Tonight (Tuesday Sept. 29) is the first Presidential Debate on Fox News. Ahead of the first official debate, the equity markets are rebounding off of their recent correction-period lows and with the Nasdaq (COMPQ) recapturing its 50-DMA on Monday. The S&P 500 (SPX) captured the same moving average intraday, but came shy of closing above this faster of the major moving averages. The VIX was broadly up on Monday, but fell on the day and through the settlement after hours.

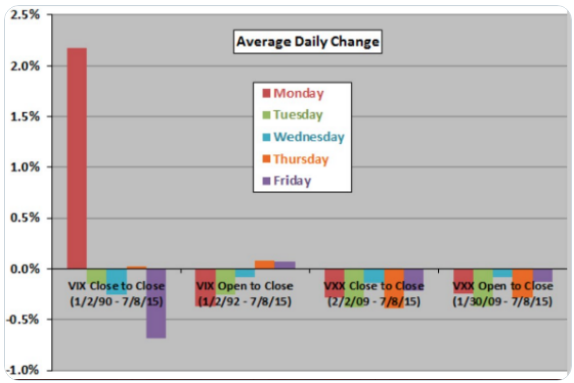

While many watched the S&P 500 rally 1.6% on Monday and with the VIX mostly higher for the day, this was actually typical for the VIX on Mondays. The more typical, inverse relationship between the two indices is often found with fault on Mondays.

- Calendar: Don’t let SPX:VIX fool you on Mondays folks.

- “VIX calendar” & how hedging creates its own indexed market, highlighted by activity on Monday & Friday historically, in the chart above.

- Monday the VIX resets from Friday’s lowered options bid & auto-weekly hedges roll on, which prove to elevate the VIX in the morning hours at least.

- Friday weekly hedges roll off, which tends to find the VIX lower on Friday and irregardless of the S&P 500 move.

In today’s “narrative” we’ll mainly focus on the implications of the upcoming debate and election season, as most are aware and found hyper vigilant given the circumstances. The mass financial media is in overdrive with their duplicative, superfluous and hyperbolic rhetoric/renderings as to what investors “need to know” and how they might position going into this seasonal period.

Many market participants have long since wagered their thoughts and bias for the election period. I’ll try offering my thoughts on the aforementioned time period from a practical perspective and spend some time on theorizing the potential near-term market responses for the pending Presidential Debates. We’ll tackle this exercise using a degree of game theory and critical thinking, but no guarantees are applicable of course.

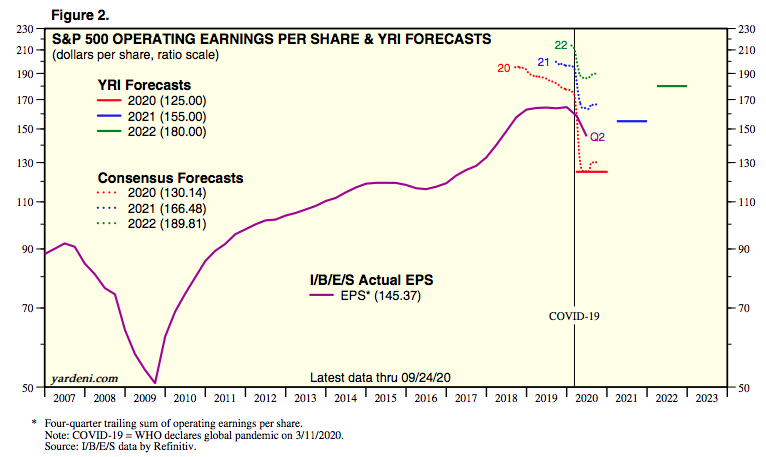

The first debate is less critical for most investors/traders, as investors will not likely change the course of their allocations and if history is any useful guide. Investors, especially passive investors know that an election outcome is going to take place and as such the market will eventually revert to its primary operation of discounting future earnings. Given this truism of markets, the whole of the election cycle may find investors better positioned by ignoring the noise and remaining focused on the long-term market drivers, earnings and/or liquidity. Additionally, those earnings projections for 2020 and 2021 have been on the rise, as shown in the chart below from Dr. Ed Yardeni:

