U.S. equity markets were up, down and all around on Monday with only the Dow proving capable of holding any gains on the day. Commodities actually were the biggest gainers on Monday with Gold and Crude oil prices moving higher, carrying forward gains from the previous week. New sanctions from the U.S. were slapped on Iran in response to the downing of an unmanned U.S. drone last week.

“We will continue to increase pressure on Tehran until the regime abandons its dangerous activities,” including its nuclear ambitions, Trump told reporters in the Oval Office.

“We do not seek conflict with Iran or any other country,” Trump added. “I can only tell you we cannot ever let Iran have a nuclear weapon.”

With yet another geopolitical skirmish rising to the forefront over the last couple of weeks, investors remained focus on the most highly impactful G-20 Summit. Equity strategists, economists and analyst are all weighing with regards to the outcome from the Trump-Xi meeting in Japan. Morgan Stanley’s strategist offered the following on the subject matter Monday:

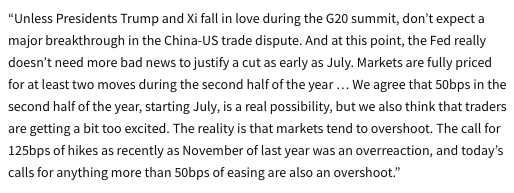

“… as we enter this week, there seems good reason to expect that the G20 will result in a tariff ‘pause’, affording both sides a defined period of time to get negotiations back on track before resorting to further tariff escalation. But investors beware: while a pause is better than escalation, it won’t refresh the economy enough to forestall a challenging path for risk assets: A pause, particularly one that comes without preconditions and follows a period of heated rhetoric, would be positive, signaling that both sides want to avoid further economic damage. If it coincides with Fed dovishness, a pause could boost investor sentiment and risk asset prices in the short term. However, we’d view this more as a set-up to sell risk than a catalyst to turn more bullish.”

Citi Group’s Tobias Levkovich suggest investors shouldn’t expect anything game-changing from the talks at the G-20 Summit.

Goldman Sachs is of the opinion that the White House isn’t done raising tariffs even if it doesn’t take place at the G-20 Summit. The firm believes that should the FOMC lower rates, this provides the Trump Administration more time to negotiate and ease the consumer pain from higher prices.

“We do not believe that the Trump Administration is done raising tariffs,” analysts wrote in a note to clients on Friday — and may even escalate further given the Federal Reserve’s accommodative stance.“

“The President’s stated desire for easier monetary policy might even motivate the White House to increase and/or prolong uncertainty. While we think some additional tariff escalation is more likely than not, we do not expect the White House to impose a 25% tariff on all remaining imports from China. A lower rate, like 10%, would be the natural alternative and would reduce the impact on consumers.”

On July 2, the next public comment period of tariffs concludes, Goldman pointed out. After that, the White House will likely initiate a final tariff notice on imports from China, but the implementation of tariffs would take another couple of weeks.

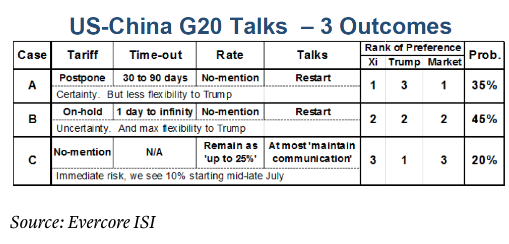

Evercore ISI strategist Donald Straszheim said there are three potential outcomes from the Trump-Xi meeting: First, the U.S. agrees to hold off on slapping additional tariffs on Chinese goods for an indefinite amount of time. Second, the U.S. holds off on additional levies for a fixed amount of time. Third, the U.S. makes no mention of the additional tariffs in its post-meeting statement, which would suggest the administration will move forward with them “ASAP.”

The ongoing trade feud between the world’s super economies has already taken its toll on the global economy and corporate profits. With FedEx (FDX) set to report its Q2 2019 results after the closing bell Tuesday, investors are forced to pay even closer attention to the firm’s outlook and findings from business operations outside of the United States. Earnings, revenue estimates and stock price targets have been slashed on concerns over a slowdown in the global economy, particularly in China and Europe.

One of the more investor friendly firms in the Dow has recently given investors even greater cause for concern that has little to do with the global issues. FedEx’s declaration on June 10 of a quarterly dividend that was unchanged from a year ago effectively snapped a 10-year streak of rising dividends.

“The non-raise “could prove a telling sign,” given mounting macro uncertainty, sluggish volume trends and FedEx’s need to refresh its aircraft fleet and make ongoing e-commerce investments, said Analyst Patrick Brown at Raymond James.”

The average analyst EPS estimate for the quarter ended May, as compiled by FactSet, is $4.85, which is down from $5.91 in the same period a year ago. The FactSet consensus has declined steadily this year, from $4.93 at the end of March and $5.32 at the end of December. For fiscal 2020, the FactSet EPS consensus is $16.23. That’s down from $16.82 at the end of March and $17.99 at the end of 2018. The FactSet revenue consensus is $17.80 billion, up from $17.30 billion a year ago. That includes a $9.46 billion consensus for FedEx Express, a $5.20 billion consensus for FedEx Ground and a $2.01 billion estimate for FedEx Freight.

