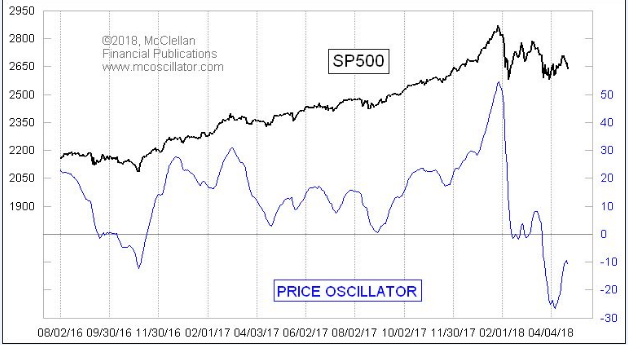

After a nearly 200 point drop on the Dow Jones Industrial Average yesterday, the index managed to close higher, ahead of key tech earnings due out after the close. The Dow and S&P 500 finished to the upside by roughly .2% while the Nasdaq finished the session flat or down .05% on the day. Nonetheless and even with stocks rallying off their intraday lows, ominous signs for market participants have been brewing. The “big bear market” for stocks that market timer Tom McClellan has been expecting appears to have begun and largely due Tuesday’s market selloff. The selloff turned a key technical indicator down from an already negative position to convey a “promise” of lower lows. The McClellan Price Oscillator, a technical indicator using exponential moving averages of closing price data, turning down after it was already in negative territory, is depicted in the chart below. McClellan, who doesn’t believe in percentage-decline definitions, said stocks are already in a bear market.

“Turning down a Price Oscillator while it is still below zero conveys the promise of a lower closing low on the ensuing move. I have been looking for a big downturn in late April. We appear to have gotten that downturn now. It should be a lasting and painful downtrend, heading down toward a bottom due in late August.

If the McClellan Price Oscillator and Tom McClellan’s outlook weren’t bearish enough, a recent survey of consumers about the stock market also proves concerning. According to data from the Conference Board, just 32.7% of consumers expect stock prices to be higher 12 months from now, the lowest percentage since November 2016. Meanwhile, 33% of respondents expect stocks to be lower in a year, the highest reading since July 2016. April represents the third straight month that the ratio of optimists has dropped, and the fifth straight month that the number of pessimists has risen. In discussing the recent survey, Morgan Stanley’s chief of U.S. equities had the following to say.

“As expected, 2018 has proven to be more difficult. U.S. returns are near zero year-to-date; volatility has made it feel worse. Over the past several months, the market has become much narrower, a classic sign of underlying deterioration, in line with our outlook for 2018. We think the main drivers of this deterioration are lower quality earnings growth and tighter financial conditions, both of which are likely to be with us for the rest of the year.”

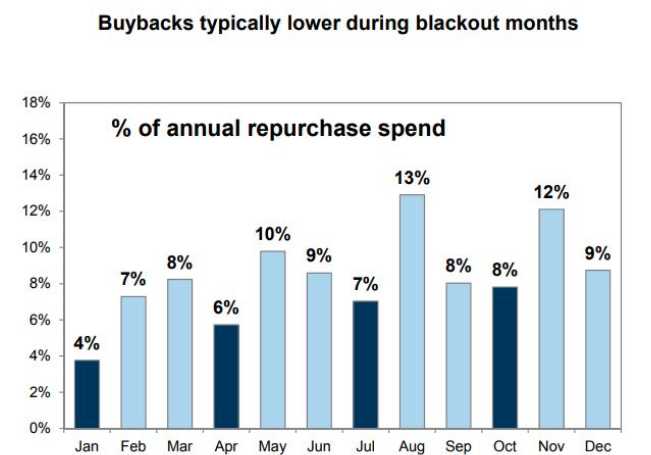

The markets have been unusually volatile in 2018 and especially compared to the record-low levels of volatility witnessed in 2017. But volatility isn’t the only factor keeping equities and the major indexes from recapturing their former glory. Major U.S. corporations are in their “blackout” period for stock buybacks, which refers to how most companies and insiders are prohibited from repurchasing their own shares in the month before the release of their quarterly results. Recently, trading volumes have been unusually low due in part from the lack of trading volumes otherwise expressed in non-blackout periods.

