Equities recaptured much of what they had lost from Wednesday’s market rout on Thursday, but those gains look fleeting now after revenue misses from the likes of Amazon (AMZN) and Alphabet (GOOGL). U.S. equity futures are sharply lower ahead of the opening bell on Wall Street after the two tech titans failed to perform. Shares of GOOGL fell 4% in Thursday’s extended session after posting better-than-forecast earnings, but a revenue miss. Amazon posted a record profit, but sales disappointed, and more importantly its forecast for 4th-quarter sales was below analyst expectations. Shares of AMZN plunged more than 7% in late trading. The two mega-cap stocks will likely serve to cast a dark shadow over the market on Friday and ahead of key economic data.

While earnings continue to come in better than expected, doubts continue to rise as it pertains to the earnings picture for 2019. A series of rising concerns is weighing on investors and the market is pricing those concerns in now, rather than trusting that all will remain on track with the economy and corporate earnings. As such, risk-off has a greater probability in the coming days and weeks.

One of the ongoing market concerns centers on U.S./China trade relations, which have undergone several talks, but found without an amicable solution. On Thursday, U.S. officials reportedly said trade talks with China won’t resume until Beijing comes up with solid proposals over forced technology transfers and other economic issues.

According to the Wall Street Journal, the impasse threatens to undermine a meeting between President Trump and President Xi Jinping of China that is scheduled for the end of November at the Group of 20 leaders summit in Buenos Aires. Both sides had hoped the gathering would ease the trade tensions. U.S. businesses have been counting on sufficient progress at the meeting for the Trump administration to suspend its plan to increase tariffs on $200 billion of Chinese imports to 25% on Jan. 1, from the current 10%. Such a move would be a blow to U.S. importers and consumers.

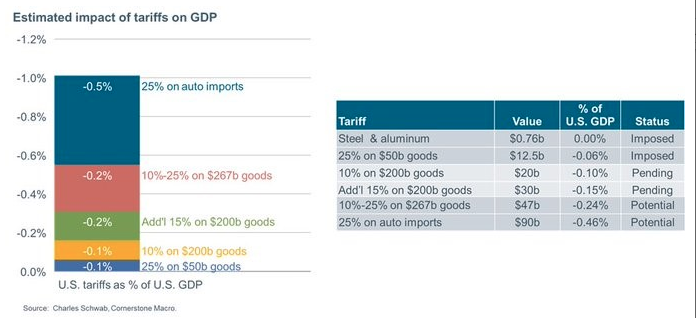

As you can see from the chart below, tariffs are expected to hurt GDP by 1% going forward, with the 25% tax on auto imports having about half of the impact.

This doesn’t seem like a huge impact, but GDP growth probably would have only been about 2% in 2019 considering the understood nature of GDP slowing in the future. This darkening outlook on 2019 might be the catalyst for the stock market volatility in October, which finds the equity market pricing in the potential slowdown.

Without trade feuds easing on the horizon, investors are still hopeful that interest rate increases might be halted in the near term. But this notion had some cold water thrown upon it on Thursday as well and with a speech from the FOMC’s Vice Chairman. The best way forward for the U.S. central bank is more interest-rate hikes, said new Federal Reserve Vice Chairman Richard Clarida, on Thursday in his first public remarks since taking office late last month.

“If the data come in as I expect, I believe that some further gradual adjustment in the federal-funds rate will be appropriate,” Clarida said in a speech prepared for delivery to the Peterson Institute for International Economics.

Through Thursday’s close, the Dow and S&P 500 were down 5.6% and 7.2% for October, respectively. The Nasdaq, meanwhile, had lost 9.1 percent. The losses are looking to be extended in the early hours on Friday. The state of market sentiment has definitively worsened with volatility on the rise. Although more downside in the market is now likely, given the market weight of Amazon and Alphabet, here is what CNBC’s Jim Cramer has to say about the potential market moves ahead and what investors should consider.

“Nobody’s talking about a recession. This is not the end of the world, which … you would think it was when you looked at yesterday’s action. There’s no systemic risk. The economy might go from really good to really mediocre.

We’re talking about a slowdown that reverses much of the economy’s recent growth and causes rounds and rounds of layoffs. Maybe our [gross domestic product] decelerates. Maybe it goes from 4 percent to 1 or 2 [percent], thanks to the lack of demand for autos, housing, construction and so many other industries — plastics, paper. That could easily be in the cards. What’s not in the cards is another full-blown recession, even though many were worried that Wednesday’s market wide nosedive signaled more pain to come.