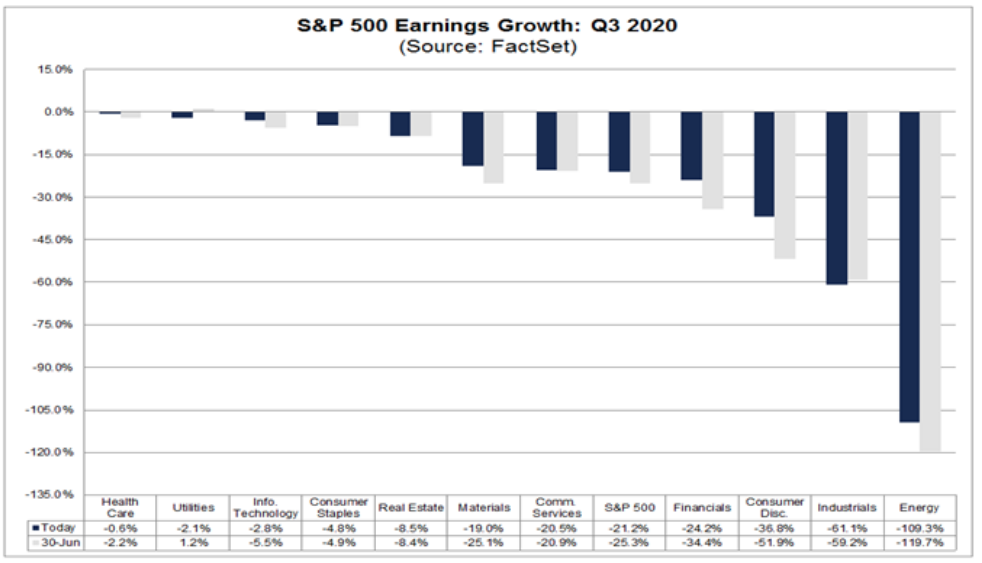

The S&P 500 EPS estimate for Q3 of $32.95 is above the estimate of $31.78 on June 30, 2020, further evidencing the consistent upward revisions over the last couple of months. The following chart of sector and S&P 500 total Q3 earnings forecasts was recently upwardly revised by FactSet:

By now, the candidates’ policies are known by market participants and therefore known by the market. The notion that the market is simply “biding” its time and hopeful for the most optimal outcome (market friendly) is utter nonsense. That’s simply not how the market works and we have already seen the markets’ attempt to price in election risk/s since early 2020. The market fully understands and reflects Joe Biden’s platform for potential tax hikes on certain segments of the population and/or business community in the same way the market understands President Donald Trump’s policies on trade and the overarching Make America Great Again platform he’s been campaigning since 2016. Both candidates, at face value, bring to the market a degree of unfriendly policies, but the latter candidate comes with known unknowns and the former brings unknown unknowns with respect to policy implementation. To put it more frankly, the market is more content with the “devil” it knows, rather than the devil it may be forced to acknowledge once again.

