Yesterday’s Fed minutes proved market moving. Prior to the release of the Fed minutes, the major U.S. equity indices were trading lower with the Dow off greater than 100 points. That all changed once investors were able to look inside what the Fed was considering for its rate hike path and why. Let’s now take a look at what the minutes spoke to in terms of the Fed’s 2% inflation target and economic growth as extrapolated from the minutes.

“A few participants commented that recent news on inflation, against a background of continued prospects for a solid pace of economic growth, supported the view that inflation on a 12-month basis would likely move slightly above the Committee’s 2 percent objective for a time,” the minutes said. “It was also noted that a temporary period of inflation modestly above 2 percent would be consistent with the Committee’s symmetric inflation objective and could be helpful in anchoring longer-run inflation expectations at a level consistent with that objective.”

The Fed uses the personal consumption and expenditures data as its primary source to gauge inflation. The index has been rising and currently is at 1.9%, while the headline rate including energy and food prices is at 2 percent. The PCE is expected to rise above 2% in the coming months. Fed officials described wage pressures as “moderate” with tightening in certain industries.

Also within the Fed minutes was the dedication toward continuing to raise rates. A gradual approach to raising rates was maintained within the minutes. The next gradual rate hike is likely to take place at the June FOMC meeting.

“Most participants judged that if incoming information broadly confirmed their current economic outlook, it would likely soon be appropriate for the Committee to take another step in removing policy accommodation.”

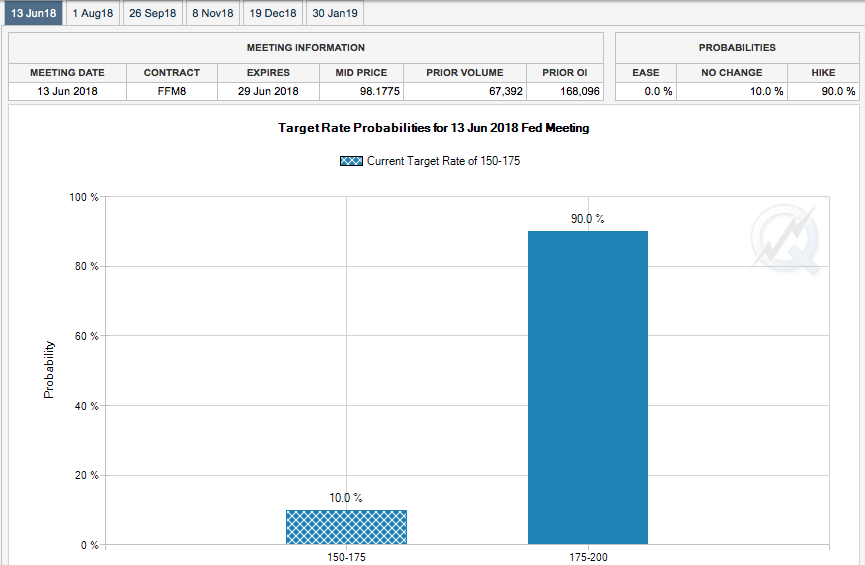

The market is already pricing in a near 90% chance of a Fed rate hike for the June meeting according to the CME’s FedWatch Tool.

As it pertains to the economy, the Fed’s outlook remains positive despite some softness in the Q1 2018 period. Committee members said they expect continued progress in the economic conditions. There was concern expressed over trade and fiscal issues, with Fed business contacts expressing “concern about the possible adverse effects of tariffs and trade restrictions, including the potential for postponing or pulling back on capital spending.”

“They noted a number of economic fundamentals were currently supporting continued above-trend economic growth; these included a strong labor market, federal tax and spending policies, high levels of household and business confidence, favorable financial conditions, and strong economic growth abroad.”

So here is the biggest takeaway when it comes to the Fed’s minutes: The Fed realizes that the economy will be strengthening in the coming quarters and as tax reform sets in, wage inflation, consumption and expenditures, commodity prices also take hold. While in a vacuum inflation/reflation seems harmful to an economy, the fact is that these elements of consumption and reflation are necessary components of a strengthening economy. The Fed is aware that such reflation and tightening in the labor market at this stage of the economic cycle is somewhat of an anomaly and thus needs to adjust its reaction to achieving its inflation target without stalling out a growing economy. By announcing that a temporary period of inflation modestly above 2 percent would be consistent with the Committee’s symmetric inflation objective and could be helpful in anchoring longer-run inflation, the Fed strategically curbs economists fears about accelerating rate hikes in the mid-term and allows itself to raise rates gradually. Essentially, this could take the speculated 4th rate hike off the table in 2018.