This is not some sort of rehash of 2007, where, by that point, a crash was inevitable,” Cramer argued. “It’s more like 2006, or at least a much healthier version of 2006 when it comes to balance sheets, where the crash still can be averted if our leaders know what they’re doing. Let’s hope the president and the Federal Reserve do a better job this time around.”

Finom Group tends to agree with Cramer, a 2007-2008 market crash and great recession is unlikely given the current state of the economy and forecasts for the economy and corporate earnings in 2019. Remember, the beat rate for corporate earnings remains above its historic average with over 80% of reporting corporations having beat earnings estimates in Q3 2018. If a recession is to hit the economy, it is likely to be a shallow one that reverts to expansionary conditions rather quickly. Having said that, the fact that these conversations and concerns are happening and occurring is a signal that the bullish sentiment for both the economy and the market are deteriorating in the final quarter of 2018. That is simply where we are in the cycle and we must acknowledge it for what it is.

Moreover, Finom Group believes it would be advantageous for investors to pair risks for the time being and until market sentiment decides on its year-end path. While we believe the S&P 500 will finish higher than where it is going into Friday’s trading session, it may find itself deteriorating firstly and before it stabilizes for a higher move into the end of the year. Hedging or taking down risk in the interim is simply prudent, active portfolio management that offers to the investor more time with less capital drawdowns. If the market falters, the damage is lessened; if the market bucks the sentiment and heads higher, only time is lost.

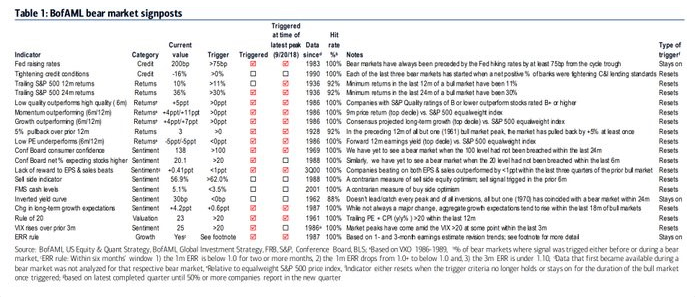

Volatility may continue to rise on Friday, providing another element of bearish market sentiment and prove to exacerbate market declines. When assessing the possibility of a more protracted downturn in the market and the inevitability for the bull market to end, we turn to the Bank of America Merrill Lynch bear market signpost list. In September, 13 out of 19 signposts were triggered.

As you can see from the table below, now 14 are triggered. This percentage of signposts was reached earlier in the year as well, but the market recovered and found new record level highs. Keep this in mind as not all signposts prove a guide for the future as this current bull market cycle has expressed many anomalies and records. Having said that 13 of the signposts were triggered at the time of the peak on September 20th.

The VIX being over 20 presently is a new trigger. “Trailing 12-month S&P 500 returns above 11%” has been taken off the board as a trigger. Bullishness in the Conference Board survey being above 20 is a new trigger. The rest are the same.

According to Bank of America, when a similar percentage of signposts are hit as compared to the current amount, there is an average of 21 months until the bull market peaks. That’s actually good news and suggests that even though the market may prove to deteriorate in the coming weeks, the bull market may not have peaked. 4 out of 7 bull markets have peaked with 100% of the indicators triggered.

While the market moves are likely to worsen before they improve and begin to reflect the growth in corporate earnings, some analysts remain focused on the longer-term outlook for equities. Here are the 5 listed takeaways from “October’s Wild Ride” according to LPL Financials latest research report:

The bad news.

- The S&P 500 is down 8.8% month to date, which would make this the worst month since February 2009 and the worst October since 2008 if it finishes the month at its current level.

- After not posting a daily move of more than 1% throughout the entire third quarter for the first time since 1963, this month has already seen six days out of 18 (33%) close at least 1% higher or lower.

- The S&P 500 has been down 14 days so far in October, the most for any month since May 2012. Also, 78% of the days this month have closed in the red (14 of 18), the worst for any month since 82% of days in April 1970 closed down.

Now, for some good news.

- Since 1950, there have been seven other years when the S&P 500 was positive year-to-date at the end of September, but fell negative year to date at some point during the month of October. The final two months of those years were higher six times and up 4.1% on average.