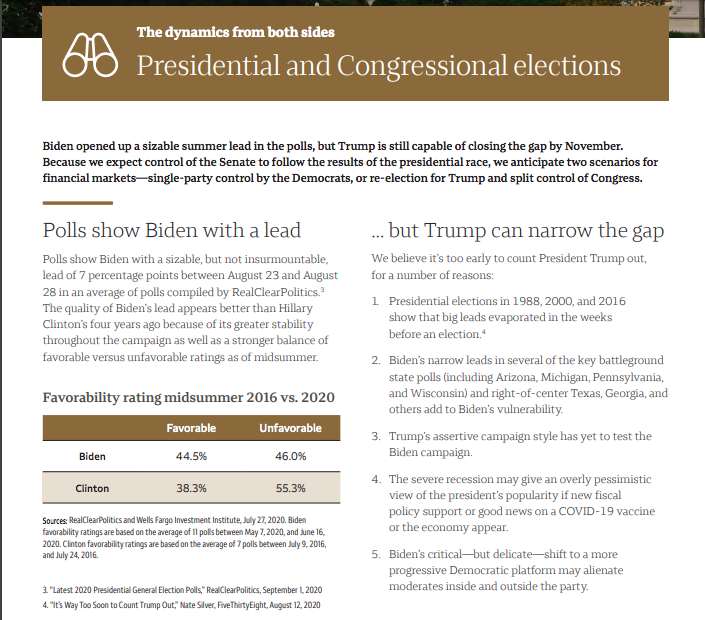

Here is where the candidates stand going into the first debate and with Joe Biden leading in most polls, however early it may be.

As it pertains to the upcoming debates; what does it takes to capture a debate-night victory? The challenger, as Biden will be known, is generally at a sentimental disadvantage. Americans, like the markets, can often lean in favor of the devil they know and rationalize the economic conditions that they’ve come to expect over the recent (4 years) presidential term. The edge in a normal election debate cycle would therefore favor the incumbent, President Donald Trump, and assuming an expansion cycle has been in place. But this is no normal year within an election debate cycle. This is the year of COVID-19! Therefore, we would have to exonerate the economic value that would usually accompany an expansion cycle with the lowest unemployment rate in 60 years that might have found a tailwind for the incumbent, largely due to the pandemic usurping the former expansion cycle. Furthermore, having some of the worst global COVID-19 statistics suggests the handling of the pandemic period reduces the economic talking points for which the incumbent can lean into during the debate.

While I could go on and on about what talking points and go-forward policies that favor this candidate over the other, I think that’s an exercise in futility and little more than noise at this point. This is not only the year of COVID-19, it’s a debate that includes President Donald Trump. If history teaches us anything it’s this: The establishment is often brought under scrutiny by leveling hyperbolic moments during a debate. Joe Biden has been deemed an establishment party candidate in the same way Hillary Clinton was in 2016, something Americans have long-since been found for souring sentiment. In the 2016 debates, simple hyperbolic statements found outsized favor for Donald Trump, mostly remembered by the infamous chant “Lock Her Up”! So while the talking points are the norm, they did not play well for the establishment in the last debate cycle of 2016 and I wouldn’t be of the opinion that is where favor would be found this go-round either. True, our sample size is just one here, but the variables are very similar.

The Trump campaign managers and strategists are likely well aware that the President would falter or be found less favorable amongst voters under time-tested debate norms. Staying on task, on point has not been a demonstrated quality of the President over the last 4 years, at least. This is not a personal jab at the President, but a truism that we’ve all seemingly adapted to up to and including scheduled press conferences that never start on time or within a half hour of the time they were scheduled. It is simply what it is, and again, the devil you know!

President Trump’s strategists and mangers would likely already have a couple of “bullets in the chamber” to fire off that will take little to come into play should POTUS find himself anxious during any portion of the debate. Strategists have likely also coalesced around a few hyperbolic, one-liners aimed at the challenger that would also incite “the base” and favor the Fox News audience. This is a key point folks, don’t miss this!

To the degree that stage presence and general candidate comfort is found, it is often found amongst “Friends & Family”. Fox News network has been more friendly to Trump than other media outlets over the last 4+ years. I think this also puts President Trump at an advantage, at least to start debate night/season. By the 3rd question, however, this will likely move from a tailwind to a non-factor as Biden catches greater comfort form his experience and U.S. political tenure. Biden’s comfort, however, is dependent upon how much hyperbole and denigrating commentary President Trump dishes, like it or not.

