Tempted to buy this dip? Presently the risk/reward scenario does not suggest doing so. Over the past 48 hours, there has been a significant sentiment shift in the marketplace and amongst investors given the threat of elevating tariffs on Chinese imports. Equity investors are becoming increasingly uncomfortable leading up to the proposed tariff increase. U.S. Trade Representative Robert Lighthizer cited “an erosion in commitments by China” in recent negotiations and declared tariffs on Chinese imports would rise to 25% from 10% on Friday, reiterating comments that President Donald Trump made on Sunday. However, China’s top trade negotiator Liu He is scheduled to participate in talks later this week, which is seen as a cause for some positivity. But some positivity remains to be seen as investors are attempting to bake into the market the worst potential outcome from these talks.

“This turn of events injects substantial uncertainty into the outcome, forcing investors to now factor in the possibility that a near-term trade deal may not be reached and that tariffs may be increased. Given these developments, we expect significant volatility, wrote Kristina Hooper, chief market strategist at Invesco in a Monday financial blog.

The most likely outcome from the pending talks between the U.S. and China is that tariffs are raised on Friday. This spillover affect to global equity markets looms large and is front of mind with investors. There is a very small window of opportunity with regards to the trade talks for a more conciliatory stance to take place and for tariffs to remain at current levels as offered by Meridith Sumpter of the EurAsia Group, in the following interview with Bloomberg TV.

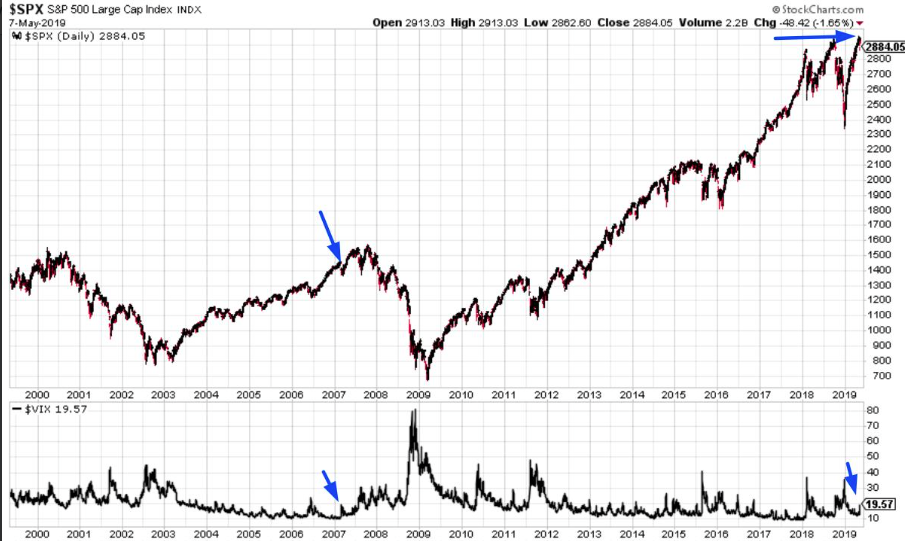

U.S. equity markets tumbled on Tuesday, but are presently bid modestly lower in the premarket and as renewed trade fears resound on Wall Street. Additionally, with the elevated fear on Wall Street, one can surmise the fear gauge or VIX has risen significantly in the first two trading days of the week. The VIX spiked more than 50% over the past 2 days, while still closing below 20 on Tuesday. From 1990 – present, this has only happened 1 other time; February 2007.