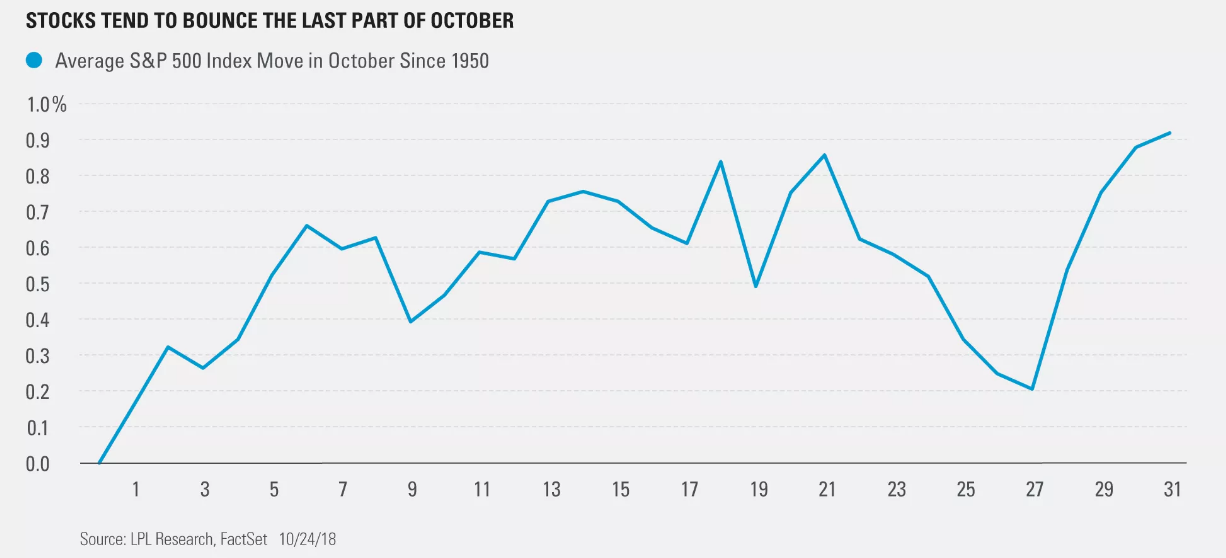

- Historically, the last few days of October have been some of the strongest of the year. With markets looking extremely oversold, the stage could be set for a rally.

The most fundamental truism about the equity market is that without a recession, bull markets persist. Recessions are what normally kill bull markets and a recession is not likely for at least a year, if not more. Given the aforementioned, the current sell-off gives investors a chance to buy stocks at better valuations. Do you really think Amazon is not going to beat its 4th quarter revenue guidance? This is a company that can turn on and off the spicket as it chooses and has done so throughout it’s history.

“We were particularly impressed by the continued YoY operating margin expansion, which is consistent with our view the company has transformed into a ‘profit machine,’ driven by multiple tailwinds (most notably AWS, which posted an over 30% operating margin for the first time),” Loop Capital’s Anthony Chukumba said in a note published on Thursday.”

With this in mind, the near term market reaction to not just trade concerns and interest rates that is being compounded by Amazon’s revenue miss, should prove short-lived. Dip buyers should find opportunity from lower market valuations that prove irresistible with an economy that is still expected to grow some 3% in 2018, providing a 3.3% GDP in the 3rd quarter alone. To reiterate, we are not in a recession and a recession is not foreseeable until at least late 2019.

“The economic fundamentals remain favorable,” said Bruce Bittles, Robert W. Baird’s chief investment strategist, after Wednesday’s sell-off. Bittles was also cautious on stocks ahead of the current rout. “Given the strength in the labor markets and confidence levels among small businesses, the odds of a business turndown are unlikely. We remain bullish on the U.S. economy.”

While the bull market has aged and may prove to be in its latter stages, as typically identified with rising volatility, active portfolio management may prove the key to investor returns. Having said that, here are some things traders can do to minimize the stresses from the forecasted volatile market moves.

- DO NOT stare at the price every single hour. Up 10 points, then down 20 points, then up 15 points, then down 30 points, then up 35 points. Do not let the market’s recent direction drive your thinking and actions. Always consider the long term in favor of the short-term.

- Focus on longer-term risk:reward. Can the market fall more in the short term? Of course it can, it has actually in October. Anything is a possibility because there is no such thing as 100% certainty in the markets. Possibility should never be considered over probability in the equity markets. What matters most is probability and risk:reward. If the market has a short term max downside risk of 5%, and an upwards target of 10%, that is a 1:2 risk reward ratio. As such, the active portfolio manager may pair risk and/or hedge, but not necessarily eliminate holdings.

{kind=link}