Welcome to this week’s State of the Markets. Please click the following link to review the SOTM video . Our emphasis in this week’s SOTM video concerns the overextended bond market rally and potential consequences that could create additional equity market volatility, underlying economic data that continues to outline the strength of the consumer and trend-growth GDP pace and what investors need to consider now that the market has retraced some 6.5% in the last two weeks.

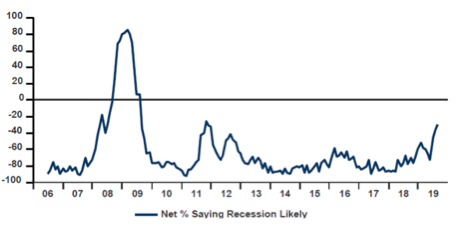

- 34% of FMS investors think a recession is likely in the next 12 months, the highest recession probability since Oct’11. Similar to BofAML U.S. economists that think there is close to a 1 in 3 chance of a recession in the next 12 months.

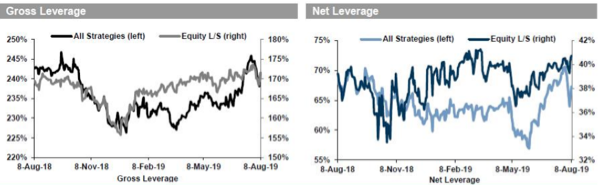

- The overall GS Prime Brokerage book was net sold for the first time in nine weeks

- Gross leverage of the overall book decreased -0.9 pts to 241.6% (77th percentile one-year) and net leverage decreased -1.4 pts to 67.3% (80th percentile).

- North America’s weight vs. the MSCI fell -1.9 pts to -1.2% underweight… Since GS began tracking the data (Oct ‘07), the GS PB Book has only been underweight North America three times: Feb ’08, Nov ’17, and this week.

- “Low unemployment, rising real wages, moderate energy prices, the surge in mortgage refinancing and the 7.3 million job openings firms are still desperate to fill — all suggest that consumers will continue to spend enough to contribute to GDP growth even as businesses retrench.”

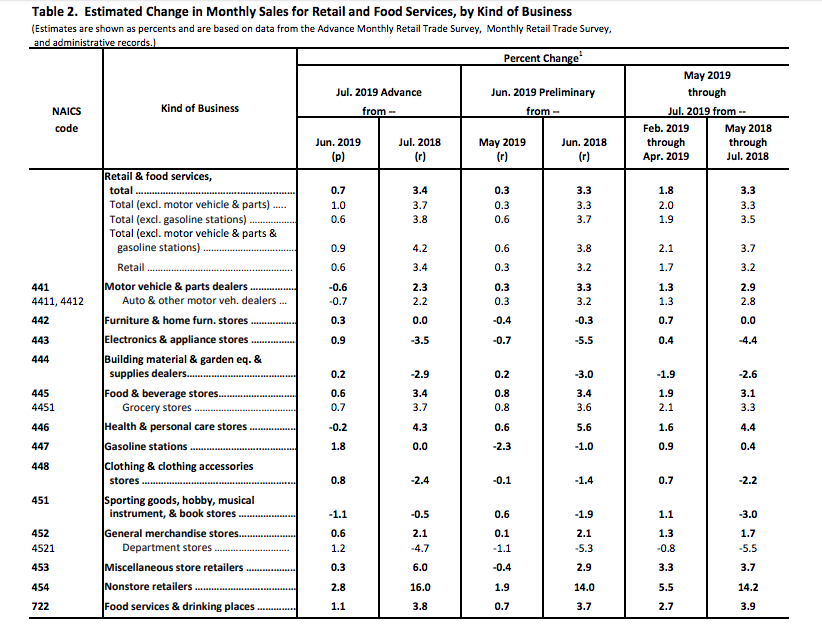

- July retail sales rose .7% MoM and 3.4% YoY. Dept. Store retail sales rose 1.2% MoM but fall 4.7% YoY. Nonstore retail sales continue to syphon sales from brick & mortar retailers, growing 2.8% MoM and 16% YoY.

