Welcome to another trading week. In appreciation for all of our Basic Membership level participants and daily readers of finomgroup.com content, we offer the following excerpts from within our weekly Research Report. Our weekly Research Report is extremely detailed and has proven to help guide investors and traders during all types of market conditions with thoughtful insights and analysis, graphs, studies, and historical data. We encourage our readers to upgrade to our Contributor Membership level ($14.99/monthly, cancel anytime) to receive our weekly Research Report and State of the Market videos. Have a great trading week and take a look at some of the materials from within this week’s Research Report, as follows:

Research Report Excerpt #1

J.P. Morgan “…we are now raising our forecast for 1Q real GDP growth from 2.5% to 3.25% saar. …We are also nudging our forecast for 2Q real GDP growth up from 0.75% to 1.0% saar…”

Research Report Excerpt #2

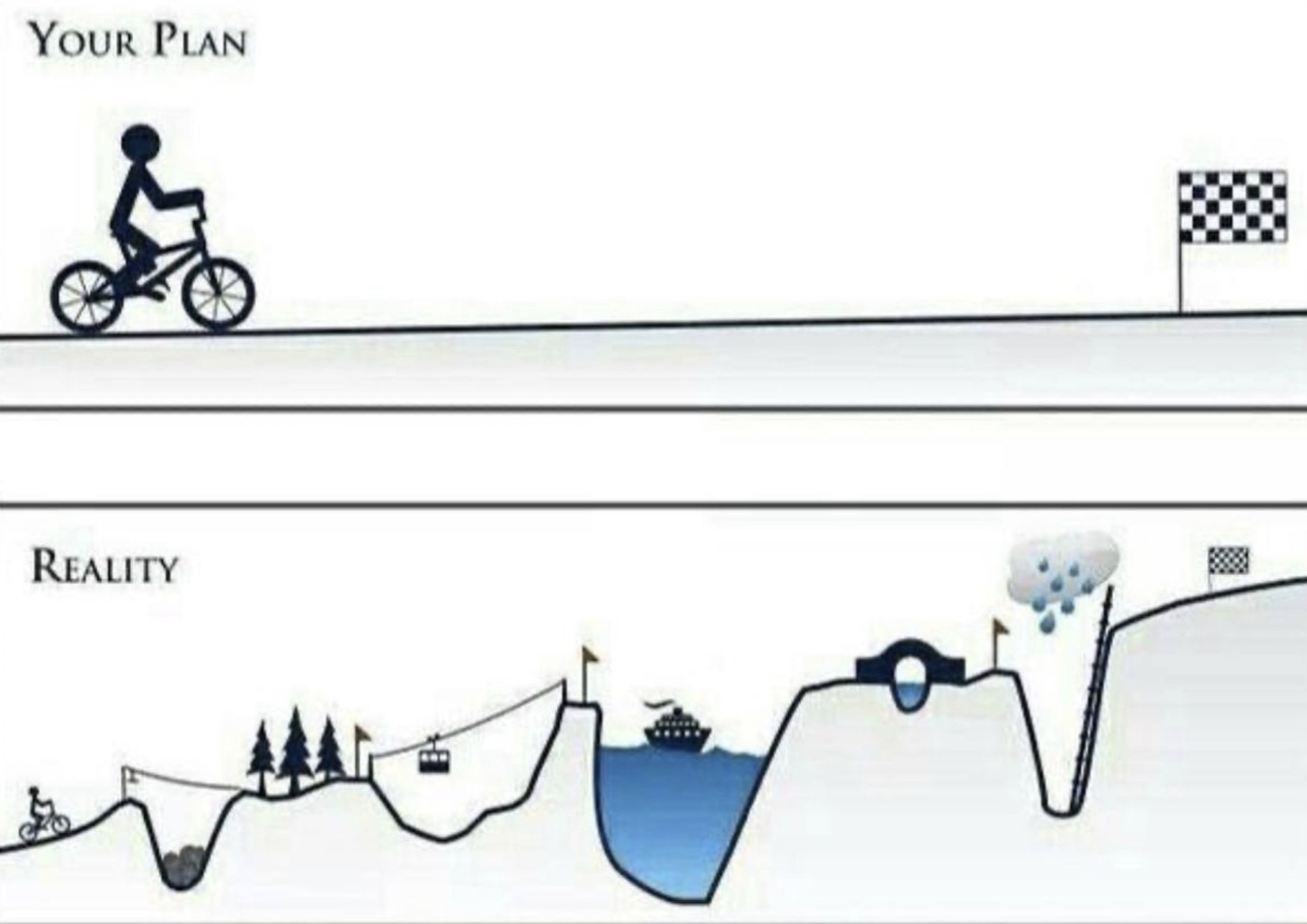

