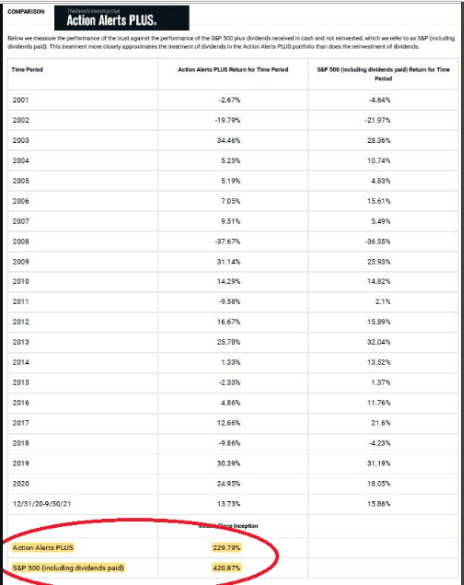

Research Report Excerpt #1

“How does Jim Cramer of CNBC do so well then?”

The short answer to the question above is: He doesn’t!

As the tracked data analyzes, for every $1 invested in the Jim Cramer Action Alerts Plus recommended investment, an investor would have earned half of what they would have earned if they invested in the S&P 500 index ETF (SPY). That’s right, for all the pomp and circumstance associated with the famed Jim Cramer, his Action Alerts PLUS service massively underperforms the S&P 500 on an annualized basis and since inception.

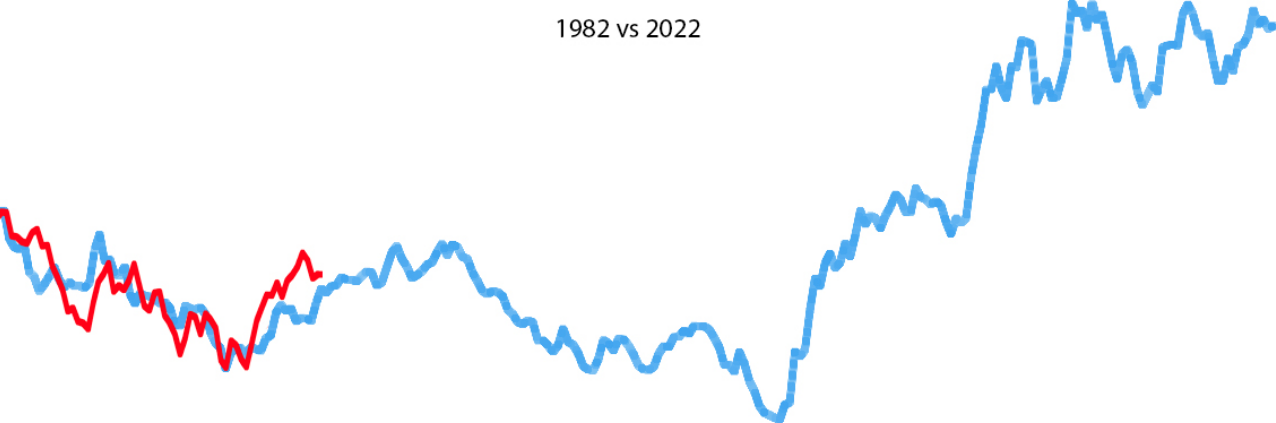

Research Report Excerpt #2

First and foremost is the still very much aligned 1982 Analogue update:

Does it get any more precise than this folks? The analogue continues to perform quite well and did so this past week. In 1982, the S&P 500 fell in the 2 days leading into the end of the quarter and then rose on the first trading day of April. The S&P 500 did the very same thing this past week. While the marginal decline in 2022 is slightly less than that which occurred in 1982, the path is very much the same.

Research Report Excerpt #3

Coupled with long-term breadth proving less than bullish, investors have become increasingly defensive as the 3-week rally progressed. No, I’m not trying to scare anybody, and yes, I realize the market internals paint a less rosy picture than price action, but our job is to remain objective and do our homework so as not to be surprised by market price action; let’s not make irrational portfolio decisions. It’s all emotions, and when you DO KNOW you CAN remain cool, calm and collected regardless of the price action.

The top chart is the performance ratio of the Dow Transportation Average (DJT) relative to the Dow Utilities Average (UTIL). Because DJT is determined to be more of a cyclical/economic index and Utilities more defensive and not economically sensitive, when the trend line is moving lower that indicates investors are seeking defensive positioning. And man alive has the trend line cascaded lower this past week and over the past 2 weeks while the S&P 500 rose. This is not bullish positioning folks.