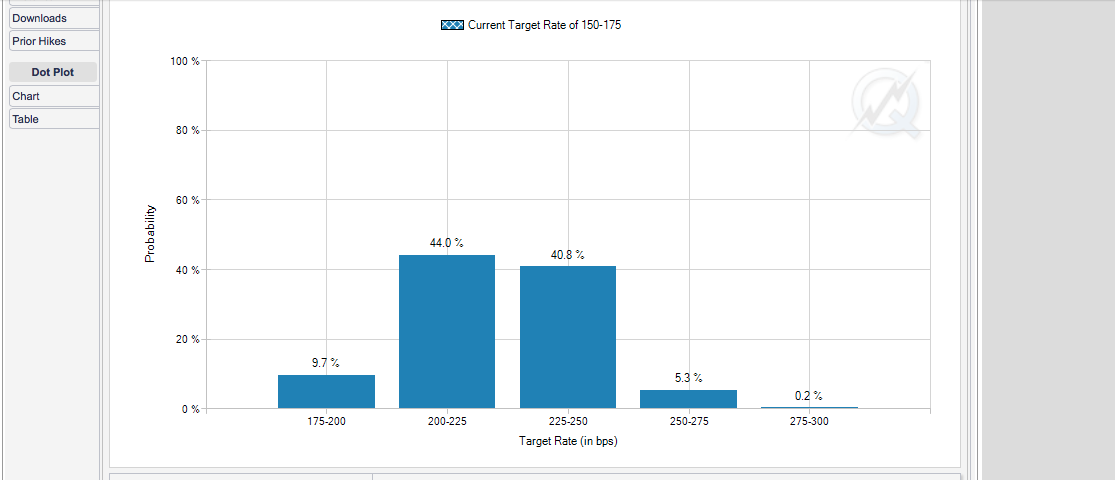

Prior to the Fed minutes, there had been a great deal of consternation surrounding the possibility of the Fed accelerating rate hikes given that the PCE would achieve 2% near term and probably rise above that rate thereafter. The CME’s FedWatch Tool at one point indicated a 50% probability of a 4th rate hike to occur in December, partly due to this inflation data. Just before the Fed minutes and over the last 30 days, the December Fed Funds contracts pointed to a 40.8% chance of a 4th rate hike as seen in the photograph below.

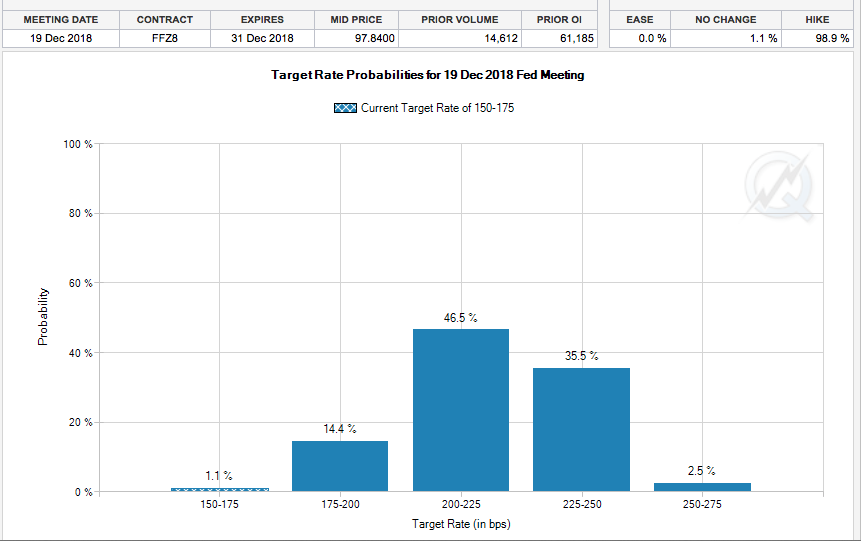

Moreover, right after the release of the Fed minutes, denoting that the committee members would agree to a temporary period of inflation above the Fed’s 2% target, the December Fed Funds contracts showed a decline in the probability of a 4th rate hike. As of May 23rd, the day after the Fed minutes were released, that December contract has fallen even further as depicted below.

The December contract now suggests a 35.5% probability of a 4th rate hike in 2018. This is the lowest probability in nearly 2 months and since inflation expectations have risen. The equity markets responded favorably to the Fed minutes largely because the fears of a 4th rate hike have subsided…at least for the time being. If the Fed sticks to the newer sentiment concerning inflation/reflation, it could prove very favorable for risk-on appetite. Even though the Fed is signaling a change to it’s “accommodative” language, it is still behaving in an accommodative manner regarding the pace of rate hikes.

From one month to the next, it proves important to study the Fed’s language as an investor. The Fed has driven a great deal of sentiment and activity in the equity markets since the financial crisis by way of its Quantitative Easing practice. In the newer era of Quantitative tightening that began in late 2015, investors are still supported by Fed policy, but to a lesser extent and as the Fed unwind its balance sheet. The process itself is historically unique, but will continue to grab investor intention.

Tags: SPX VIX SPY DJIA IWM QQQ TLT

{kind=link}