“Given corporations represent the largest single source of demand for U.S. shares, equity returns have typically been lower and volatility higher during blackout periods, wrote Goldman Sachs earlier in February, which also coincided with the market correction.

There are four blackout months a year. The four months that achieve the greatest volume activity are January, April, July, and October. On average, 6.25% of a company’s annual repurchasing expenditure is done in a blackout month, compared with 9.5% for non-blackout months and 8.4% overall.

Speaking of blackout periods that precede and coincide with earnings periods, let’s get into some of the earnings that came after the bell yesterday. Most were better than expected and found a few companies boosting their full-year outlook.

AMD reported much stronger sales than expected in the first quarter and said that crypto-mining was 10% of overall revenue, a larger portion of sales. While executives admitted that they expect a “modest decline” in crypto-related revenue next quarter, the company’s revenue forecast for the second quarter exceeded expectations. AMD reported first-quarter net income of $81 million, or 8 cents a share, on sales of $1.65 billion, up about 40% from $1.18 billion a year ago. After adjusting for stock-based compensation and other factors, the company claimed earnings of 11 cents a share, up from a break-even performance a year ago. The firm also guided for stronger revenue growth in the current quarter. AMD guided to revenue of $1.68 billion to $1.78 billion, while analysts were forecasting $1.58 billion. AMD said that would mean 50% revenue growth.

PayPal reported a quarterly profit of $511 million, or 42 cents a share. That compares with $384 million, or 32 cents a share, in the same period of 2017. On an adjusted basis, PayPal’s per-share earnings rose to 57 cents, above the estimate of analysts polled by Thomson Reuters. Net revenue climbed 24% to $3.69 billion, more than the $3.59 billion analysts were expecting. Payment volume totaled $132 billion, up nearly one-third from the same period a year ago. A fifth of that volume came from cross-border trade. Venmo, PayPal’s mobile person-to-person payments service, handled more than $12 billion in volume during the first quarter. That was 80% more than the volume it handled in the first quarter of 2017, a slower growth rate than previous periods. For 2018, PayPal told investors to expect more revenue but less net income than it had previously offered as guidance. Full-year revenue is now expected to be as much as $15.4 billion, up $150 million from its previous outlook, while per-share earnings are now projected at as much as $1.76, down from a previous maximum of $1.86. The company’s income-tax expense fell 31% to $37 million, causing its effective tax rate to go to 7% from 12%.

Qualcomm reported fiscal second-quarter net income of $363 million, or 24 cents a share, compared with $749 million, or 50 cents a share, in the year-ago period. Revenue rose to $5.26 billion from $5.02 billion in the year-ago period, while Wall Street had forecast $5.19 billion and Qualcomm had predicted revenue of $4.8 billion to $5.6 billion. Estimize had expected revenue of $5.28 billion. For the third quarter, Qualcomm estimates adjusted earnings of 65 cents to 75 cents a share on revenue of $4.8 billion to $5.6 billion, while analysts expect earnings of 75 cents a share on revenue of $5.28 billion.

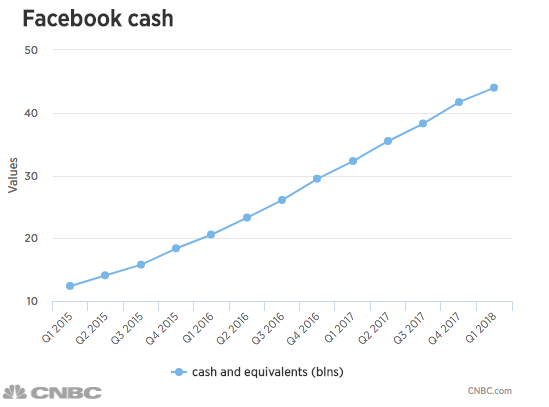

Facebook recorded record results yesterday, with total revenue growing 49% to nearly $12 billion and net income of $4.9 billion. Facebook said in its first-quarter earnings report that cash and equivalents rose to $44 billion in the period. That’s more than double the amount the company held just two years ago, when its cash stockpile sat at $20.6 billion.