Midway through the first debate, President Trump should capture a sentimental lead. What he can’t afford to do is “play by the rules”, which basically panders to the establishment, Joe Biden. If this should happen, it creates a tailwind for Biden, not only in the Tuesday debate, but for the subsequent debate/s. I wouldn’t be of the opinion that again, President Trumps’ strategists, wouldn’t foresee and theorize a game plan to avoid such an outcome. Hence, no matter which direction we analyze the potential debate, at some point it must revert to hyperbole, one-liners and a break from norms in order for President Trump to be deemed the victor. Ending the first debate is often found a favorable circumstance for the incumbent, as they are more often than not offered “the final word”.

For Joe Biden, while his camp of managers and strategists know to expect the aforementioned hyperbolic retorts, responses, one-liners and even ad hominem attacks from President Trump, reacting rationally and with favor is an art form that we didn’t necessarily see play favorably for the challenger during the Democratic debates in 2019. Such a rational, favorable response is likely to be learned after the first debate by the Joe Biden camp, not during. As such and at the risk of repeating, any which way we analyze the potential debate, Joe Biden may need home field advantage and debate experience with an opponent such as Donald Trump before finding a victorious debate outcome.

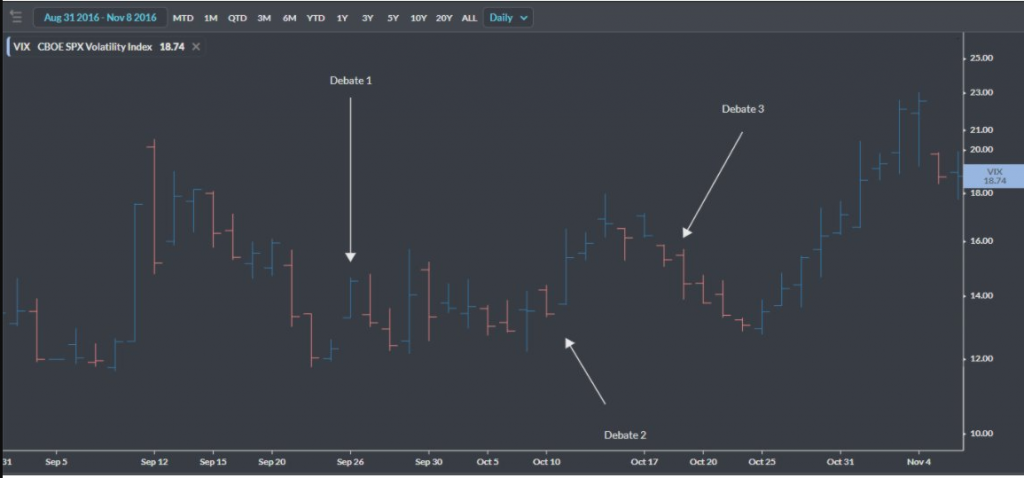

When it’s all said and done, an outright victor could be difficult to assess, even from polling. I wouldn’t anticipate too much, if any market reaction, directly related to the first debate night and if anything a market move may be more coincidental than anything else. This would be consistent with the first debate in 2016, as shown in the chart below:

- VIX didn’t move much after the 1st debate back in 2016.

- It rose a bit after the 2nd, but fell after the 3rd debate.

- Ultimately the VIX ran hot into the actual election and peaked above 22 election night.

This has already proven a highly volatile year for the S&P 500, culminating with the highest closing VIX reading (above 82) in history. Market realized and implied volatility has been trending lower since March, but remains elevated given the unique circumstances presented before investors over the aforementioned time period.

As disseminated by the CBOE, the average close/close change in the S&P 500 Index this year has been 1.57% (absolute value).

- The average closing value for the VIX in 2020 through September 18 is 30.7, which implies 1.92% daily moves in the S&P 500.

- The average closing value for the VIX Index in 2019 was 15.39.