We’ve understood, as long-term, disciplined investors, that the recovery process wasn’t going to happen immediately or happen in a straight line. Our plan has a starting point and an end point, but rarely is that end destination going to translate across a smooth plane/pathway. The graphic above distinguishes how investors should better establish expectations from Point A to Point Z. Investors would like for the “Your Plan” path to play out, but the “Reality” pathway is usually how we experience markets. The destination is the same; the journey is often different than we plan.

Research Report Excerpt #3

Research Report Excerpt #4

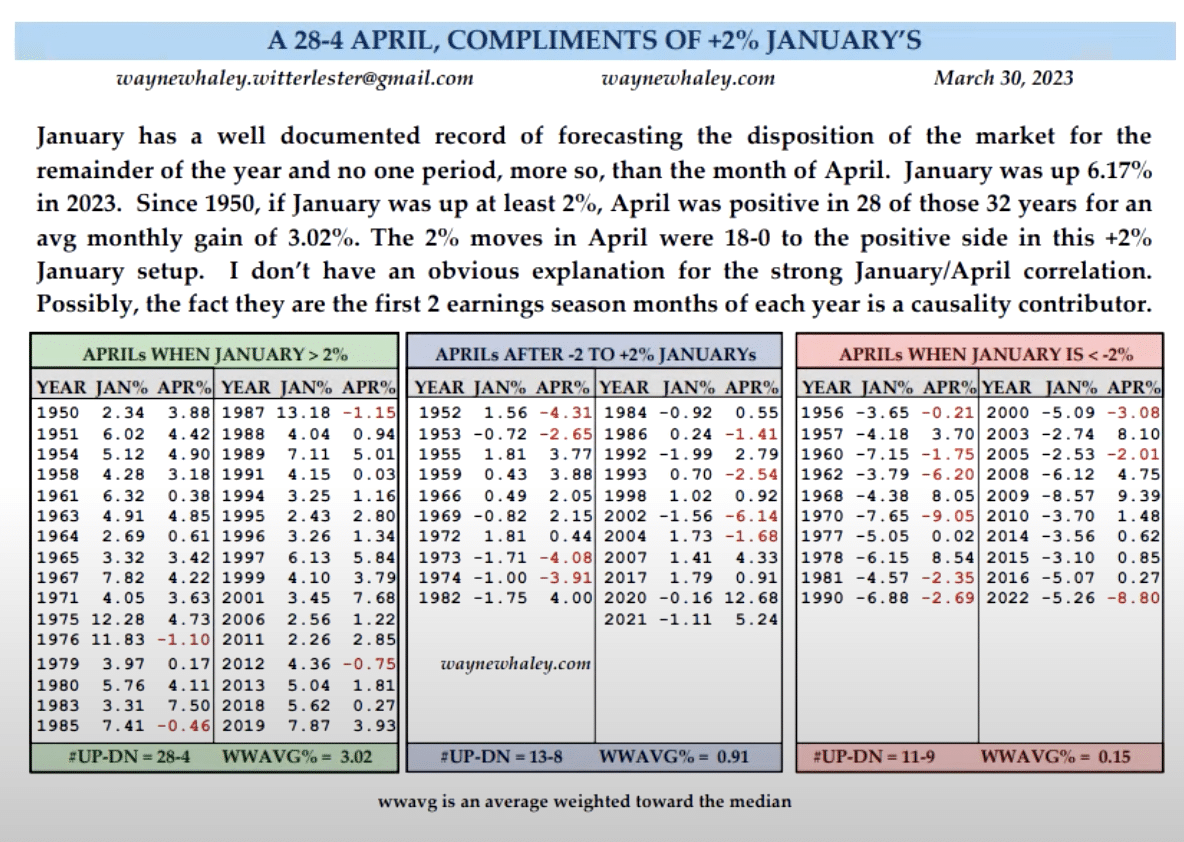

We can further elaborate on this point with the latest study from the most famous of quantitative analysts, Wayne Whaley. In his latest dissemination, he also reviewed the January returns against the forward April trading month. Turns out, his study doesn’t differ much, if at all from that of the January Trifecta and Fundstrat data positioned above. Here is what Mr. Whaley outlined this past week, in the table and commentary.

