic dialogue and whatever your do, don’t “go it alone”. You’re not better than Mr. Market, regardless of what you choose to believe!

{kind=link}

The Onyx reference! Of course… ♥

And you know this maaaaaaaannnnnn! 😉