If you’re just waking up to seeing U.S. equity futures up by more than 1%, you’re likely in a better mood than last week, when markets ended the week with the major averages down more than 1 percent. It’s been one thing after the other causing markets to decline since February. But this week marks the end of the quarter for traders and one that will find portfolio managers rebalancing and hoping for a better 2nd quarter performance for the markets. That’s right, this is the last trading week of the quarter, so traders should expect volatility in equities this week or should I rather say a continuation of volatility. The VIX, after all, ended last week at 24.87, but like equity futures rebounding, the VIX is relaxing somewhat and is presently down 7% in the premarket.

The chart below, offered by the J.P. Morgan’s quant team, is an overlay of the August 2015 sell-off and the February 2018 sell-off in flow terms. As one can see, the current market flow has a similarity with the August 2015 sell-off.

Back in 2015, this greatly impacted the short-VOL trade forcing covering of short volatility positions, momentum triggered CTA outflows, and dealers’ option gamma prompted selling of futures. These outflows happened at a time when electronic (high-frequency) liquidity in index products collapsed. The similarities between the flow and market sell-off then are remarkable when compared to the present flow and market sell-off.

What typically happens during such market sell-offs that don’t warrant or accompany a recessions is that short-term momentum returns to the markets. The causation of this market cycle is due largely to short-term options expiring within a 1-month cycle and realized volatility starts declining prompting volatility sensitive investors to renew buying activities. This all happened in 2015 and has been happening during certain periods of March. We’ll have to wait and see if 2018 more precisely mirrors the August 2015 market sell-off and volatility spike.

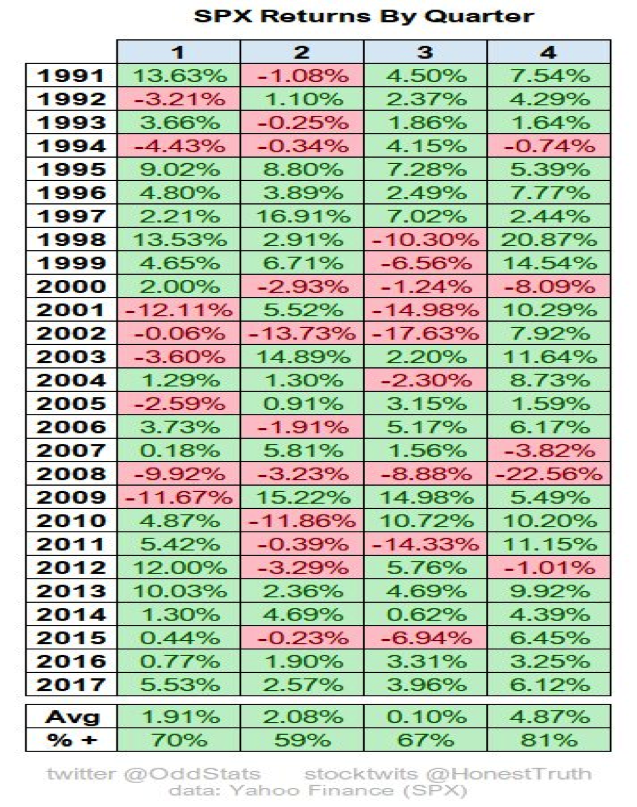

The bad news, regarding Q1 is that the quarter is expressing declines for the S&P 500, the broadest index. The benchmark index is currently down by more than 3% for the quarter. If the index does not offset this decline in this shortened, holiday trading week, it will mark the first decline for the S&P 500 on a quarterly basis in the last 9 quarters. The good news, however, is that following a negative 1st quarter, the S&P 500 has only had a negative 2nd quarter on 3 occasions since 1991 as displayed in the table below presented by Yahoo Finance.

The benchmark index currently trades at 16.5 X forward earnings, down from an 18.6 X multiple at the end of January when it last hit record highs. Such valuation is still less than that expressed during the dotcom bubble era when the S&P 500 traded as high as 25.8 X earnings. So when market pundits claim the index is overvalued that may be the case historically, but it fails to encompass perspectives beyond historical median valuation for the index and as earnings are currently expected to grow in the mid-teens for 2018.

