In our most recent research report (subscription required), we disseminated the weekly expected move for the S&P 500 starting the week of 11/12/18. As shown in the screenshot below, the weekly expected move is $50… and we got every bit of that weekly move in the very first trading day of the week.

The major averages dove on Monday with the Nasdaq (NDX) leading the declines, off by 2.7 percent. The Dow Jones Industrial Average (DJIA) fell 2.3% followed by a 1.97% decline in the S&P 500. So what happened on Monday that caused the steep market sell-off; take your pick!

Oil prices popped higher in the Monday morning trade as Saudi officials suggested a cut in OPEC oil production given the probability for a supply glut in the near future. Shortly after the Saudi verbiage, a tweet by President Donald Trump on Monday added to oil’s woes, as he voiced disapproval over a potential production cut by Saudi Arabia and OPEC, and said prices “should be much lower based on supply!” And that was all it took for oil prices to tumble. Another down day for oil will mark the 12th consecutive decline, the longest series of losses for the commodity since WTI started trading in 1983, according to Dow Jones Market Data. Monday marked an 11th straight loss for the contract.

Oil wasn’t the only variable weighing on equities Monday, as the U.S. Dollar was another key element causing angst amongst investors. The dollar index, which measures the greenback versus a basket of other currencies, jumped 0.7 percent on Monday to 97.58, a 17-month high. The USD has surged in recent months with global growth fears rising and a troubled Europe that is plagued by a Brexit and Italy budget fallout.

“It could be a challenge for the stock market in the fact that about 40 percent of the S&P 500 earnings are generated from outside the United States,” said Michael Arone, chief investment strategist at State Street Global Advisors. “As the dollar strengthens, that has certainly created risk to those earnings. Another thing that could be a risk is, as the global economy has been slowing this year, the rising dollar poses a problem for many countries outside the U.S., and that has contributed to the slowdown in growth. The question is whether the U.S. economy can withstand a slowdown in global growth, and I don’t think it can in the long run.”

While the media may portray the fears of a strong dollar and how that might clip earnings results going forward, the reality is that the USD has been stronger in 2016 and 2017. Investors tend to discount impacts from foreign currency exchange rates in quarterly earnings calls. Corporations know this and it offers them a line item to promote the effects of currency exchange rates when they deliberate earnings impacts so as investors understand the probabilities under more normal operations, not impacted to the same degree by currency exchange rates. In other words, investors have always forgiven impacts from currency exchange rates, as they tend to be a transitory impact.

The reasons to be bearish on the market near term seem to be growing and with trading sessions like the greater than 2% declines on Monday, the reasons seem quite formidable.

- Fears over slowing growth in China and around the world

- Fed Raising interest rates

- The ongoing tariff battle between the U.S. and its trading partners

- Midterm election results that saw the Democrats take the House

- Slumping oil prices caused in part by a drop-off in demand

- Possibility that S. corporate profits are peakingand likely will taper off in 2019.

- U.S. Dollar strength

“So much of it is going to depend on the tariff stuff,” said JJ Kinahan, chief market strategist at TD Ameritrade. “The market hates uncertainty. That’s the biggest cause of uncertainty. You’ve got the election settled, hopefully you have that settled by the end of the month.”

After the October market swoon, it seemed as if the risk-on trade was back en vogue. Between Friday and Monday’s market retrenchment, however, much of the risk-on sentiment has been washed away. This has left investors wondering what might rescue the markets from what seems an inevitable revisiting of the October lows. Keeping in mind that the S&P 500 finished Monday below it’s 200-day moving average, CNBC’s Jim Cramer suggested there were 7 key things that need to happen to stem larger market declines.

- A recovery in the stockof Apple, which led much of Monday’s declines after a supplier report implied weakening iPhone orders, would be the first key to a broader reversal.

- The FANG stocks, Facebook, Amazon, Netflix and Google, now Alphabet, also have to stabilize.

- The market would benefit if Federal Reserve Chairman Jerome Powell acknowledged that he was “winning the war against inflation. Ideally, that would happen at Federal Open Market Committee meeting in December.

- Any sign that China may cooperate with the Trump administration’s trade demands would give stocks a boost. The G-20 summit at the end of the month could be the deciding factor.

- The strong dollar seems unstoppable. “That’s bad for the earnings of most companies. So, despite the lower energy costs, the earnings estimates for next year are still too high.”

- The “flight to quality”on Wall Street also needs to end for the broader market to go higher.