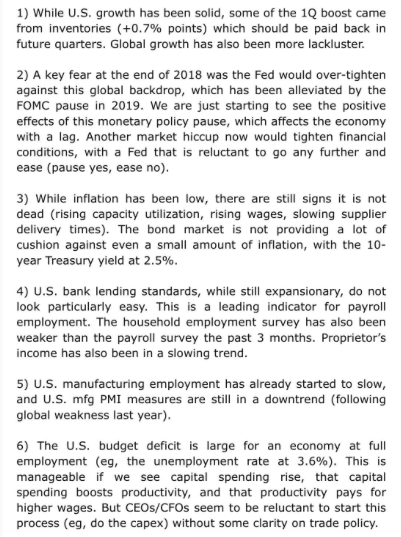

The fear on Wall Street is palpable and not abating with investors awaiting some clarity on trade talks that will commence once again in Washington Thursday. If you were looking for reasons as to why the present escalation of the trade feud is not a good time to raise the temperature, look no further than recent notes from Strategas identified below:

Moreover, Marc Chandler, a managing partner at Bannockburn Global Forex, suggested that “The threats to increase tariffs on China is part of the presidential game of chicken game with the Federal Reserve and Chair Jerome Powell and not with China. Trump could be using the ongoing trade feud as a means of backing the Fed into a corner.”

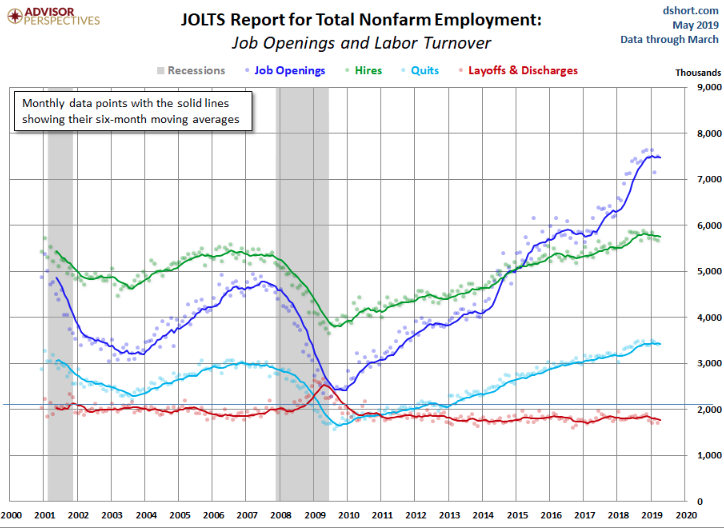

While investors remain skittish about the outcome of trade talks, economic data is showing further strength in the labor market as reported through the JOLTS Survey. The number of job openings rose to 7.5 million on the last business day of March, the U.S. Bureau of Labor Statistics reported today. Over the month, hires and separations were little changed at 5.7 million and 5.4 million, respectively. Within separations, the quits rate was unchanged at 2.3% and the layoffs and discharges rate was little changed at 1.1 percent. This release includes estimates of the number and rate of job openings, hires, and separations for the nonfarm sector by industry and by four geographic regions.

Overseas, Germany’s latest economic data release also showed some green shoots. German industry beat production forecasts in March, as output in the sector rose for the second consecutive month, led by manufacturing and construction. The Federal Statistical Office said Wednesday said total industrial output–comprised of output in manufacturing, energy and construction–increased 0.5% in March from the month before, in calendar-adjusted terms. Economists polled by The Wall Street Journal last week had forecast a 0.5% decline.

We wouldn’t be of the opinion that positive economic data will support equity markets in the face of trade fears that have a pretty binary outcome on markets. If the greatest fears are realized, we would expect the market sell-off to intensify. If tariffs are not raised and some degree of levity among the negotiations is found amicably moving forward, the markets will likely rebound. Having said that, growth in the U.S. is solid, and growth around the globe has shown signs of improvement. The Fed is also more dovish, as is the ECB. We can refer to these factors as the backstop for equity markets. Naturally, the backstop is only as good as the next buyer of consequence.

