Although it was only a one-day layoff with the markets closed for the 4th of July, it seems like headlines continued to roll in regarding global trade. The most significant or positive headline may have come out of the European Union. European officials are considering holding talks on a tariff-cutting deal between the world’s largest car exporters to prevent an all-out trade war with the U.S., according to the Financial Times who cited diplomats briefed on the matter. The European Commission “is studying whether it would be feasible to negotiate a deal with other big car exporters such as the U.S., South Korea and Japan.” Such a move could address Trump’s complaint that the U.S. sector is unfairly treated, while reducing export costs for other participating countries’ auto sectors.

The proposed talks by the EU have seemingly proven to elicit a positive response from U.S. officials. A U.S. official said the U.S. would be prepared to stop threatening to impose stiff tariffs on cars imported from the EU if the bloc eliminates duties on U.S. cars, according to a report by German newspaper Handelsblatt, citing unnamed sources.

The other headline, by Reuters, was equally negative for global trade. China warned that the United States is “opening fire” on the world with its threatened tariffs. Chinese officials said they will respond the instant U.S. measures go into effect. China has said it will not “fire the first shot”, but its customs agency made clear on Thursday that Chinese tariffs on U.S. goods would take effect immediately after U.S. duties on Chinese goods kick in.

Speaking at a weekly news conference, Commerce Ministry spokesman Gao Feng warned the proposed U.S. tariffs would hit international supply chains, including foreign companies in the world’s second-largest economy.

“If the U.S. implements tariffs, they will actually be adding tariffs on companies from all countries, including Chinese and U.S. companies. U.S. measures are essentially attacking global supply and value chains. To put it simply, the U.S. is opening fire on the entire world, including itself.”

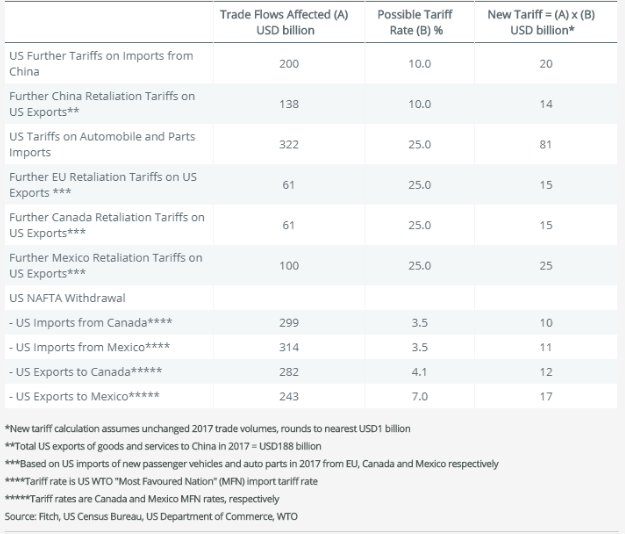

Last, but certainly not least is the warning from Fitch Rating. Fitch Ratings warned that rising tensions between the U.S. and its trading partners could lead to new measures with a greater impact on global growth with as much as $2 trillion in global trade in jeopardy if President Donald Trump remains on a trade warpath.

“The U.S. investigation into auto tariffs, possible additional U.S. tariffs on Chinese imports, and the likely reactions of other countries and blocs, point to a potential serious escalation, albeit with an impact that falls short of across-the-board tariffs imposed on all major trade flows,” Brian Coulton, chief economist at Fitch, said in a report.”

Despite all the trade rhetoric, be it positive or negative, European equities are higher and leading U.S. equity futures higher in the early morning hours. This could quickly change depending on the news cycle, as investors seem overly concerned about the next trade headline when compared to corporate earnings. Most importantly for U.S. equity investors today will be economic data and FOMC minutes.

ADP employment data will be released at 8:15 a.m. EST today. The data is expected to show that the U.S. labor market remains healthy, growing jobs month-to-month at a strong rate. Of even greater interest to investors outside of the trade spat may be the FOMC minutes. The Fed minutes are expected to be released at 2:00 p.m. EST today and with some investors and economists of the opinion the Fed may need to pause its hawkish rate hike trajectory for 2018.

At the June meeting, the Fed raised the target range for its benchmark policy rate to between 1.75% and 2% and made changes to its statement and economic projections that were hawkish relative to expectations, said Jan Hatzius, chief economist at Goldman Sachs. The central bank projected four rate increases in 2018 instead of three previously planned.

