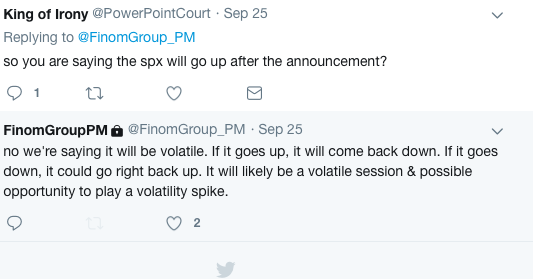

Ahead of the rate hike announcement that was delivered Wednesday afternoon, Finom Group had anticipated and forecasted the post announcement move to our subscribers, as shown in the following screen shot from our private Twitter feed.

After the end of a two-day meeting, the Fed increased its target for its benchmark-lending rate to a range of 2% to 2.25%. Rates are now at their highest level since shortly after the bankruptcy of Lehman Brothers in the fall of 2008. The markets did indeed initially take the rate hike well, but then came the press conference.

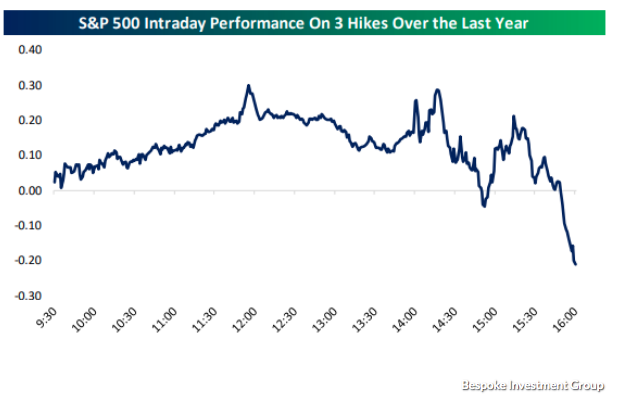

Yesterday and as it was with the previous 3 rate hikes, initially the markets traded well once the Fed announced its rate hike decision, but quickly reversed course thereafter and into the closing bell.

Along with raising rates, senior Fed officials dropped the long-standing language saying its stance on interest rates “remains accommodative.”

“This change does not signal any change in the likely path of policy,” Powell said. “Policy is still accommodative.”

The Fed’s dot plot showed that 12 officials now expect another quarter-point rate hike in December, up from eight officials in the last projections in June. Only four officials now pencil in a pause. The Fed continued to project t 3 rate hikes next year and one more in 2020.

As it pertains to the Fed’s updated economic forecast, the revised forecast showed the unemployment rate would start to rise in 2021 as its restrictive policy started to take affect. In the Fed’s forecast, economic growth will gradually decline over the next 3 years from a 3.1% annual rate this year to a 1.8% rate in 2020 and 2021.

According to the forecast, inflation will remain contained, with core personal consumption expenditure price index holding steady at 2.1% rate over the forecast period.

During Fed Chairman Powell’s press conference, he tried not to break too many market and political sentiments, staying as neutral as the Q&A, along with the data, would allow for him to remain. In doing so, Powell did recognize several questions related to the potential impact of tariffs on the economy, consumer and inflation forecast. While Powell did recognize a plethora of businesses raising concerns about the tariffs and potential impact, he downplayed the issue and even went so far as to so the Fed doesn’t see inflation going beyond the Fed’s forecast.

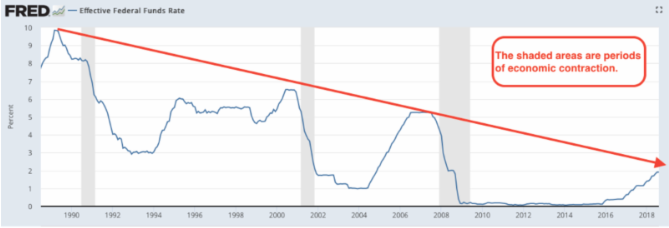

What’s most important to understand about the current rate hike cycle is found in the following chart.

The chart identifies that even though the Fed is raising rates during an expansion era, they are rising from historic low levels. As such, the Fed’s longer-term forecast is understood to still be accommodative, even as the word has been removed from its verbiage.