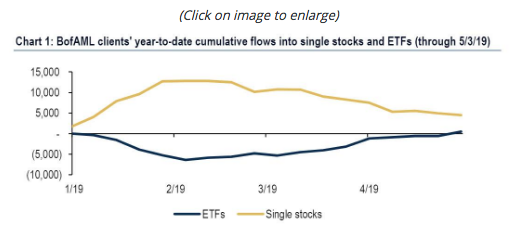

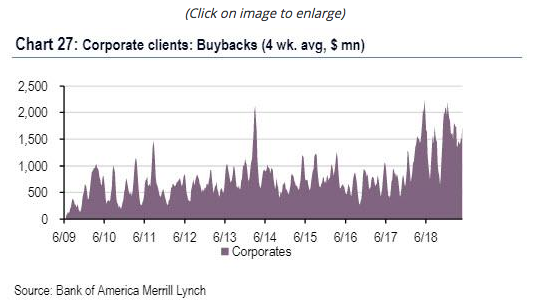

In speaking of the next buyer of consequence for equities, that has been corporate buybacks throughout the 2019 rally. Bank of America’s strategist Jill Carey Hall outlines that last week, during which the S&P 500 was up +0.2%, just about everyone was selling stocks, as “Institutional clients, hedge funds and private clients sold the highs in equities last week.” And yet, somehow the S&P hit a new all-time high. How? The answer: “Corporate buybacks ramped up.”

As BofAML discusses further, “buying was led by corporate buybacks, as all other groups (hedge funds, institutional and retail clients) were net sellers of equities for the 2nd week in a row as trade skirmishes flare up.

- Clients were net sellers of single stocks (2nd straight week) but continued to buy ETFs (8th straight week). Cumulative flows into ETFs YTD turned positive, reversing outflows seen earlier this year (Chart 1).

- Buybacks last week were their highest since early Feb: they tend to be strong during earnings seasons and seasonally peak in mid/late May. Buybacks YTD are +20% YoY, though the growth rate continues to decline.

It’s a little comical to witness this verified data from BofAML PB desk, given the former fears surrounding the blackout period that never came to be and have no basis in reality. This also means that we can once and for all forget about the recurring lie of a buyback blackout period that simply doesn’t exist with any enforceable measures by and through the SEC guidelines, which as I’ve explained in the past only applies to a subset of stock repurchases. (See March Research Report)

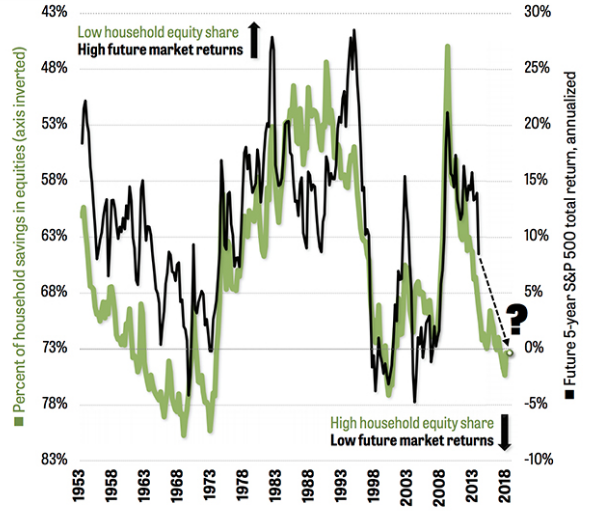

Investors shouldn’t anticipate a near-term bottom in equities should tariffs rise by Friday, but longer-term considerations for investors will eventually find a market foothold. With that in mind, the 5-year return probabilities for the S&P 500 come into focus as put for the by Michael Mauboussin, the director of research for BlueMountain Capital Management in New York City. Based on a formula that’s proven itself over the past 65 years, a new white paper by Mauboussin predicts that the S&P 500’s total return (including dividends) between now and the end of 2023 will be zero, as shown in the accompanying graph.

Mauboussin plots the five-year total return of the market against a statistic published by the Federal Reserve known as “Households’ Financial Assets and Liabilities.” (In its definition of “households,” the Fed includes some nonprofit organizations that serve families.)

The graph shows that the percentage of household liquid assets in stocks, ETFs, and REITs—as opposed to cash and bonds—has a close relationship to the returns of the stock market in the next five years. The fit isn’t perfect—if you find a formula that perfectly predicts the market, keep it to yourself, OK?—but the ups and downs of American households’ investments in stocks clearly show turning points in the S&P 500’s bull and bear phases.

