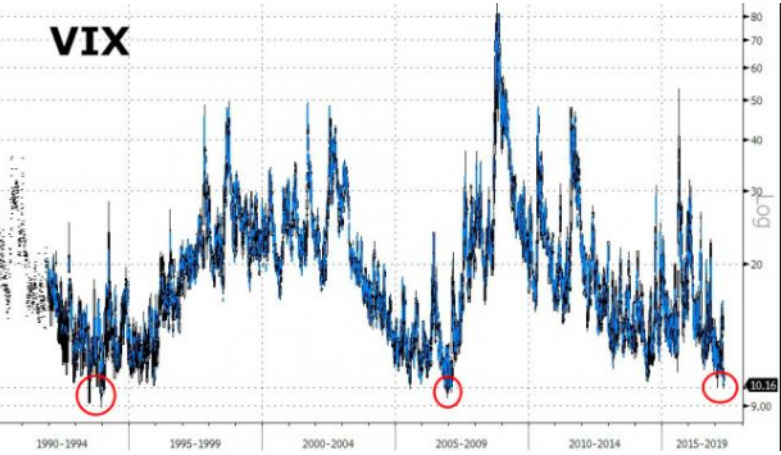

It’s Thursday January 18, 2018 and we are just shy of hitting the debt ceiling and in need of resolution and an agreement from the Federal government. Republican leaders are scheduled to bring forward a short-term spending bill to keep the government running through mid-February, The Wall Street Journal reported. The uncertainty surrounding a resolution to fund the government has created heightened levels of fear in the market, driven by outsized protection through cheaper VIX options over the last several trading sessions. The VIX is currently hovering around 12 and up significantly in the New Year. It may seem a contradiction to cite VIX 12 as being up significantly, but with the median VIX average being just 11.10 in 2017… it proves fitting.

Earnings in Favor

This week we’ve encountered more of the big-bank earnings, which continue to come in, largely, ahead of expectations. Morgan Stanley is set to report its quarterly results. The FactSet analyst consensus for Morgan Stanley is for per-share earnings of 64 cents, down from 81 cents a year ago, but revenue of $9.2 billion, higher than the $9 billion booked a year ago. The mean stock rating is overweight, and the price target of $58.08 is about 7% higher than its price in trading on Thursday.

Next week is a more powerful earnings week with respect to the S&P 500, as some of the bigger tech titans will be reporting their quarterly results. Netflix will be reporting on January 22nd and is coming off of a rather strong report in the most recent earnings season. Expectations are high for Netflix as all indications are that earnings will be strong yet again. Netflix has forecast 6.3 million additional subscribers, which would be another record.

Qualcomm Inc. will be reporting on the 21st and has had its share of difficulties over the last two years. Over that period it has underperformed the iShares PHLX Semiconductor ETF that is up 48% in the last 12 months. Of course, a good deal of the underperformance is due to its troubled relationship with Apple.as well as an unfavorable rulings and fines from regulators overseas. Having said that, QCOM stock has surged 30% since November due to renewed optimism surrounding the hostile bid from Broadcom.

On the final trading day of the month, Facebook will be reporting its Q4 2017 results. Facebook Inc. has been languishing for much of the last 90 days and since it last reported quarterly results. More recently, shares have plunged back below $180 a share on the announcement that it will be making some changes in user news feeds. Stifel thinks Facebook’s planned News Feed changes are the correct move for long-term sustainability, but shares will struggle until the economic implications of the change become clearer. The firm reiterates Buy rating, though with less conviction at the moment, and a $195 price target, which is 9% above yesterday’s close. In the coming earnings report, investors will be focused on how the social media portal may change going forward.

How great would it be to kick off February with an Apple Inc. earnings beat? Well Apple is set to report and while the firm may in fact beat, the guidance will be critical to the stock’s performance, especially with all the scrutiny and uncertainty surrounding the handset makers iPhone X. The iPhone X went on sale in November to reasonably good buzz, but not without supply-chain issues. There were fears that initial demand may not have been met in December, so it will be important to see whether Apple delivers. Investors will also be interested to hear directly from Apple the company’s plans for higher dividends and a more aggressive buyback strategy. The massive corporate tax cuts passed by Congress late last year is a boon to cash-rich profit machines like Apple, and Wall Street expects the tech giant to share its cash with shareholders. Wednesday the company said it planned to contribute $350 billion to the U.S. economy over the next five years, through new jobs, a new campus, and investments in data centers.

Looking Abroad

European stocks are modestly higher Thursday after the release of upbeat economic growth and industrial output data from China. Official figures showed the world’s second-largest economy grew 6.9% in 2017, beating Beijing’s target of 6.5 percent. Industrial output accelerated in December, but retail sales slowed. U.K. equities were in the red however, as traders continued expressing concerns about the health of the British real-estate market.

U.S. Markets

U.S. equity markets continue their torrid pace of outperformance with the Dow Industrial Average set to open at record levels above 26,100. Having said that, we’d continue to monitor treasury yields or the pace of the rise in treasury yields. At present, the 10-year Treasury yield is hovering at 2.6% and will finish for a second consecutive week above 2.45 percent. It would seem as though a rate hike in March is all but a certainty at this point and with equity markets already up 6% for the fiscal year.

Bitcoin’s spot price rose 0.2% to $11,165.89, after selling on Wednesday knocked it to its lowest level since late November, falling below $10,000. South Korea’s central bank governor, Lee Ju-yeol, said at a press conference on Thursday that cryptocurrencies weren’t “legal” currencies, and not being used in such a manner at present. This comes after some harsh rhetoric from China on cryptocurrencies over the last couple of days.

It has been a light week for economic data with a couple of minor releases due out today. Weekly jobless claims, along with housing starts and building permits for December, are all due out at 8:30 a.m. Eastern Time. The Philadelphia Fed’s manufacturing index for January is due at 10 a.m. Eastern.

Tags: IWM QQQ SPY VIX

{kind=link}

test