Research Report Excerpt #5

We initially alerted Finom Group members to this fundamental shift in the liquidity regime, which should prove bullish for markets, back in November of 2022, with the below commentary from Jim Paulsen, formerly of The Leuthold Group (retired).

Far too many investors are fighting last year’s bear market, failing to absorb the liquidity pivot that may be afoot  , and playing out in the price action of the markets. Liquidity rules all, and so long as liquidity is improving, the economic ramification from the primary bank failures and fears surrounding a future credit crunch are likely to be backstopped, or muted at the very least.

, and playing out in the price action of the markets. Liquidity rules all, and so long as liquidity is improving, the economic ramification from the primary bank failures and fears surrounding a future credit crunch are likely to be backstopped, or muted at the very least.

Research Report Excerpt #6

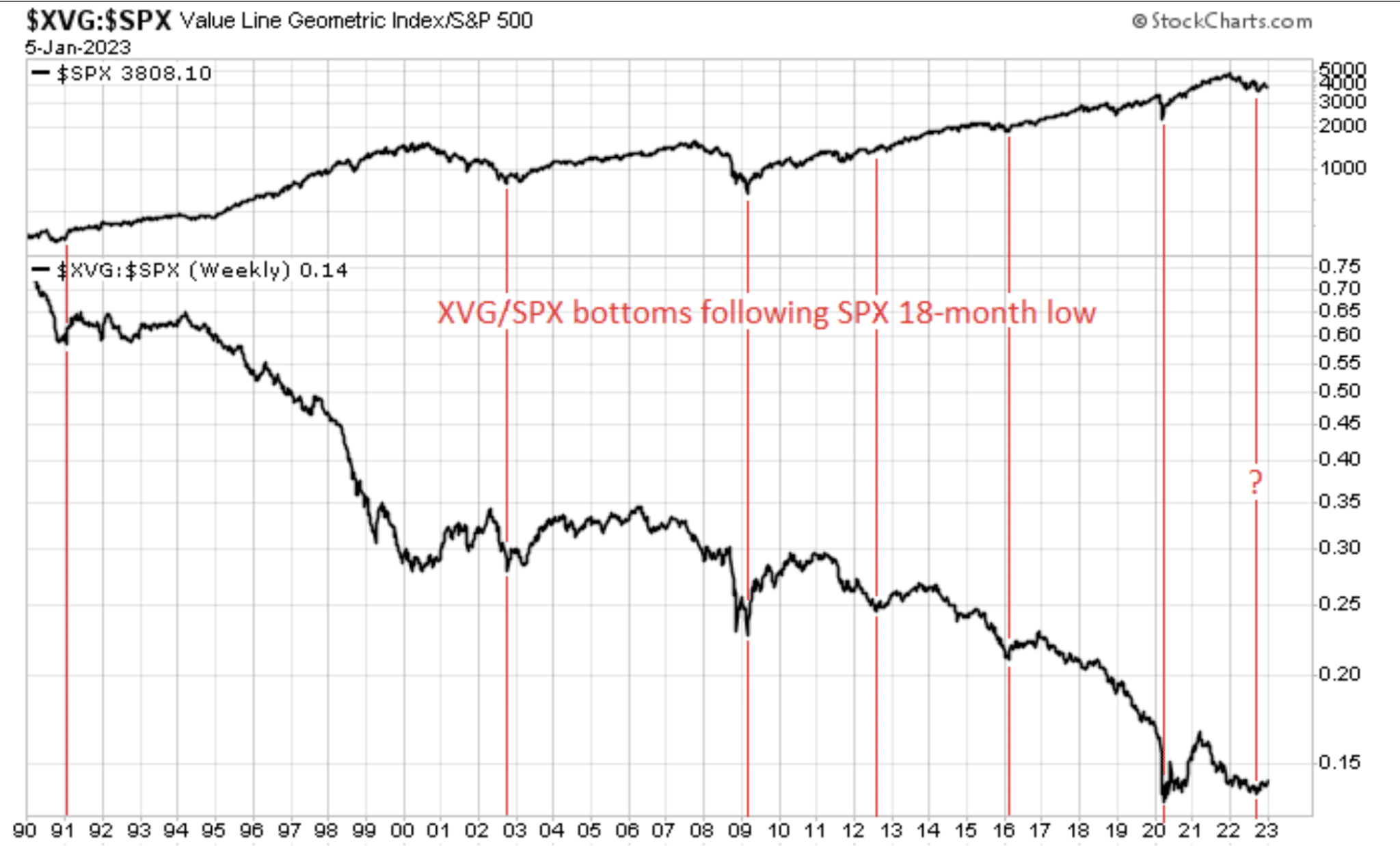

In reviewing the history of the Value Line Geometric Index (XVG), it often tends to show that the median stock leads off of market bottoms, but then fades relative to the S&P 500 and as a bull market persists. (chart via Mark Ungewitter)