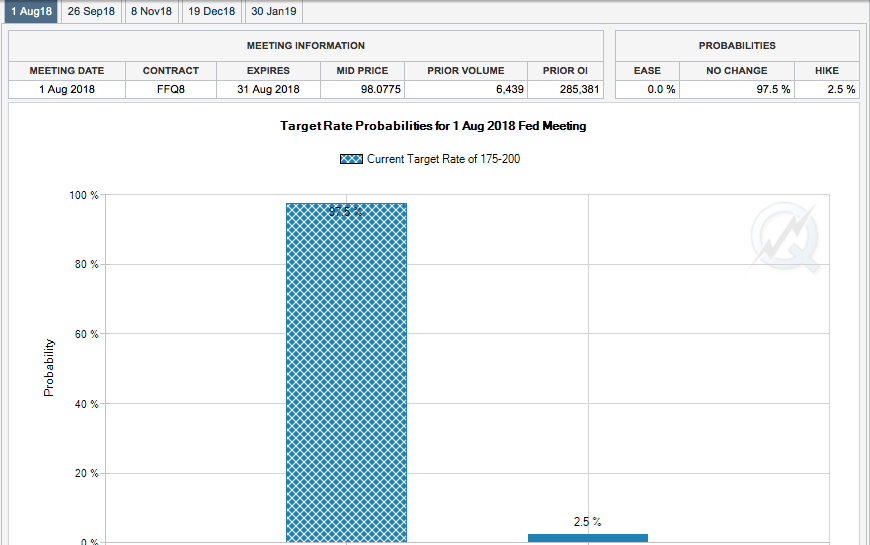

Economists will be looking closely to see how much pushback there was at the last meeting from doves and also for clues as to what it could take for the Fed to deviate from its current pace of lifting rates. Future rate hikes are expected to take place in August and December of 2018. According to Fed fund contracts and the CME’s FedWatch tool, an August rate hike is already priced into the market with an expected rate of 97 percent as shown below.

Michael Hanson, head of global macro strategy at TD Securities, thinks the Fed is locked in.

“The June FOMC minutes are likely to reflect the ‘great’ economic outlook summarized by Powell during his press conference, and thus have an on-net optimistic tone.”

Joe Lavorgna, chief economist for the Americas at Natixis, is hoping that some Fed officials make a strong case for slowing down interest-rate hikes because the yield curve is flattening, with the spread between 2-year notes and 10-year notes near the lowest level seen since 2007.

While we will continue to hear a great deal more concerning global trade and the potential for a trade war, the U.S. economy is still growing at its fastest pace in several years. Furthermore, the U.S. economy is less prone to economic declines or curtailed economic activity from trade issues than its trading partners around the globe. In other words, while other economies around the world are witnessing slowing growth, this should not affect the U.S. economy to the extent the media suggests investors pay attention to the subject matter.

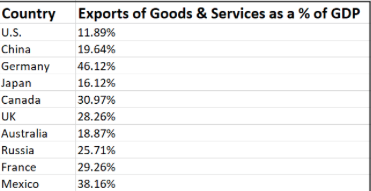

As shown in the chart above, the U.S. simply doesn’t export as much as other nations and therefore doesn’t depend on the demand from those national economies to support the United States’ economy. It’s the emerging economies and national trading partners that rely on U.S. demand. This fact is another reason that as emerging equity markets have been falling sharply, with China expressing a bear market for equities presently, the U.S. stock market has seen less impact from the current trade spat.

Although U.S. equity futures are gaining strength in the 6:00 a.m. EST hour, the market may prove quite volatile Thursday as economic data rolls in ahead of the likely imposed tariffs on $34bn worth of goods from China on Friday. Also of importance come Friday, for investors, will be the Nonfarm Payroll report.

With the potential for markets to express heightened levels of volatility, Finom Group continues to trade what the market delivers daily and weekly. On the shortened trading day this past Tuesday, Apple Inc. (AAPL) proved to be a positive intraday trade ahead of the news on Micron.

As shown in the screenshot above, we were able to alert our subscribers regarding this AAPL trade that was profitable intraday. Near term and with AAPL shares haven fallen further since the completion of this trade and ahead of earnings season, we’ll be looking for additional trading opportunities with shares of AAPL. Additionally, the greater volatility in the market place that has persisted through much of 2018 thus far will likely breed opportunities to short the volatility ETP complex throughout the year.

Tags: AAPL SPX VIX SPY DJIA IWM QQQ TVIX UVXY VXX XRT

{kind=link}