After all the hullabaloo on Wall Street Tuesday, the major indices were extremely flat and proved an uneventful trade on Wednesday. The Dow fell slightly with the tech-heavy Nasdaq up a tick. The S&P 500 fell less than a full point as the broadest market index found investors wondering whether or not Tesla (TSLA) is prepared to be taken private as heralded by the firm’s CEO Elon Musk. It has been reported that the SEC is looking into the claims and manners for which the public was informed of the possible transition from a public to private company.

The “bigger” news of the day on Wednesday that likely affected investor appetite for equities surrounded, what else, trade war escalation rhetoric. China said that it would impose tariffs on an additional $16 billion in U.S. autos and energy products, retaliating for the Trump administration’s latest import levies on an equivalent value of Chinese goods.

Even as Trump’s approach to China thus far bears little fruit, administration officials say they are optimistic they will be able to announce by the end of this week agreement with Mexico on key elements of a new North American trade deal. U.S. and Mexican negotiators are finalizing new rules for granting automobiles duty-free treatment, which would require more manufacturing work to be done in high-wage factories.

“Any such agreement would still need to be reconciled with Canada, the third party in the original 1994 North American trade accord. But a U.S.-Mexico arrangement is expected to lead to the end of U.S. tariffs on steel and aluminum from Mexico as well as retaliatory Mexican tariffs that hurt American farmers’ south-of-the-border sales, said Dan Ujczo, a trade lawyer with Dickinson Wright.”

As the S&P climbs out of a near 6-month correction, with each passing day analysts and strategists articulate their bullish and/or bearish outlooks. Morgan Stanley has been bearish on the markets for the bulk of 2018 and maintains that stance in more recent notes to clients. Over the weekend and in Finom Group’s more recent research report, we detail Morgan Stanley’s latest commentary on the markets. The following notes are from Morgan Stanley’s chief U.S. equity strategist, Michael Wilson.

“I’m a bit leery about the fact that small caps have become a perceived safe haven in the event of trade conflicts,” and that this “perception may now be overpriced.

Just remember that those last innings can bring a lot of excitement and anguish, too, depending on which team you are rooting for.

Within the U.S. market, we have noticed a significant divergence between the perceived weakest links and the stronger ones. From a sector standpoint, it’s really down to just technology and consumer discretionary [maintaining strength].

Our call was that these groups are likely to get hit next and, indeed, we think a meaningful correction in these asset categories began late last month. The bad news is that these sectors make up almost 40% of the S&P 500 and close to half of the Nasdaq Composite Index, so the correction will leave a mark on the broader U.S. indexes if we’re right.”

Morgan Stanley continues to warn investors and issue their more bearish insights and outlook on the market this week. The firm seems increasingly worried about market breadth and what it believes are warning bells for investors and traders alike.

“Fewer stocks are carrying the load of the market, a sign of exhaustion and, in our view, a bad signal for further price gains,” the investment bank’s team of analysts wrote. It added that a recent example of a major stock hitting a notable milestone for strength — Apple Inc.’s market capitalization cresting $1 trillion — “sure sounds like a ‘ringing of the bell’ to us.” Rather than the $1 trillion valuation being a sign “that all is right with tech,” Morgan Stanley wrote, it “could be a meaningful historical market for a tradable top.”

While tech and Internet stocks are the most visible momentum plays, Morgan Stanley said this trend was showing signs of deteriorating regardless of market sector. The following chart identifies the divergence between the number of Nasdaq stocks hitting 52-week highs and the Nasdaq price itself.

“Sector-neutral momentum has been breaking down due to the outperformance of defensives and weakness in growth,” it wrote (emphasis in original). “Given the exposure of both discretionary and quant investors to the momentum factor, lingering weakness here can feed on itself and invite further rotations, which will not be good for price momentum leaders — i.e. Tech and other leading growth stocks — or the market.”