- We suspect some growth was pulled into July at August’s expense. After all, Prime Day was a big driver of sales. Non-store retailing exploded 2.8% in July. Still, ex non-store retailers, core sales rose a respectable 0.4% and up 5.1% annualized over the last three months.

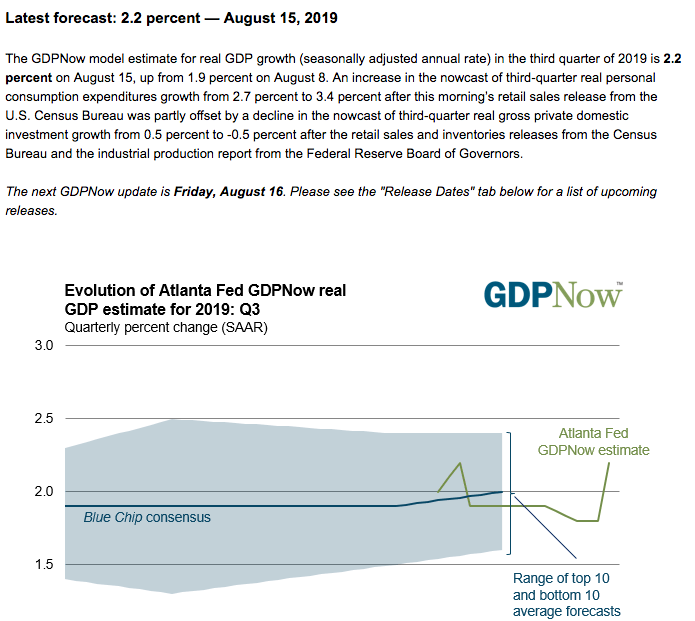

- Following today’s data deluge, Goldman boosted its Q3 GDP tracking estimate by two tenths to +2.1%

- Merrill: “The data boosted our 3Q GDP tracking estimate by 0.4pp to 2.1% qoq saar. 2Q was unchanged at 1.8%.”

- Very light economic calendar next week. FOMC and Housing industry related data highlight the week.