Even as a mature company facing public backlash, Facebook managed to increase its revenue growth, an astounding feat. Facebook said its daily active users grew 13% in March to 1.45 billion on average, and monthly active users grew 13% to 2.2 billion. That was only a slightly slower pace than in the December quarter, when both daily active users and monthly active users grew 14 percent.

“This quarter, we’ve continued shifting from passive consumption to encouraging meaningful interaction. It’s still early but we’re starting to see some signs that this is working,” Facebook Chief Executive Mark Zuckerberg said in Wednesday’s conference call. “Some types of sharing are increasing even as passive consumption of video is down. We expect that European MAU [monthly active users] and DAU [daily active users] may be flat to slightly down sequentially in Q2 as a result of the GDPR rollout,” Facebook Chief Financial Officer David Wehner told analysts. “While we do not anticipate these changes will significantly impact advertising revenue, there is certainly the potential for some impact and we will be monitoring this closely.”

Earnings season will peak this week, but not end and with that the news cycle will continue to center on corporate and economic fundamentals going forward. However, investors are presently keying their decisions off of reflation/rising rates and geopolitical fears concerning trade/tariffs. Earnings, while coming in largely better than expected, have taken a back seat to the aforementioned macro factors. With the 10-yr. Treasury yield touching and reaching beyond 3% this week, investor fears have crept more broadly into the equity markets. But CNBC’s Jim Cramer said there’s no reason to start selling.

“You now have lots of investors and commentators acting like this is indeed the end of the world, or, at the very least, I should say, the end of the bull. I think their fear is misplaced.

Furthermore, Cramer said research suggests that moving through this level does not adversely affect equities’ performance. The market often rallies, he said, with rising rates. Other times, the rate peaks past 3% or 4%, once during the 2009 financial crisis and once in 2010 during the recovery, the market “exploded,” said Cramer, with all three major indices rising more than 30 percent.

With respect to the macro-factors weighing on markets, Thursday we’ll see how well our neighbors across the pond feel about their economic outlook as the European Central Bank kicks off. Brace for a dovish message at today’s European Central Bank meeting, say HSBC economists, who pointed to disappointing data and broader worries that could keep the central bank on its toes.

“The macro, and particularly inflation background, is getting more and more important for the ECB as it moves towards starting to normalize monetary policy,” said HSBC economists Fabio Balboni and Simon Wells, in a note last week.

Most economists and analysts are expecting no change in the ECBs language at the meeting today. Additionally, they are looking for greater details on the central banks asset purchase program, which may be extended further than anticipated.

Given the various macro and sentimental factors whipsawing markets over the last couple of months, investors may look to further hedge their portfolios if not actively managed daily. For more active portfolio managers, the volatility has likely proven advantageous and for those who prove to be good “stock pickers”.

As it pertains to trading, yesterday gave Finom Group little confidence that the late day rally was little more than anticipation for strong tech earnings. While such results did come in strong and equity futures are looking higher presently, the recent market selloff on Tuesday may still have lingering market affects, somewhat offered by the McClellan Price Oscillator. As such, a cautious outlook may be the prudent way to participate through week’s end and a Friday that will deliver a first look at Q1 2018 GDP.

Finom Group’s sole trade yesterday came in the premarket and via shorting shares of VXX, a VIX exchange traded product. The trade is defined below in our private twitter feed.

Moreover, Finom Group still holds a previous position entered and looking to trade VXX in continuum as volatility reigns supreme in 2018. To date, Finom Group has a greater than 90% success rate on trade alerts delivered to subscribers. Our most recent longer-term investment in shares of Anadarko Petroleum (APC) have hit the defined price target objective and delivered a greater than 20% return this year. Subscribe today and receive our trade alerts!

Tags: AMD FB PYPL QCOM SPX VIX SPY DJIA IWM QQQ VXX

{kind=link}