While the positioned chart within Morgan Stanley’s notes is undeniable, the analysis and conclusions being drawn bear greater burden of proof. The breadth vs. price divergence has occurred at various points over the last several years with regards to the Nasdaq and more recently in March of 2018. But the present divergence is seemingly elongated; lending itself to rising concern suggests Morgan Stanley. When we consider the tech-heavy Nasdaq, momentum names in the index and recently reported tech earnings we have to also consider the go-forward probabilities. Individual stocks and even indexes or sectors can express weakness in favor of future appreciation that is founded upon earnings. What we learned from tech earnings in the Q2 period is that they continue to come in quite strong.

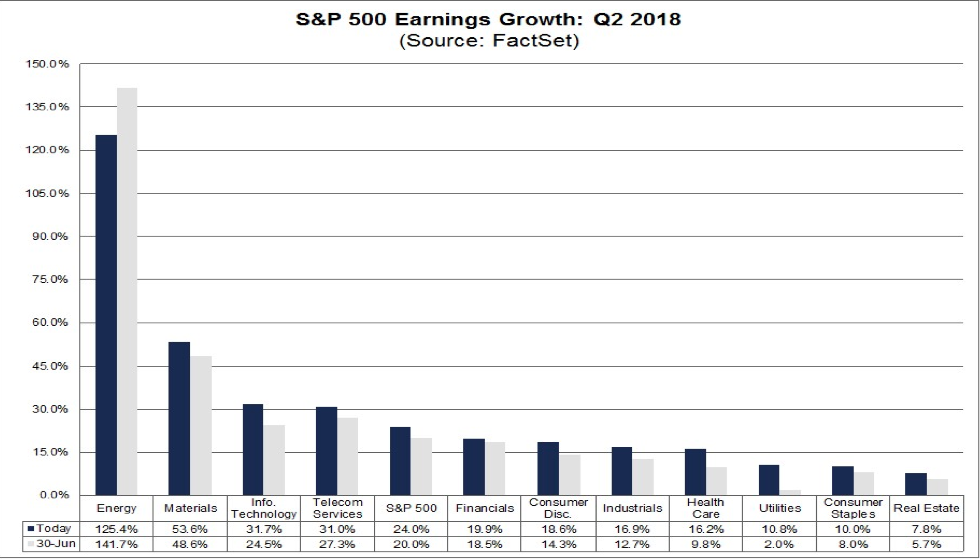

According to FactSet, the Information Technology sector is reporting the third highest (year-over-year) earnings growth of all eleven sectors at 31.7 percent.

At the industry level, all seven industries in this sector are reporting earnings growth. Five of these seven industries are reporting double-digit earnings growth: Internet Software & Services (79%), Semiconductor & Semiconductor Equipment (45%), Technology Hardware, Storage, & Peripherals (29%), IT Services (21%), and Software (14%). So while the Morgan Stanley analysis bears consideration, when we review the earnings growth picture, we come to find that, more than likely, the momentum or high growth technology names may once again set share price records in the future.

Two tech names that have recently been highlighted for greater share price appreciation by Oppenheimer’s Ari Wald, head of technical analysis, are Alphabet (GOOGL) and Apple (AAPL). Wald believes the S&P 500 will achieve a new record high shortly and favors these big cap, mega-tech names. The analysts said investors would want to own stocks in an interview on CNBC.

“Tech is broadly strong across capitalization, across industries. This sector’s going to continue to work,” he said. “Google, breaking out to the upside, breaking above $1,200, that’s a resumption to the stocks’ long-term uptrend.”

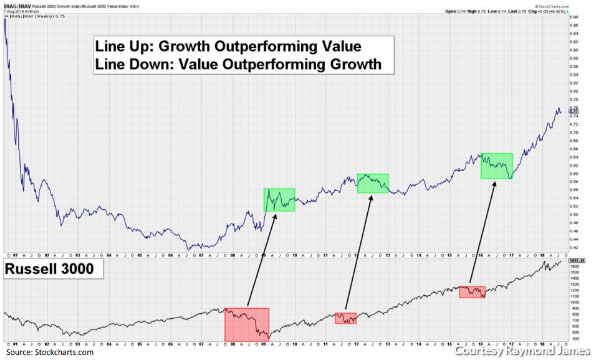

Another consideration regarding Morgan Stanley’s belief that momentum, tech stocks is flagging bearish for even the broader market may be the fact that value stocks have come back en vogue. Investors have expressed the biggest shift from growth to value in nearly a decade, according to Nomura data. However, the move could be premature.

