It was a turbulent time for equities and the S&P 500, which lost nearly 4% during the month of February. Rounding out the month yesterday, the S&P 500 finished lower by roughly 1.1% and with all three major indexes finished lower on the day. The Dow was the biggest loser, closing down by 1.50 percent. Investors continue to ride the roller coaster market in search of equilibrium that seems elusive at this time. Interest rates and inflation concerns headlined the month of February as the new Fed Chairman took to the helm of the Federal Open Market Committee. Fed Chair Jerome Powell is set to deliver his testimony today at 10:00 a.m. EST and before the Senate Banking Committee.

After appearing somewhat hawkish in his testimony before the House on Tuesday, some analysts are hoping the Fed Chair will dial back some of his comments concerning the possibility of further rate hikes. The debate prior to the Fed Chair’s first testimony had been centered on 3 rate hikes in 2018, but Powell’s comments hinted at the possibility of 4 rate hikes as determined by analysts and economists alike. It’s unlikely that his testimony will change all that much today as the Fed Chair would probably want to present a clear and consistent message.

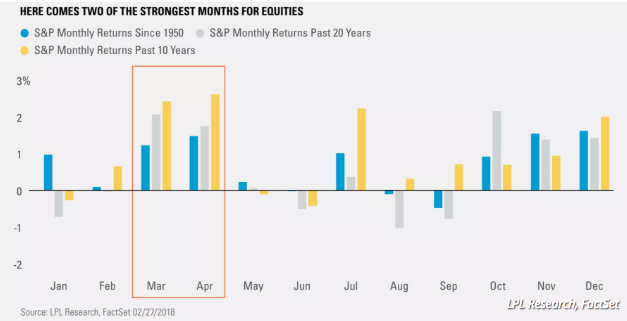

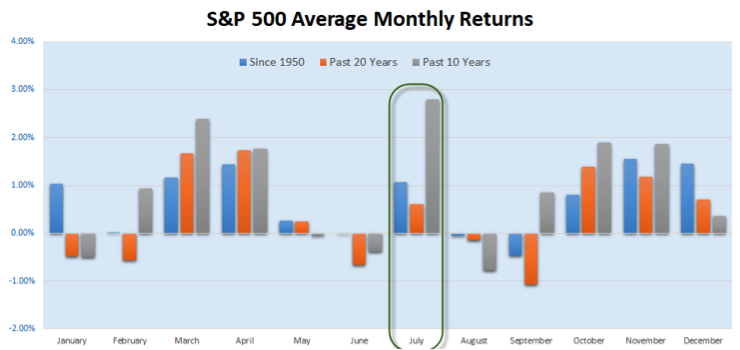

While equity markets went out whimpering in February, March as historically been a strong month for equity markets. Over the past two decades, March has been the second strongest month for the S&P 500 on average.

And April has historically been even stronger than March. This strength has also been reflected in returns, as March raked in 4.1% on average over the past two decades, outdone only by the average October, according to LPL. Going back to 1950, average March returns were 1.3 percent.

As Bitcoin attempts to regain its former traction and high water mark trading prices, regulators are on the march. The Securities and Exchange Commission (SEC) is looking into the cryptocurrency market according to The Wall Street Journal. The newspaper reported that, as part of that investigation, the SEC has issued “scores of subpoenas” to obtain information from technology companies and advisors tied to the digital currency markets. Sources told the Journal that the agency is looking into the structuring of initial coin offerings, which are not as heavily regulated as public offerings.

GDP was revised lower from 2.6% to 2.5% as expected. Some of the latest economic data has been coming in softer in the month of February, especially around the housing market. But even with softer than forecasted new and pending home sales, home prices continue to surge as inventory remains scarce. Nonetheless, consumer sentiment is on the rise. The Conference Board says its consumer confidence index rose to 130.8 in February, highest since November 2000 and up from 124.3 in January.

“Overall, consumers remain quite confident that the economy will continue expanding at a strong pace in the months ahead,” says Lynn Franco, the Conference Board’s director of economic indicators.

Tax cuts and low levels of unemployment continue to drive consumption trends. Recently reporting retail companies have pointed to tax cuts as bolstering consumption and sales, giving them confidence in their outlook for 2018.

“As people slowly absorb the details of the tax reform package, opinion polls suggest that it is becoming significantly more popular,” Stephen Stanley, chief economist at Amherst Pierpont Securities, wrote in a research note.”

With consumer sentiment at levels not seen since 2000, retailers still have an uphill battle ahead given the trends surrounding consumption and the shifting habits toward purchases made online. According to The Star Tribune who first reported on the news Wednesday afternoon, Best Buy will be closing all of its smaller mobile phone stores. CEO Hubert Joly confirmed the reporting in a memo to employees. The stores, which are about 1,400 square feet in size compared with Best Buy’s bigger boxes of 40,000 square feet, are scheduled to close by the end of May. There are 250 stores altogether that are planned to close.

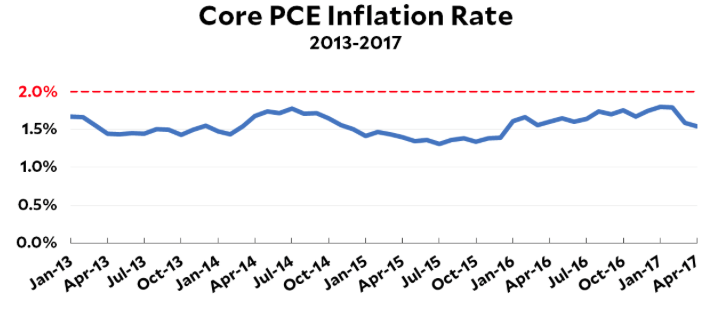

Equity futures are pointing to another triple-digit loss at the open for the Dow Jones Industrial Average. When Fed Chairman Powell begins his testimony today, once again all eyes and ears will be focused on his verbiage. But leading up to the testimony, all eyes will be centered on the all-important inflation data coming out this morning in the way of Personal Consumption and Expenditures or PCE for short. This is the more important and highly monitored piece of economic data that the FOMC monitors and looks toward with regards to inflation expectations and benchmarking. Personal income and consumer spending are both expected to have grown by .3% during the month of January. Core inflation is also expected to tick higher by .3% in January 2018. Should the inflation data come in hotter than anticipated, it could perpetuate fears centering on inflation and the potential for additional rate hikes in 2018. On a side note, ISM manufacturing, weekly jobless claims and construction spending are all due out this morning.

{kind=link}