- Finally, shares of General Electric, the closely watched industrial giant in the midst of a long-winded turnaround, need to reverse course

All but that last bullet point would find agreement with Finom Group’s assessment for curtailing market declines. Having said that, the Fed doesn’t meet again until late December and the G-20 summit isn’t until November 30th. As such, the markets may continue to be choppy, at best, until at least that time.

The bears are out in force and with market fears rising, the retail earnings season is taking a back seat at the moment. Nonetheless, Home Depot (HD) has reported Q3 2018 results ahead of the opening bell and beat estimates handily. The retailer also raised it’s sales outlook for the fiscal year.

Corporate earnings results from Macy’s (M) and Wal-Mart (WMT) will follow the do-it-yourself retailer in the coming days. Additionally, a read on monthly retail sales is expected from the Census Bureau on Thursday. Retail sales for October are expected to grow .4% from September.

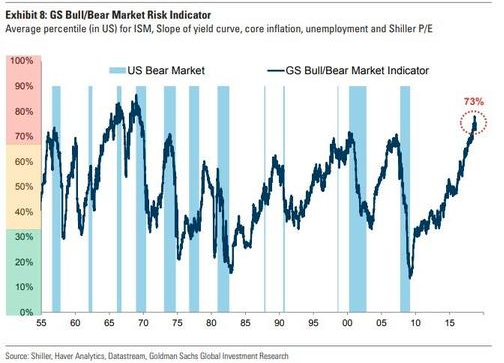

Given the numerous issues plaguing global equities and the declines around the globe, Goldman Sachs recent notes only exacerbate fears that the market is “on the verge”. The firm’s Bear Market Risk Indicator is presently in the 73 percentile.

Historically, when the Indicator rises above 60% it is a good signal to investors to turn cautious, or at the very least recognize that a correction followed by a rally is more likely to be followed by a bear market than when these indicators are low. By the same token, when the Indicator is very low, below 40% (as was the case in 1975, 1982 and 2009), investors should see any market weakness as an opportunity to buy.

According to Goldman Sach’s Bear Market Indicator, the risk of a bear market is near all-time highs. Investors may take caution given the risks noted.

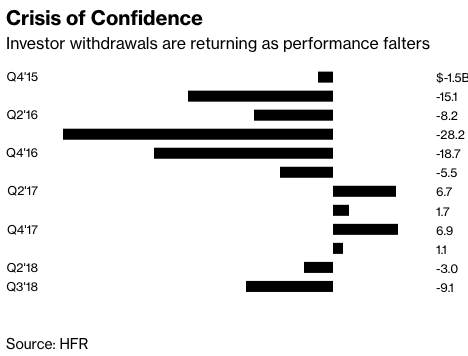

Although equity futures are pointing to a higher open on Wall Street in the early morning hours, and with both China’s indices finishing in positive territory overnight, Finom Group urges investors remain cautious as the current trading week may find investors selling the rips. Why? One very key event that is going to express itself this coming week for the markets and investors is hedge fund redemptions. Nov. 15th is the deadline for investors to put managers on notice to get some, or all, of their money at year end. If history is any guide, the rush for the exits will be rapid. Clients have already pulled $11.1 billion even before funds fell into the red for the year.

It’s “anything can happen Tuesday”, which is of course not a “thing”. Nonetheless one thing that will be happening on Tuesday is a morning chat session between Finom Group’s chief market strategist Seth Golden and the famous Dale Pinkert of Forex Analytix https://www.forexanalytix.com

Mr. Pinkert only interviews the top traders in the marketplace and offers a wealth of information to the public trading community through various forms of live streaming and social media platforms. Do check out our conversation!

To reiterate, caution is likely the best stance to take against the backdrop of a rather bearish marketplace presently. From a technical standpoint, the bear case holds water. From a fundamental standpoint, the debate is likely to wager on from both sides of the market. The bears can point to deteriorating A/D line performance over the last 30-60 days and all the aforementioned issues that brought about the October correction. The bulls can point to record high operating margins, strong revenue and corporate earnings growth, a relatively fairly valued S&P 500 and the probability of some of the bearish issues actually having a more positive outcome i.e. global trade and the FOMC potential to pause. Having said that, when in doubt, hedges and a long-term market outlook have a tendency to benefit investors more so than day-to-day minutia. Sometimes, you simply have to ride out the storm to find the sun will shine again.

Tags: AAPL FB GOOGL HD M NDX SPX VIX SPY DJIA IWM QQQ UVXY WMT XRT

{kind=link}