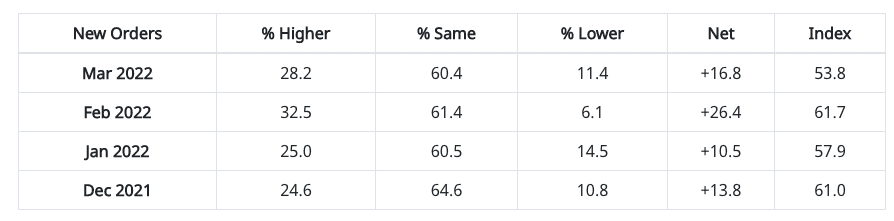

Research Report Excerpt #4

ISM‘s New Orders Index registered 53.8 percent in March, a decrease of 7.9 percentage points compared to the 61.7 percent reported in February. This indicates that new orders grew for the 22nd consecutive month. While the New Orders Index remains in growth territory, the month-over-month decrease is the largest since a 15.3-percentage point drop in April 2020. “Five of the six largest manufacturing sectors increased new orders at moderate-to-strong levels: Food, Beverage & Tobacco Products; Transportation Equipment; Chemical Products; Computer & Electronic Products; and Machinery. Price instability, softening lead times and panelists’ order books being full resulted in a pause in new order rates. Backlog and customer inventories remain at very encouraging levels, indicating that demand remains strong in spite of this month’s slowing in new order expansion,” says Fiore. A New Orders Index above 52.9 percent, over time, is generally consistent with an increase in the Census Bureau’s series on manufacturing orders (in constant 2000 dollars).

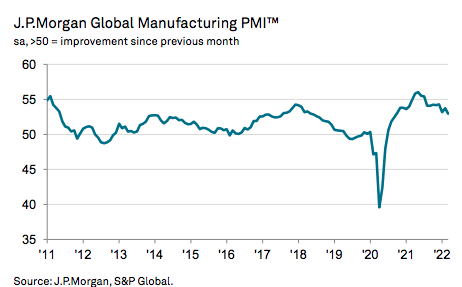

Research Report Excerpt #5

Nonetheless, when we look at global manufacturing, here is what we come to find, as outlined by J.P. Morgan:

“March saw the rate of expansion in global manufacturing production slip to its lowest during the current 21-month sequence of increase. Output and demand growth were hampered by multiple headwinds, including ongoing COVID disruptions, stretched global supply chains, rising inflationary pressures and elevated geopolitical tensions. The J.P.Morgan Global Manufacturing PMI™ – a composite index produced by J.P.Morgan and S&P Global in association with ISM and IFPSM – fell to an 18-month low of 53.0 in March, down from 53.7 in February. Although signaling an improvement in operating performance for the twenty-first consecutive month, the rate of growth was the weakest since September 2020.”

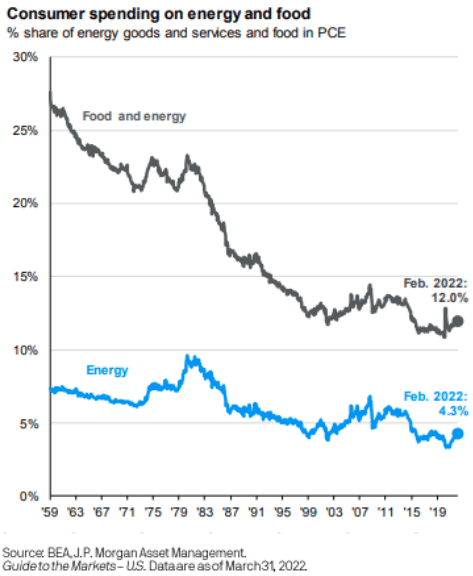

Research Report Excerpt #6

So while indeed, prices have risen for these goods, consumption has fallen for such goods, rendering the impact muted on the household balance sheet. (chart below)