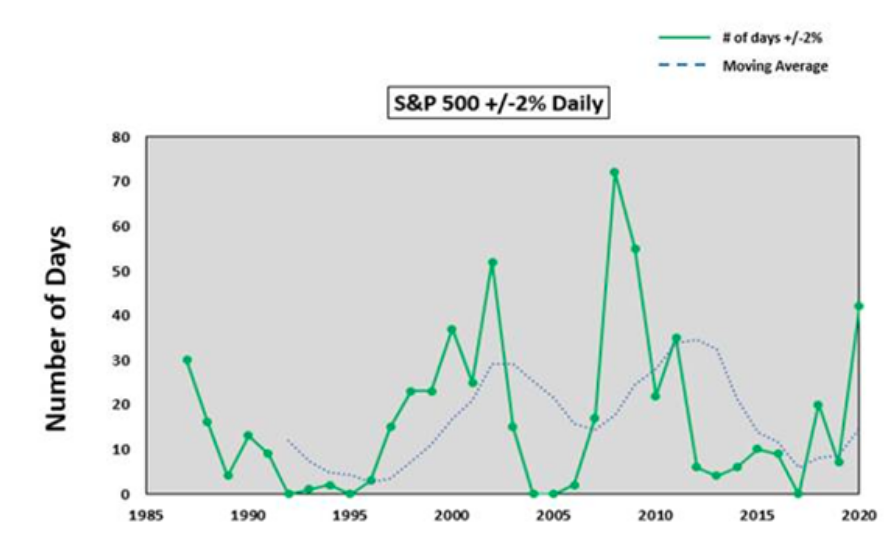

Thus far this year, 47% of the trading sessions have exhibited +/-1% “volatility” and 23% have been +/-2%. The market is on pace for ~55 sessions with 2% moves! That’s only been eclipsed in 2008, which experienced 72 such volatile sessions.