This is a technical rendering that simply suggests the narrow leadership today is typical and investors are past the point where stock picking is likely to outperform the index. If the XVG is essentially the median stock index, and it underperforms throughout bull markets, it’s likely better to own the S&P 500 rather than the median stock. Don’t get me wrong, certain stocks will and can outperform, but our ability as investors to pick which ones will outperform often proves limited.

Research Report Excerpt #7

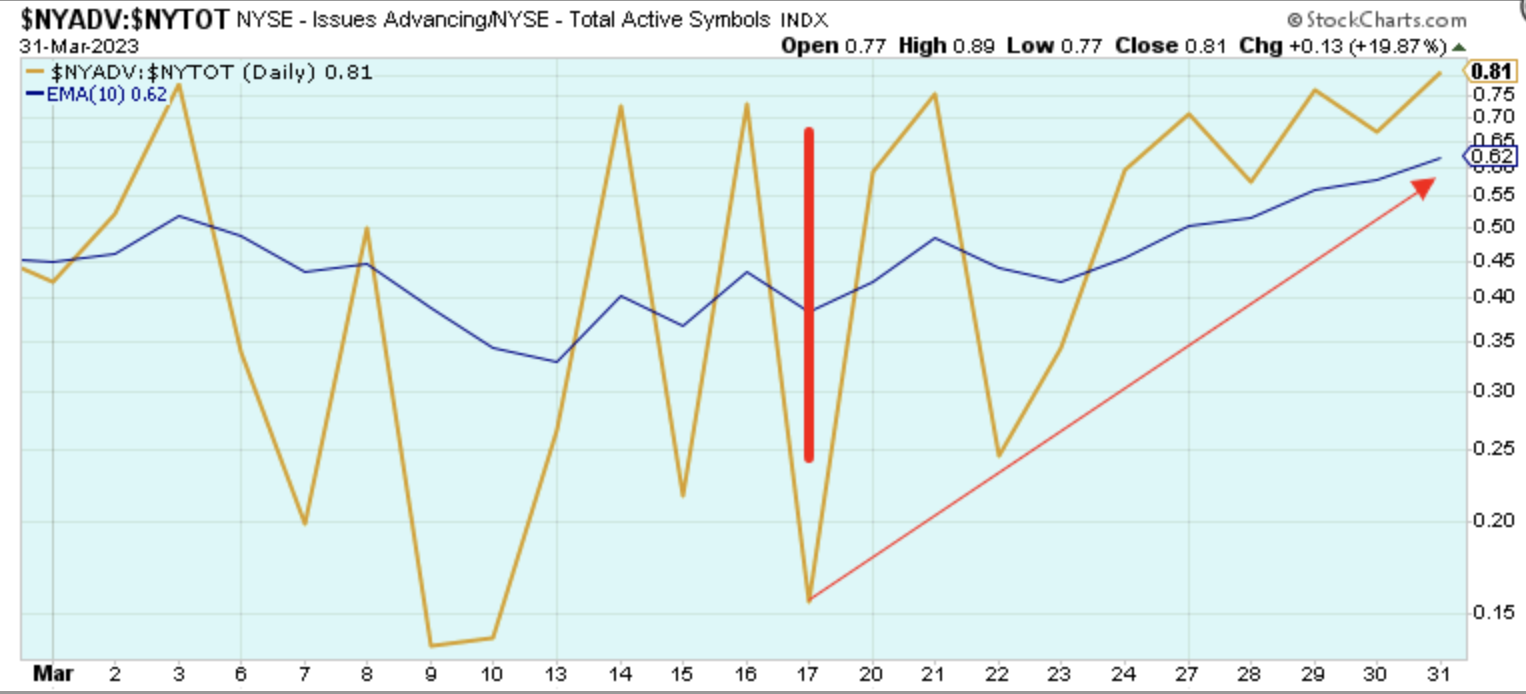

Below is a chart of the actual Zweig Breadth Thrust that completed, within the requisite 10-day period, on Friday of this past week.