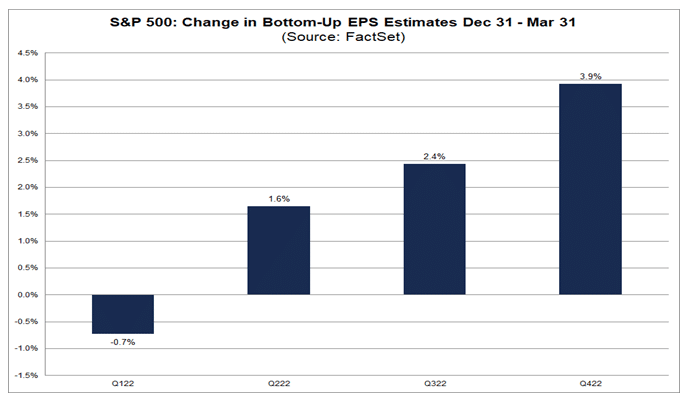

Research Report Excerpt #7

I would remain of the opinion, despite the lowered estimates and negative guidance, that realized EPS growth will be significantly higher than the estimates. Additionally, you’ll notice that while the Q1 EPS estimate fell slightly this past week, the FY 2022 EPS rose from 9.4% to 9.5% growth. Additionally, each successive quarter found estimates rising (chart below):

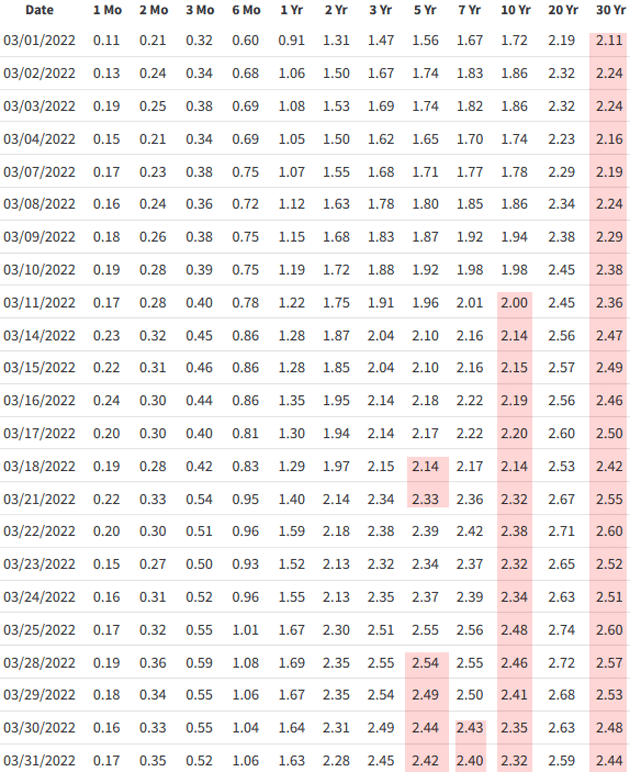

Research Report Excerpt #8

Here’s a table showing March’s daily Treasury pair yields. Normally you would see numbers increase along each row. I highlighted points where they drop. These are inversions and they are not normal. They seem to be spreading from right to left.

Yields are supposed to reflect risk, and risk grows with time. The chance something bad will happen in the next 10 years is higher than the chance something equally bad will happen in the next two years. Longer-term bond investors should demand higher yields as compensation for that higher risk. Presently they aren’t, or at least not always.

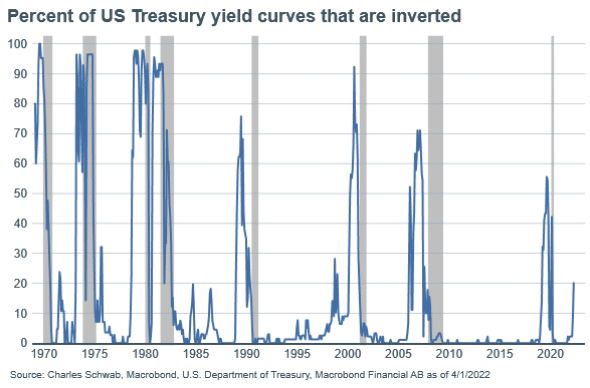

Research Report Excerpt #9

As the chart above shows, where in the previous week there was roughly 10% of yield-curves inverted, there are now 20% of yield-curves inverted (far right hand side for 2022). While it doubled in the span of a week, and that seems alarming, keep in mind this happened as a reaction to the strong Nonfarm Payroll report on Friday. The strength of the labor market combined with strong consumption is fueling an actual desire for the Fed to raise rates, which is what the bond market is pricing. Hence, while more of the yield-curve has inverted rather quickly, it is likely to slow in the coming months and with realized Fed rate hikes. Markets, bond and/or equity, are forward discounting mechanisms.