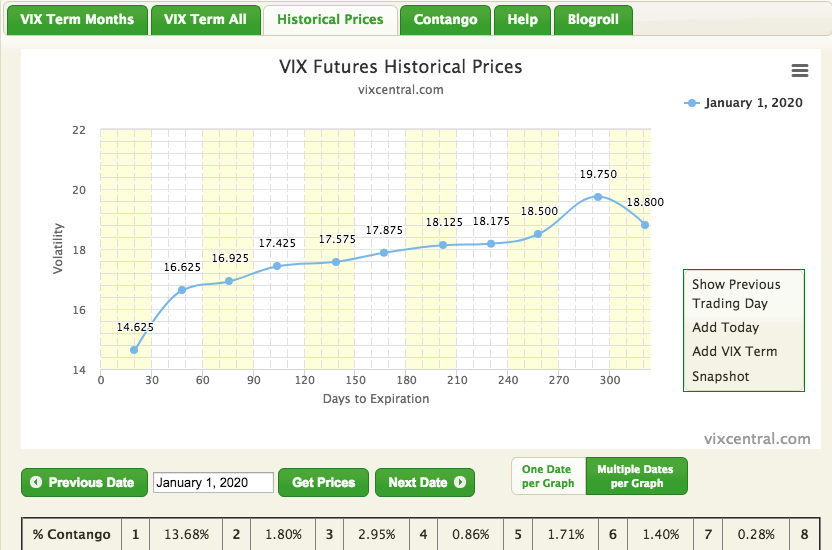

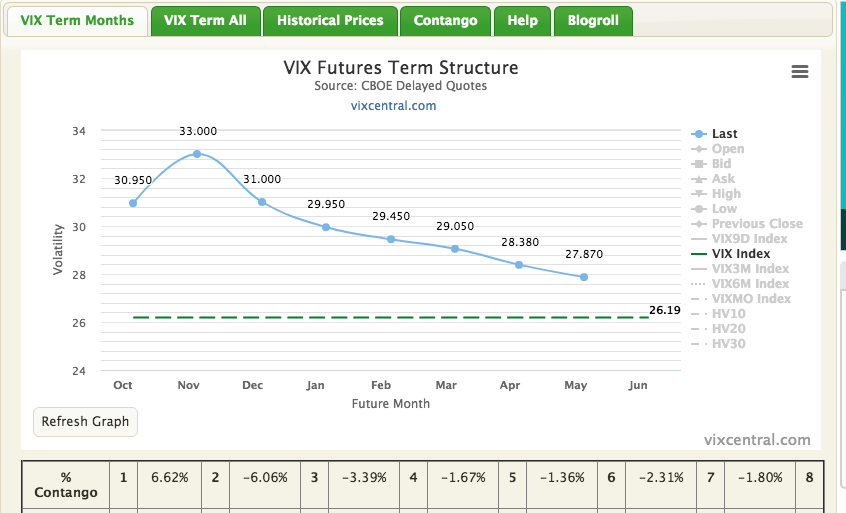

With a 10.2% peak-to-trough S&P 500 correction having already unfolded with earnings positively revised in continuum, ahead of the actual election and with debates ahead, the question that remains front and center is, “How does this election saga end?” This is what, unfortunately and possibly irrationally, has kept a goodly amount of investors up at night. This will likely keep many investors on edge until the election finds a terminal point, with a RESULT! Make no mistake about it, a result will be found and for which makes much of these consternations and anxieties rather silly if not useless and for the very sake of inviting volatility into one’s portfolio. We can see the anxiety over positioning for the election, which may or may not prove contested for an outcome, play out in the VIX Futures market since the beginning of the year. There has only been one contested election in the modern era, but recency fears have reared their ugly heads given the media attention and incumbents foreshadowing of a potential contested election.

That bump in the curve, identified on January 1, 2020, reflects the premium in the October VIX Future contract. The bump or premium has existed ever since. The contract price has risen steadily throughout 2020 and more recently in September tipped $40 before drawing lower to the current value of $30.95 (Monday evening).

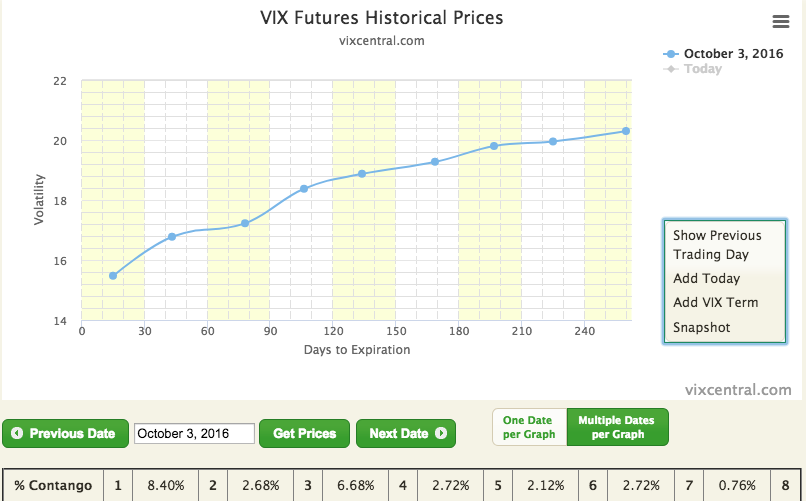

This is quite the premium being paid for protecting downside risk, even for an election cycle. We can’t dismiss that if 2020 was a normal economic calendar year, whereby a pandemic self-induced recession didn’t spike VIX and VIX futures, the current premium would likely mirror that of 2016. If we travel back in time we can see the price of VIX futures for the 2016 election below.

The front month VIX Future in October was less than $16 and found with 8% contango, suggesting the VIX was also below 16 at the time. Today’s October VIX Future contract is more than double what it was in 2016. There has been a goodly amount of election cycle, volatility front-running by investors all year long. While you and I can rationalize the activity and even look beyond this time period to understand an outcome will be found and markets aren’t guided by politics, we can’t impede the understood mass protection buying afoot. Having said that, we can look beyond the abnormality of the here and now in markets and position for the inevitable drawdown in market volatility, given the outsized premiums at play.