In the graph, which is based on the raw data underlying Mauboussin’s white paper, higher percentages of household investments in stocks are shown as lower readings of the green line. The higher the percentage of stocks in people’s accounts, the lower the return of the S&P 500 in the next five years.

When households have more than about 70% of their liquid assets in stocks, the market’s return eventually becomes negative. With the percentage now around 73%, the expected five-year return for the market is zero, according to Mauboussin.

After recording all-time highs in the benchmark S&P 500, the market is reeling and the likelihood of further declines is increasing as algorithmic trading programs are now keying on the 50-DMA, which has a probability of giving way on Wednesday. Tariffs are a clear and present danger for corporate earnings, which are the underpinning of the long-term trajectory of the market. When those earnings are called into question, the market begins to price in the worst-case scenario, aiming to fill the gaps created in the upside market moves over the past several months.

With the threat of tariffs, analysts say many of Wall Street’s assumption for profits and growth would have to be tossed, suggesting that stocks could be too richly priced near recent highs.

“The forward price-to-earnings ratio on the S&P 500 was at 17 times earnings expectations. “That has to come down because growth has to come down…A good part of what went on in this market was predicated on a deal getting done in the first place. If that’s not the case, we have to start taking [earnings] estimates down,” said Art Hogan, National Securities chief market strategist.

Keith Parker, chief U.S. equities strategist at UBS, said the hit to S&P 500 earnings would be 2% or greater, if the 10% tariffs on $200 billion in Chinese goods are raised to 25%. Parker said earnings would be hit by 7% if there was a full-blown trade war, while the S&P 500 could trade in a range of 600 points on different scenarios of escalation of trade wars to de-escalation. The S&P is now near the top of the range, he said.

The market is in risk-off mode an fear is on the rise. It’s no time to play hero amongst the investor community and attempt to be the contrarian, as a flight to safety resumes anew and bond yields fall. U.S. yields are approaching their lows from the December 2018 period and when fears had reached a peak.

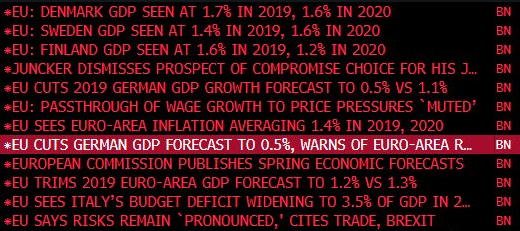

Another ramification from the latest spurring of trade escalation and fears is the lowered global growth expectations coming from the EU. Europe’s economy is slow to recover from a recent slowdown, weighed down further by the ongoing U.S.-China trade fight and a potentially chaotic Brexit, the European Union said Tuesday, further slashing growth expectations and warning of prominent risks.

Gross domestic product in the 19-member Eurozone will grow by 1.2% in 2019, the EU said in its quarterly report, cutting its 1.3% forecast from February. The expansion rate is seen barely rising to 1.5% next year, down from 1.6% previously expected.

“Substantial downside risks to the growth outlook remain,” the European Commission, the EU’s executive, said. “An escalation of trade tensions could prove to be a major shock and create roadblocks for Europe’s growth trajectory.”

“We should stand ready to provide more support to the economy if needed,” said Pierre Moscovici, the EU commissioner for economic and financial affairs, taxation and customs. “Above all, we must avoid a lapse into protectionism, which would only exacerbate the existing social and economic tensions.”

U.S. tariff threats are stoking business uncertainty and will prolong a longer-than-expected economic slowdown, European Central Bank President Mario Draghi said in April. The Eurozone lender could act to shore up the faltering economy, he added.

In setting up the trading day, the headlines will prevail and they will definitively center on how the market ebbs and flows through the news cycle, which will highlight concerns over trade and Iran’s latest uprising. There is no economic data scheduled for the day, while one Fed speech is also anticipated to a lesser degree. Should dip buyers present themselves to the marketplace today, we wouldn’t view this as foreshadowing a positive near-term outcome from trade talks, but rather a temporary reprieve of selling pressure and possibly a means or opportunity for de-risking.

{kind=link}