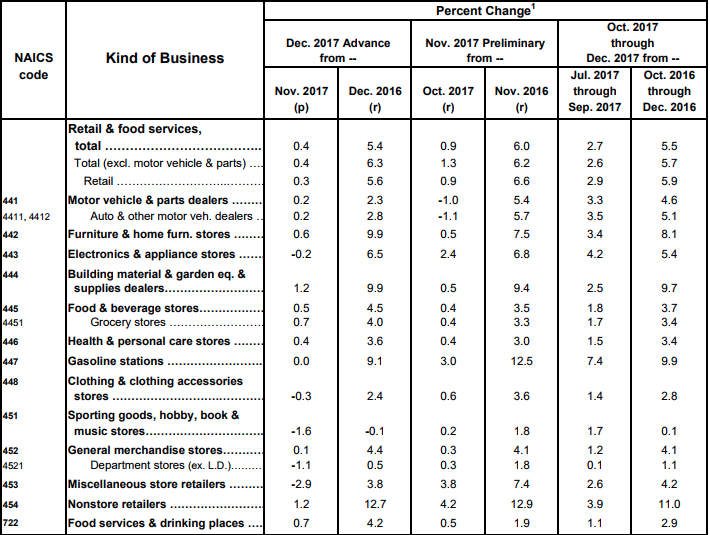

Last Friday, December 2017 monthly retail sales were reported. The Commerce Department said on Friday that retail sales rose 0.4% last month. Data for November was revised to show sales gaining 0.9% instead of the previously reported 0.8% increase. Retail sales in December rose 5.4% from a year ago. Excluding automobiles, gasoline, building materials and food services, retail sales increased 0.3% last month after an upwardly revised 1.4% surge in November.

Some of the key focal points in the Commerce Department’s retail sales dissemination noted in their table above surround Department Store and Nonstore retail sales contribution to the net total monthly retail sales. It was encouraging to witness Department Store sales climb .5% YOY even as MoM sales fell 1.1 percent. The 1.1% decline from November to December should be expected as Black Friday (November 24-25) sales proved greater than the previous year and where the greatest of holiday sales proliferate.

What proves problematic, however and after reviewing Department Store sales for the period, is that Nonstore or online sales continue to grow at a double-digit rate YoY while climbing MoM. For the reporting period, Nonstore sales grew 12.7% YOY and 1.2% MoM. The backdrop for Nonstore sales continues with strong momentum into 2018. While the surge in reporting department store sales from the likes of Macy’s, J.C. Penney, Target and the like have been favorable during the holidays, the Nonstore sales component of the total retail sales report may offer that these corporate reporting metrics may be little more than improvements off of very low comps in the previous year. Such improved performances may last through the 1st half of 2018, but will also prove a difficult comp in the back half of the year. Until then, the headlines from media outlets will likely continue to beat the drum that spouts, “brick & mortar revival is upon us”!

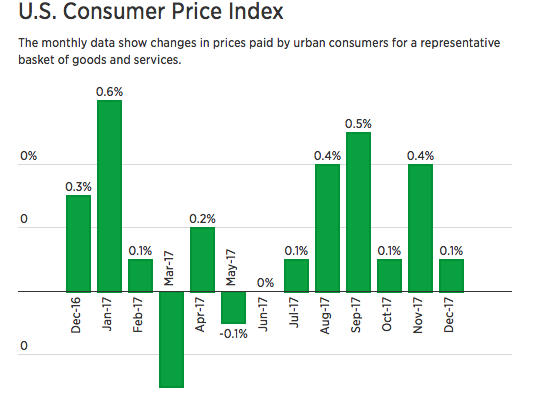

Alongside the monthly retail sales, last week we received a review of the latest inflationary metrics by way of Consumer Price Index or CPI. U.S. consumer prices recorded their largest increase in 11 months in December amid strong gains in the cost of rental accommodation and health care, bolstering expectations that inflation will gain momentum this year. The Labor Department said its Consumer Price Index excluding the volatile food and energy components rose 0.3% last month also as prices for new motor vehicles, used cars and trucks and motor vehicle insurance increased.

The rise in underlying inflation pressures last month could largely be attributed to rent increasing 0.4 percent. Rent for primary residence climbed 0.3% after gaining 0.2% in November. The cost of medical care increased 0.3%, with prices for prescription medication surging 1.0% after rising 0.6% in November. The cost of both hospital and doctor visits increased 0.3 percent.

Households also paid more for new motor vehicles, which rose 0.6% in price last month, the biggest gain since January. The cost of motor vehicle insurance increased 0.6 percent. Apparel prices, however, fell 0.5 percent.

The U.S. economic data has been strengthening coming out of 2017 and into the early portion of 2018. Next week will prove to present limited economic data. Most investors and traders will be eyeing Wednesday’s release of the Fed’s Beige Book.

Tags: BBBY TGT WMT XRT

{kind=link}

Seth Golden always does the due diligence in his articles. Plenty of research there