There was an initial meltdown in market breadth during the first 2 weeks of March, which culminated in a significant breadth surge to end the quarter. For those investors/traders who don’t recall the last time ZBT signaled in 2019; the S&P 500 rallied another 27% to end the year with a 31% total annual return (including dividend).

Research Report Excerpt #8

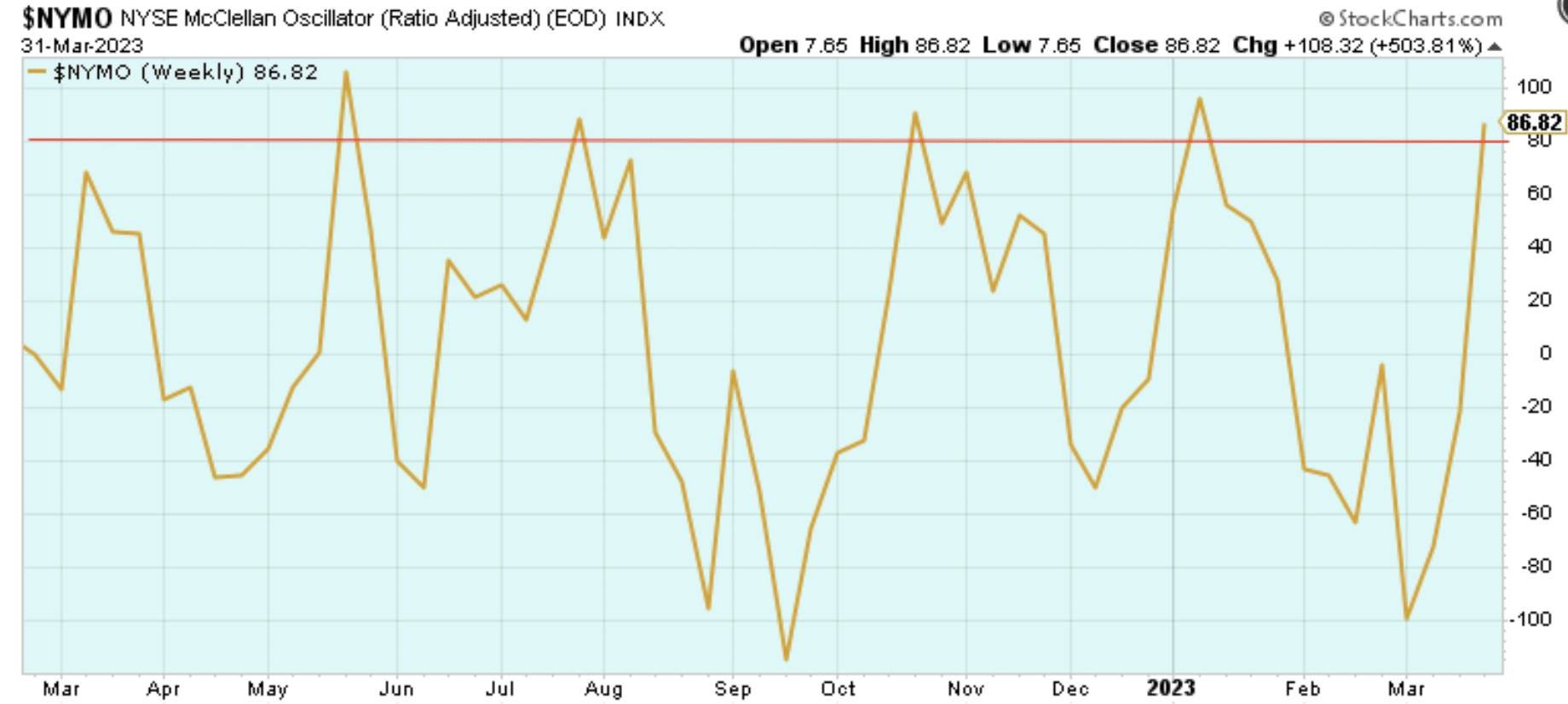

The S&P 500’s McClellan Oscillator (top chart) is at what can only be described as extremely overbought territory. We should not be terribly surprised if some form of consolidation is displayed in price action in the coming week/weeks, possibly just ahead of earnings season. For broad market consideration, the NYSE’s McClellan Oscillator (NYMO bottom chart) is also signaling extremely overbought conditions.