As it pertains to market volatility (VIX), what we recognized from history is that what goes up, must come down and normalize around the VIX mode with time. Despite popular characterizations, the VIX does not just mean revert, but rather mode revert. The VIX spends the majority of its time around the mode (12.43) and not the mean.

With the previous statements and “knowns” about the VIX recognized, I think investors are best positioned for the “end result” of the election rather than the intermediate. Having said that, investors should adhere to their disciplines and risk tolerance/management modeling.

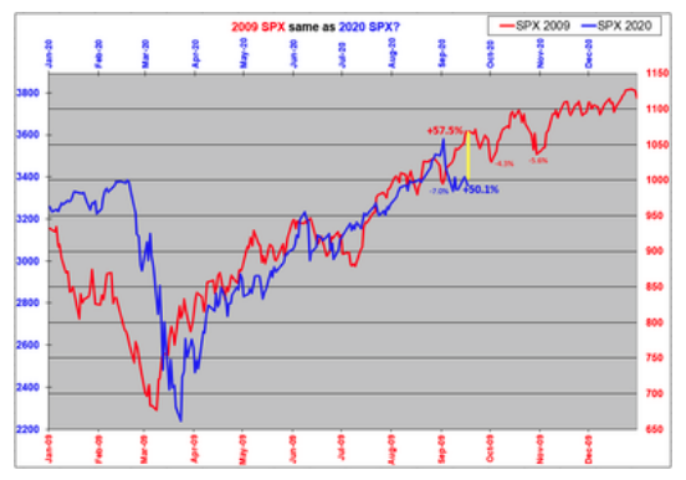

From another perspective, the VIX has been trying to follow the VIX 2009 analogue since the March, market bottom and has been extremely successful in doing so. The recent September VIX spike happened precisely when it did in 2009, to kick-off the month.

Moreover, while the S&P 500 has recently underperformed the same 2009 analogue by roughly 5% during the consolidation/correction period (See chart below), another VIX spike started the October market cycle in 2009. (See VIX 2009 chart above). The first of what appears to be triple-PEAKS, completing in early November and before the VIX found its first sub-20 reading in December.

- The S&P 500 has recently seen the largest performance gap (yellow line) from the 2009 analogue since mid-May, which has positioned the S&P 500 for a potentially sharper rally once the consolidation period has concluded.

- The only question is: what will the catalyst for a resumption of the uptrend be, if any? Earnings season, oversold conditions…?

Investor Takeaways

I’m of the opinion that the market will remain more focused on the macro-picture through the first debate, and conditions are more favorable for the incumbent to find greater favor due to some unique and Trump-centric debate characteristics, which should be favorable for markets. There are no guarantees of course, but our game theory exercise suggests that the media’s hyperbole may prove to be the more detrimental factor for investor positioning heading into debate and election season than any of the actual outcomes, contested or not. Keeping in mind that there has only been 1 contested election since the 20th century (2000), investors shouldn’t be moved to act based on a sample size of 1, that we also can’t directly correlate to a 2000 market response from said contested election (Gore vs. Bush).

What we have seen already from former September VIX futures positions/contracts is that through the contract cycle (roughly 30 days), a trader/investor had only a brief period to witness contract appreciation before the contract finished at its low trading price by expiration. Premiums proved too high, without demand, building contango and impeded by the time lapse value throughout the cycle. Heading into the month of October and still with more than 30 days until election day, similar elevated premiums exist in VIX futures, but with even more contango (6%+). Protecting one’s portfolio for a near-term event outcome often proves a tax on one’s portfolio, rather than an “assumed/implied hedge” against downsize risk. Elevated premiums force investors to pick and choose protection with that much more precision. Simply and rationally put, I think it that much more beneficial to position for the inevitable result and pending volatility decay thereafter than to postulate and position for the near-term unknowns. While it may be true that the market doesn’t appreciate uncertainty/unknowns, what price are you willing to pay for speculating!