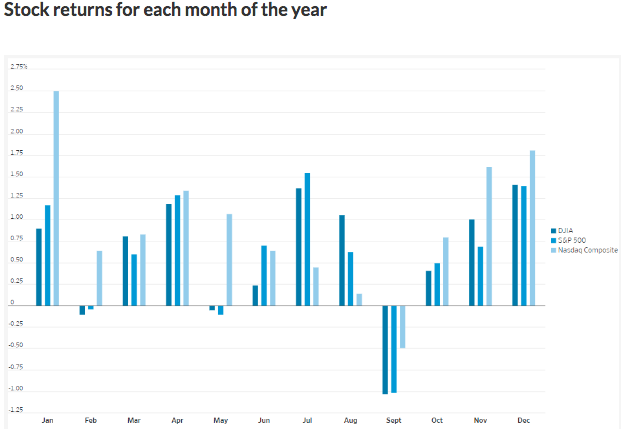

Shifting focus a bit here from the first ever September rate hike and end of quarter rebalancing season, we recognize that September is outperforming its historic trend of being the worst month of the year for stocks.

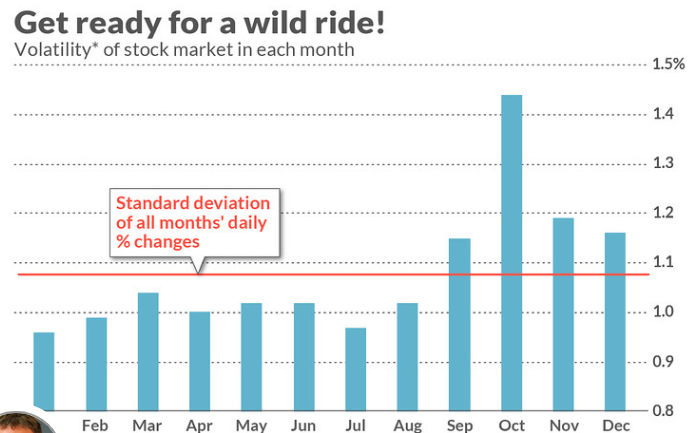

Before we jinx it, as there remains 2 more trading sessions, October is recognized for the start of Q3 2018 earnings season. And according to famed newsletter writer Marc Hulbert, investors should buckle in for what could be a wild ride ahead of mid-term elections.

According to Hulbert, the reason for the above average volatility in October is due to when bull markets have begun, on average. Of the 35 bull markets since 1900 in the calendar maintained by Ned Davis Research, 8 got their start in October. That’s twice as many as began in any of the 11 other months of the calendar.

“For longer-term investors, the investment implication is not to get spooked by October’s volatility. Chances are that it doesn’t represent the beginning of a new bear market. In fact, of the 35 bear markets on the Ned Davis Research calendar, only one began in October.”

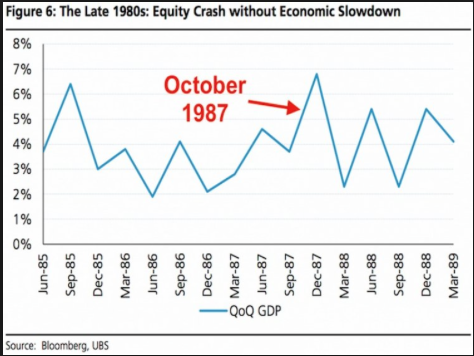

Of course, if we dig a little deeper into what has made October a difficult month for equities, we also recognize that several crashes did in fact occur in years past. According to the Stock Trader’s Almanac, there were “crashes in 1929 and 1987,” the Almanac read, along with “the 554-point drop on October 27, 1997, back-to-back nightmare scenarios that played out in 1978 and 1979, Friday the 13th in 1989 and of course the meltdown in 2008 that eventually became known as the Great Financial Crisis.

Although there have been a handful of years that characterize the month as a “jinx” month, the reality is that on average equities tend to perform well during October. Historically speaking, the Dow Jones Industrial Average rises an average of 0.6% over the month, the S&P 500 rises .9% over the month and the Nasdaq rises .7% over the month. While the aforementioned statistical performance is the average throughout history, midterm years tend to correspond with extremely strong Octobers, according to the Almanac. While the Dow rises 0.6% in October overall, it jumps a far stronger 3.1% in midterm years. The S&P climbs 3.3% in midterm Octobers, more than three times the average overall gain, while the Nasdaq jumps 4.2%, six times its overall average.