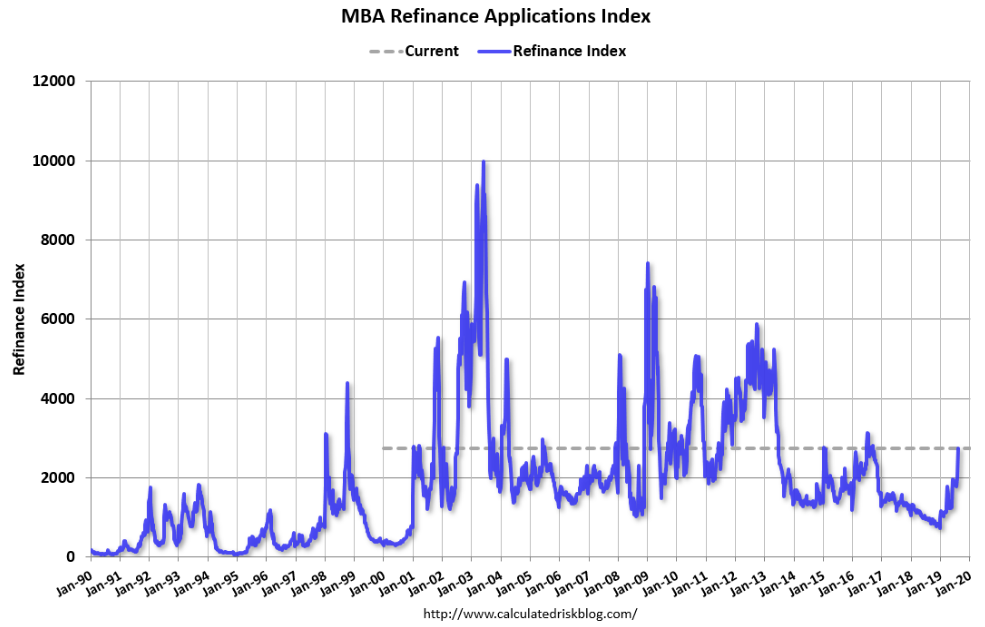

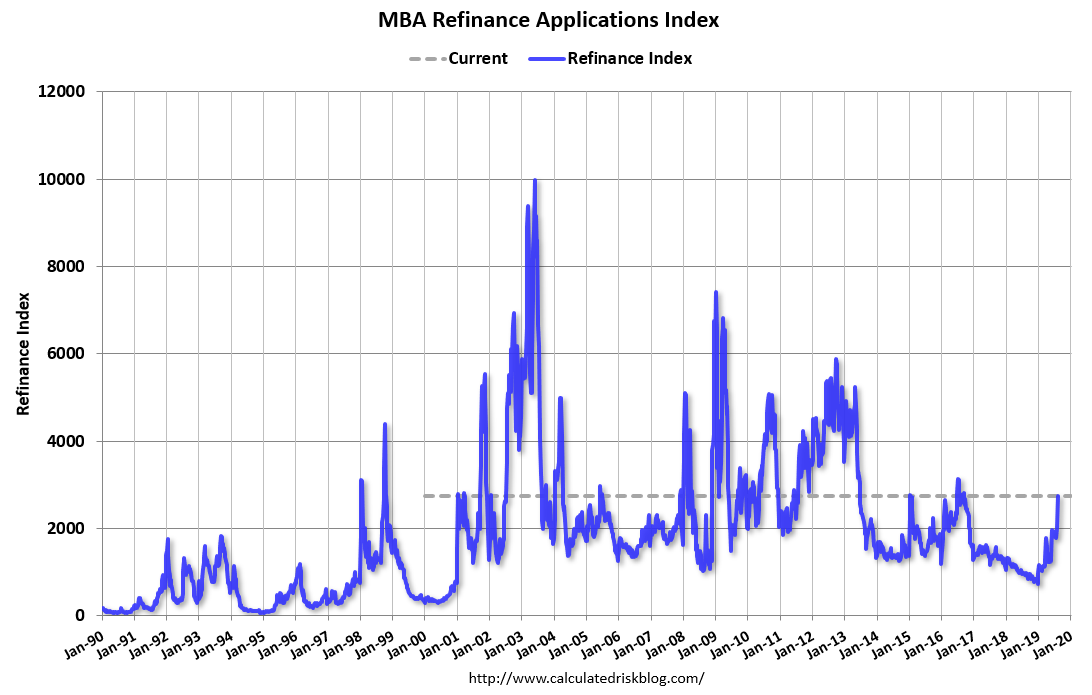

- 37% jump in refinance volume for the week, the highest level since July 2016. Refinance applications were nearly 196% higher than a year ago.

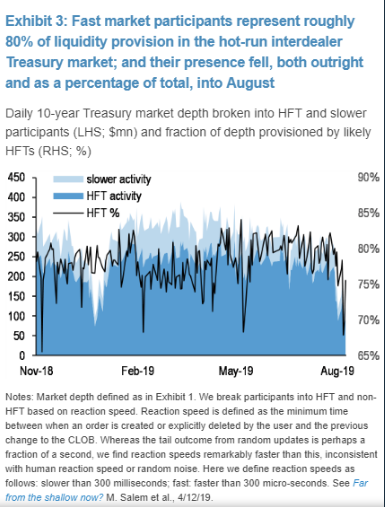

- Behind the wild swings in Treasurys? Diminishing liquidity, potentially caused by ultrafast traders pulling back this month, JPMorgan says.

{kind=link}

{kind=link}

Interesting point about the overextend and overbought bond market at the moment and will that have an effect on other markets when it unwinds. The most recent example of when government bonds became extremely overbought was in 2016 just after the EU referendum in Britain. UK government bond yields fell by 1%. The impact was not isolated to the UK however as the 10 years Treasury fell by 0.8%. I’m sure you remember 2016 that equity markets sold off and volatility quickly rose but it impact didn’t last very long as equity markets quickly recovered and within a few months US treasury yields rose to previous levels.

I don’t see that the concentration is a Volmagedon impact though like Feb 18 as the bond market is just way too big and liquid (especially government bonds). The bond market is even bigger than the equity (by about 10trn) so I think that there will be plenty of buyers (especially insurance companies and pension funds) to handle the unwind. Don’t get me wrong I can imagine some big moves in the bond market (either up or down) but I don’t think concentration will be a problem like what in the volatility complex during Volmagedon.