Research Report Excerpt #9

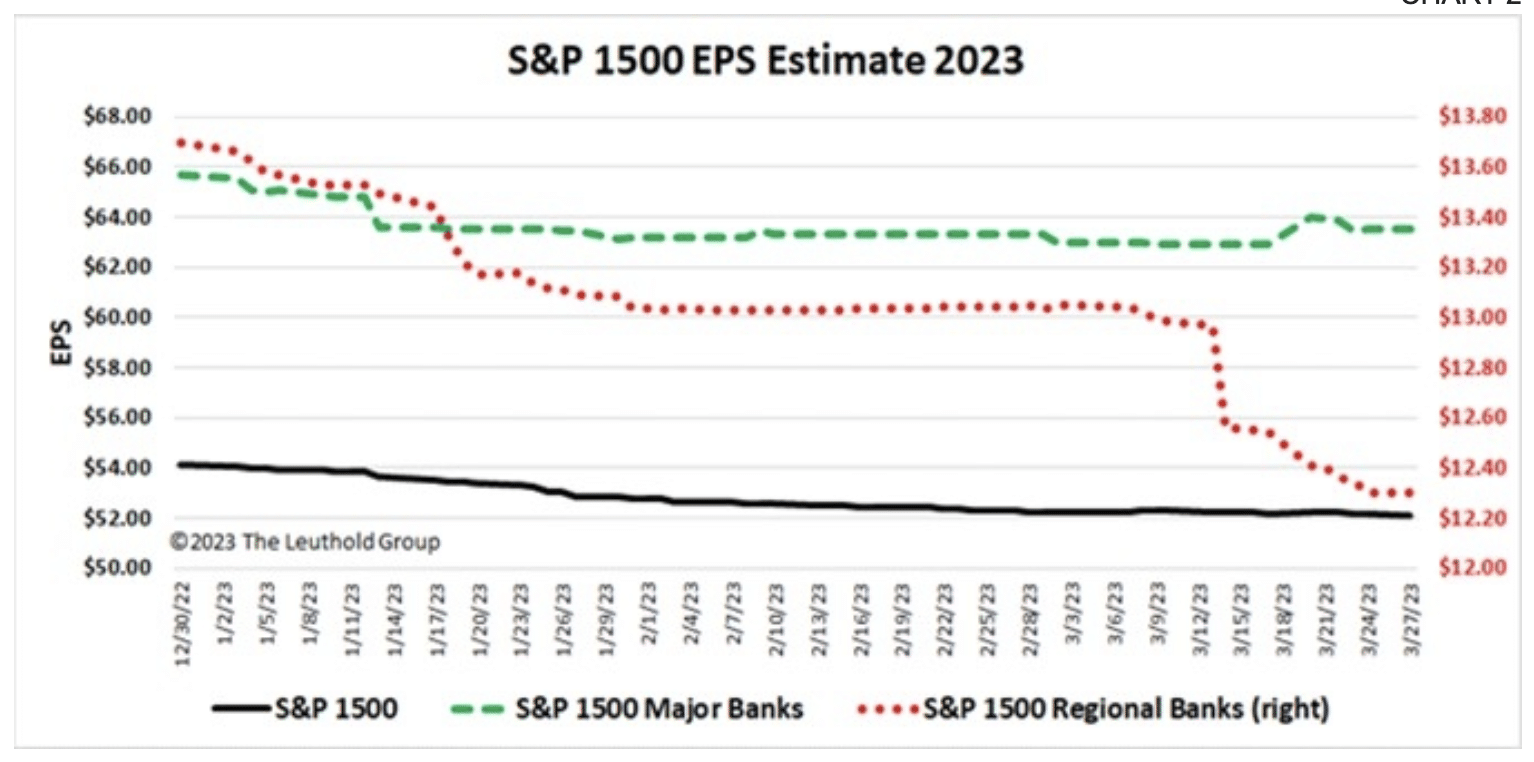

The chart below detail Wall Street’s estimates of EPS for 2023 and 2024. The broad S&P 1500 and major bank indexes have seen estimates hold almost flat since March 8th. Regional banks have seen theirs fall by about 6% as of March 28th; noticeable to be sure, but far from a crushing downgrade.

With estimates holding their ground and prices down 25% for the regional banks, unless regional banks paint an even gloomier picture than many are anticipating, we wouldn’t be surprised to see regional bank performance improve during earnings season, which kicks-off on April 14, 2023.

{kind=link}