As we begin to butt –up against earnings season, some corporations are already delivering results. After the closing bell yesterday, Bed Bath & Beyond released its latest quarterly results that missed expectations across the board. Bed Bath & Beyond said it earned $48.6 million, or 36 cents a share, in the quarter, compared with $94.2 million, or 67 cents a share, in the year-ago period. Revenue was flat at $2.94 billion. Analysts polled by FactSet had expected earnings of 50 cents a share on sales of $2.96 billion. Same-store sales fell 0.6%, the company said. Bed Bath & Beyond “remains on track to achieve moderating declines in operating profit and net earnings per diluted share in fiscal 2018 and fiscal 2019, and to achieve growth in net earnings per diluted share by fiscal 2020” in connection with its 3-year financial plan, the company said. Oddly enough, this 3-year plan started in 2015 when its gross profit margin “situation” became increasingly alarming.

It was only 10 days ago that BBBY shares were upgraded at Raymond James. Analyst Budd Bugatch raised his rating to market perform, after being at underperform for the past 5 months. Bugatch said while the company continues to face compressing margins, his upgrade “simply underscores our view that sales results for F2Q18 now seem more likely to reflect a better consumer sales environment than previously expected, thereby mirroring the results for overall retail and other retailers have posted during late spring and summer.” With the stock underperforming the retail sector this year, Bugatch believed upbeat results will provided a “trading opportunity,” leaving a bearish rating now “too harsh.” Unfortunately, Bugatch’s upgrade proved erroneous.

Finom Group’s chief market strategist Seth Golden has been bearish on shares of BBBY since 2015. In 2016 he authored an article titled “Bed Bath & Beyond: Stay Away”. Since then he’s written a series of articles outlining the company’s continued deterioration of sales and profits.

“All you have to do is follow the path of gross margins in the retail space and for Bed Bath & Beyond that’s been a dire visual exercise, said Golden.”

The retail landscape over the last several years has been littered with fits and starts as well as “haves and have-nots”. Clearly, Bed Bath & Beyond is a “have-not”. The broader retail industry will perform well above the struggling home goods retailer when the category reports earnings results in November. Until then, Finom Group’s top picks in the retail sector remain Target (TGT), Wal-Mart (WMT) and Amazon (AMZN). For investors who desire a more diversified and passive way of investing in the retail sector, ETFs such as SPDR S&P Retail ETF (XRT) and Amplify Online Retail ETF (IBUY) may suit their investing style.

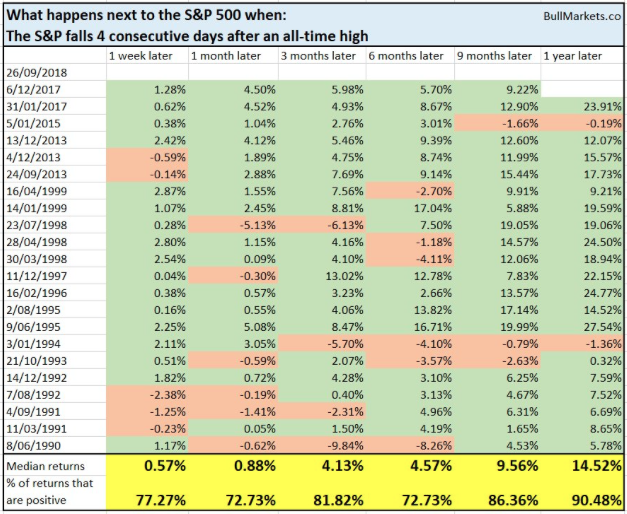

The S&P is experiencing a 4-day losing streak since reaching new all-time record level highs. According to Bullmarkets.co, here is what happened during the previous like occurences from 1990- present:

Lastly and with respect to Finom Group’s expectations for volatility in October, we will outline our thoughts in this weekend’s research report. Subscribe today and get early access to our research, insights, social sharing applications and trade alerts.

Tags: IBUY SPX VIX SPY DJIA IWM QQQ TLT TVIX UVXY VVIX VXX XLF XRT

{kind=link}