“While value stocks have been doing better recently versus growth stocks, the long-term trend still remains clearly in growth’s favor, and we believe it’s too early to start significantly shifting portfolios toward value sectors,” wrote Andrew Adams, senior research associate at Raymond James. “Given the obvious preference toward growth over the last several years, it will require more than just a few strong weeks for value to really prove it has turned a corner for the long run.”

Since 2006, according to Raymond James, which looked at the growth and value tilts of the Russell 3000, there have only been three occasions when value performed better than growth for meaningful periods. In each case, however, growth swiftly resumed its upward momentum.

As shown in the chart provided by Raymond James, the current lull in the momentum, tech names may just be the typical lull the sector sees from time to time. As such, the analysis offered by Morgan Stanley may be found overly cautious going-forward should the “mo mo” names recapture their glory.

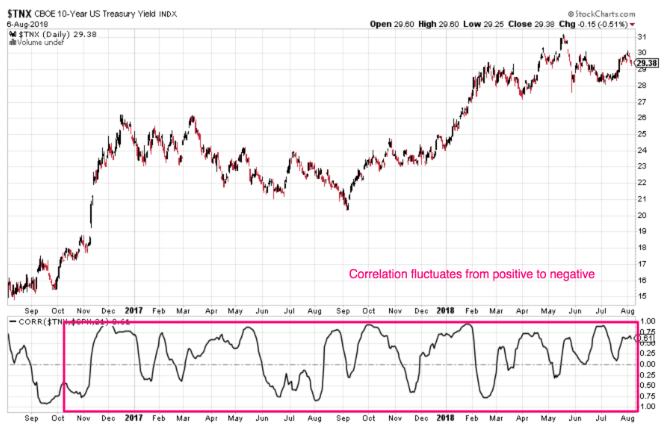

One of the reasons Finom Group believes growth stocks, “mo mo” or otherwise, will outperform value stocks is due to rising rates. There’s a constant drumbeat by the bears that rising yields and rates portend badly for stocks. That simply isn’t true nor has it been historically. This is especially true because yields tend to fall over time with brief periods of reflating. Interest rates are rising right now.

The 10-year yield and S&P 500 have a positive 20-day correlation right now and as depicted in the chart above offered by Troy Bombardia of Bullmarkets.com. Stocks and yields are going up together. This is normal and what has occurred historically. Having said that, the pace of equities rising does adjust to rising rates. By and large, the market has validated this notion in 2018.

More important to the conversation surrounding growth stocks and rising yields/rates is that we believe investors will crave growth stocks in a rising rate environment. Simply put, low growth stocks with dividends will compete with higher yielding treasuries more so than in the past. While the dividend helps alleviate risk associated with low growth stocks, a certain percentage of the investor population will simply allocate more capital to bonds than in the past rather than take the risk with low growth equity names. But high growth equity names likely won’t be hit and Raymond James seems to agree with this thesis.

“We feel that as rates rise, it’s more likely to first take demand away from the lower growth, higher dividend-yield stocks commonly used as bond proxies, rather than the high [earnings per share] growers. A stock with a 2-3% dividend and a lower expected growth rate simply becomes less attractive as interest rates rise, while a stock with the potential to grow earnings at a high rate isn’t as impacted by rising rates.”

There’s definitely a debate concerning what the market is telling investors that will carry forward through the remainder of 2018. Truth be told, Morgan Stanley’s bearish outlook on the market may come to fruition, even if not for the firm’s stated thesis.

Tags: AAPL GOOGL NDQ SPY DJIA IWM QQQ VIX XLK

{kind=link}