From rates rising, a more hawkish Fed, a cascade of advisors and officials leaving the White House, Presidential tweets to trade wars, the markets have been tremendously resilient… up until recently. As it was in February, the markets find catalysts in an era of stretched valuations to curtail momentum and in February, wage inflation was the catalyst for a market correction. In March, rationalizing a lack of inflation or the realization of moderate reflation had left markets range bound between double bottoming and seeking all-time highs. In the last two-weeks, however, the SPX found its reasoning for risk-off measures as trade war fears usurped all else. Finom Group discussed these trade war issues surrounding President Trump’s trade tariff proclamations in a recent article titled “Trade War: To Be Or Not To Be…” The article was titled as such because the likelihood of an actual trade war was limited. Moreover, for all of the panic in markets last week, no actual tariffs had been put forth and the President’s former tariff proclamation on steel and aluminum had all but been walked back to non-existence. The following excerpt was taken from the article:

“The risk-off trade is in affect as the major averages fight through this correction period and in search of stability. What we know lay beneath these trade fears is a strong global economy. U.S. corporations are expected to grow earnings in the mid-teens through 2018 with the S&P 500, Q1 2018 earnings expected to grow some 18 percent. Right now, however, many investors fail to see the forest through the trees as they say. But it’s important to recognize one critical fact: NO TRADE TARIFFS HAVE BEEN IMPLEMENTED, JUST PROCLAIMED!”

In discussing the market pullback, Scott Wren, senior global equity strategist at Wells Fargo, told CNBC’s “Futures Now” recently that, “We think this thing still has some upside the rest of the year.” Wren recognized that corporate earnings and a strong consumer are supporting global equities. When discussing the trade war fears he offered the following:

“This is going to be on the front burner for the next couple of years,” he said. “I just really think this is not going to be an all-out trade war, but obviously the market is worried about that and certainly if that would happen that wouldn’t be a good thing.”

Wren also answered questions for CNBC’s Futures Now regarding Fed rate hikes. He suggested that the Fed is not behind the curve and believes that 4 rate aren’t warranted in 2018 and would likely be a mistake. Wren is bullish on the stock market despite the correction. He reiterates his midpoint price target on the S&P 500 at 2,850 for the end of the year. A finish at that level marks a 6.6% advance for the year.

What’s comical about a 9-year old bull market is that investors believe that age justifies the means. By that I mean due to the longevity of the bull market and above historical mean valuations, investors look for excuses to justify profit taking and selling equities. The more that investors look for such reasons, even the hint of possible reasons are jumped on/to quickly. Such was the case with the wage inflation data from the January Nonfarm payroll report and such is the case presently regarding the possibility of a trade war. But for some reason and all of a sudden, over the weekend, more rational thinking has prevailed and surrounding those trade war fears. As I offered last week at what may prove to be the height of such fears (remains to be seen), a trade war is unlikely, improbable and cooler heads are likely to prevail if we are to believe in “The Art of the Deal” that is the trademark of the U.S. President. This is not a trade war, this is a negotiation that finds the tactics being put forth in the negotiating process… less than the norm, to put it politely. Many have come to the conclusion or pushed to the forefront over the weekend that it is in nobody’s best interest to initiate a trade war and the rhetoric has turned toward the understanding that “behind the scenes” negotiations are taking place between China and the United States. It the recent China Development Forum, Stephen Schwarzman of the Blackstone Group offered his take on the trade war rhetoric and fears.

“Most of the type of things being discussed by the U.S. side can be delayed in terms of their implementation, and hopefully will be,” said Stephen Schwarzman, CEO of Blackstone Group, which had $434 billion in assets under management at the end of 2017.

I anticipate that rational people will be able to come to a really good solution,” he told CNBC at the China Development Forum on Saturday. “There’s an opportunity to accelerate the efforts of both countries to find an equitable solution.”

China’s officials have already stated that they are willing to hold trade talks with the U.S. and this may provide some degree of relief for equities near term. For certain this week’s trading remains…uncertain, especially as it encompasses fewer trading days and the end of the quarter. Fundamentals have given way to fear and pessimism over the last two months of the quarter and some economists have curbed their enthusiasm for Q1 2018 growth prospects. Investors and traders will get the final look at Q4 2017 GDP this Wednesday, which shouldn’t change all that much from the previous reading. The big report or data point this week will come on Thursday by way of the Personal Consumption and Expenditures data or PCE. This is the Fed’s key measure of inflation on the economy and will be carefully considered by investors as it pertains to the potential for 4 rate hikes this year.

Below is the trimmed mean PCE. It is likely the best measure of inflation in my, as takes out the top and bottom outliers. The Fed desires to see 2% inflation but that is not being expressed through the PCE, at least not yet. Having said that, the Fed has raised its expectations for inflation in 2018.

As we look forward to a more constructive week in the markets, we reflect on last week’s S&P 500 chart.

As shown in the chart, the S&P 500 held its 200 DMA, closing just above it. Will the 200 DMA prove to support the index near term? Most attempts for the market to rally in the last month have been sold-off. But maybe history will prove to find a negative Q1 S&P 500 performance followed by the more usual positive Q2 performance.

Tags: SPY DJIA IWM QQQ

{kind=link}