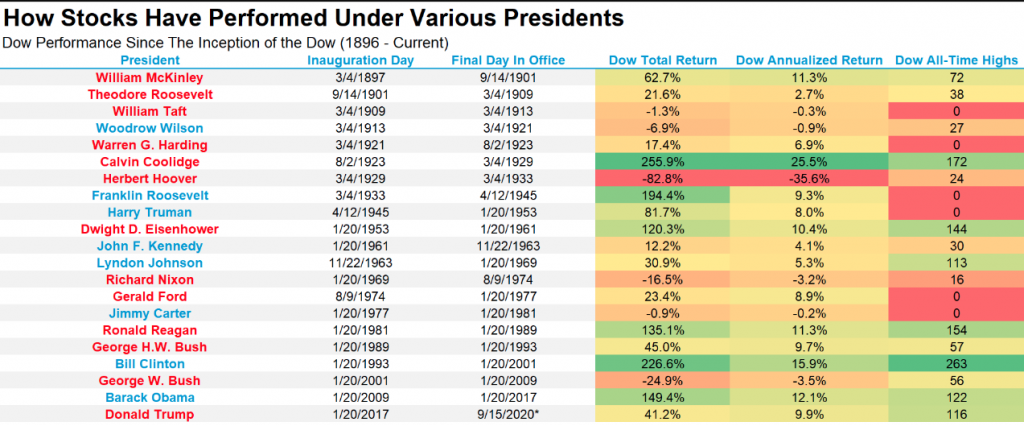

The whole point of this exercise surrounding the election season is not to suggest that the active portfolio manger shouldn’t hedge against market risks, but to simply weigh the cost of doing so. What we know and better understand through much of our due diligence is that political outcomes don’t determine long-term market trajectory: earnings and liquidity accomplish that task. Below is a table of market performance under each president going back to 1896. (LPL Financial)

Lastly, and for those intently focused on contested election risks, here was the market’s play-by-play during the contested election year, and with a BEWARE caveat thrown in for good measure 😉 ! (DataTrek)

Contested Election 2000:2020

- Election Week: The election was held on November 7th, 2000, but the outcome was unknown for over a month because of the time it took to recount Florida’s ballots and decide who won its Electoral College votes and therefore the presidency.

- From the close on Election Day through the end of the next week on 11/17, the S&P was down 4.5%.

- By the end of a little over 2 weeks since the vote, the S&P was down 6.3% from 11/7 to 11/24.

- From Election Day on 11/7 through November month-end, the S&P was down 8.2%.

- Week 5 and through year-end 2000: The Supreme Court decision Bush v. Gore was announced on December 12th. Despite investor relief about the conclusion of the US presidential election, the S&P fell 0.65% that day as a revenue and earnings warning from Compaq Computer further fueled concerns over tech profitability in a slowing economy. As a result, the S&P was still lower by 4.2% from Election Day (11/7) through the Supreme Court’s decision on 12/12.

- Volatility only got worse even with the certainty of the presidential outcome. Later that week, Microsoft announced it would miss estimates for the first time in a decade, leading to a large tech selloff.

- Post the Supreme Court’s ruling on 12/12, the S&P had 5 more down +1% days through year-end: 12/14 (-1.40%), 12/15 (-2.15), 12/19 (-1.30%), 12/20 (-3.13%), and 12/29 (-1.04%).

- From Election Day on 11/7 through year-end on 12/29, the S&P 500 declined by 7.8%.

As for what this means if this year’s presidential race is contested as a worst-case scenario: 1) Not knowing who will be President for days or even weeks after Election Day certainly does contribute to incremental volatility. 2) But investors understand an outcome will eventually be called and can start discounting the winner based on legal proceedings. 3) Long-lasting and significant volatility usually stems from an economic shock as opposed to politically related issues.

{kind=link}