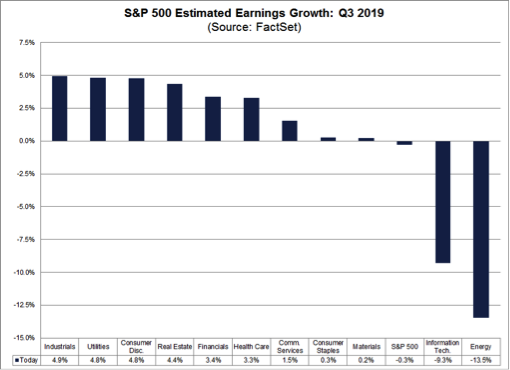

As profit reports just start to trickle in, the expectations are getting worse. Forecasters already were indicating negative earnings growth for the second quarter, but the outlook also has swung into red numbers for the third quarter, according to the latest FactSet calculations.

The data firm now estimates that the third quarter outlook has changed from a slight gain of 0.2% as recently as June 7 to a slight decline of 0.3% as of late last week. Including the Q1 0.3% decline and an expected drop of 2.6% in Q2, that would mark the first three-quarter pullback in profits in three years, during the earnings recession from Q4 2015-Q2 2016.

The primary culprit for the downward trend has been weakness for multinational companies. FactSet recently estimated that companies that do more than half their business outside the U.S. likely will see an earnings decline of 9.3% in Q2. Those that do a majority of sales domestically were projected to see a 1.4% growth rate.

The lowered Q3 estimates are coming from sectors that have large international exposure — energy (-13% decline expected) and information technology (-9%). Tech is ranked first on the S&P 500 in international exposure while energy is fourth.

With FedEx and Micron both reporting results Tuesday, investors are increasingly cautious about putting capital to work. On Monday, a breakdown in the Dow Jones Transports (DJT) added more concern to the earnings season that lay ahead. The “trannies” divergence versus the S&P 500 is starting to become even more concerning.

Past sell offs have been accompanied with prior weakness in the DJT, as shown in the chart above. But using Dow Theory is very difficult in real time and usually a futile exercise as shown in the chart below.

Reverting to the theme of the week that is somewhat unfortunate, but consistent since 2018, geopolitical issues are leading to global weakness and a uniform approach to tackling the weakness by central banks. Despite what geopolitical skirmishes come to the forefront and persist, these manmade crises don’t generally cause great economic calamity and financial market disintegration. They can certainly disrupt growth in the global economy, with corporate earnings falling to one degree or another alongside equity prices, but they don’t generally disrupt financial conditions that support financial markets over time. And that’s what has brought central banks to a more uniform outlook for 2019 and 2020, as they aim to offset the geopolitical risks to the global economy. Here is what David Moenning of Sowell Management offers to investors when parsing the global slowdown with central bank activity.

“If traders have learned anything over the last decade, it is that when the world’s central bankers are all singing the same dovish song, the refrain for market participants becomes, “Happy days are here again.” I.E. Risk assets tend to rise and bond yields tend to fall as stocks discount better days ahead and bond traders fall all over themselves to buy bonds.

Rarely has the message from central bankers been so clear, or so universal. Which, of course, makes the appropriate trading decisions a bit simpler.”

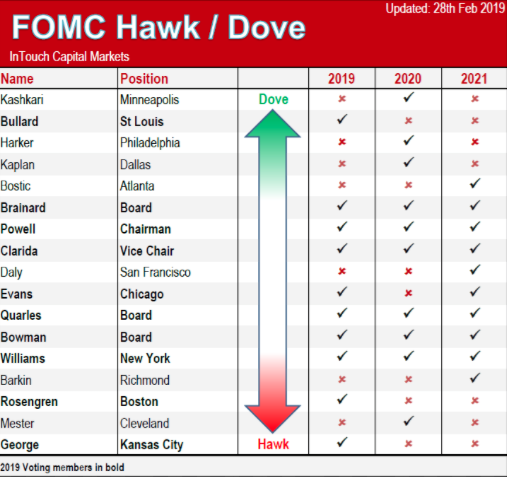

Speaking of central banks and Fed officials… It’s going to be a busy day of Fed speakers on Tuesday. All Fed speakers today are also voting members.

- 8:45 – Fed’s Williams speaks at Finance Forum

- 12:00 – Fed’s Bostic Speaks on Housing

- 13:00 – Powell Discusses Economic Outlook and Policy

- 15:30 – Fed’s Barkin Speaks in Ottawa

- 18:30 – Fed’s Bullard Speaks in St Louis

While certain Fed members have recently come out in favor of a rate cut, the speeches today will go a long way to reassuring the market that the FOMC pivot in favor of action near-term wasn’t just for show. It is increasingly important to market stability seeing how far in advance the market has priced in a Fed rate cut for the month of July. With that in mind, on Monday, Dallas Fed President Rob Kaplan on tried to slow down the rush to an interest-rate cut, saying he would take more time to watch developments before deciding to ease.

“I believe it would be wise to take additional time and allow events to unfold as we consider whether it is appropriate to make changes to the stance of U.S. monetary policy.”

As shown in the table above, Kaplan is not a voting member in 2019. Minnesota Federal Reserve President Neel Kashkari is not a voting member in 2019 either, but it didn’t stop him from putting pen to paper in offering the following:

“In the Federal Open Market Committee meeting that concluded on Wednesday of this week, I advocated for a 50-basis-point rate cut to 1.75 percent to 2.00 percent and a commitment not to raise rates again until core inflation reaches our 2 percent target on a sustained basis. I believe an aggressive policy action such as this is required to re-anchor inflation expectations at our target.

Since I became president of the Federal Reserve Bank of Minneapolis in January 2016, I have advocated against interest rate increases because I did not see sufficient evidence that inflationary pressures were building, and I believed there was still slack in the labor market. These views led me to formally dissent against rate increases in March, June, and December 2017. More recently, I supported the Committee’s decision in January 2019 to pause further rate increases.”

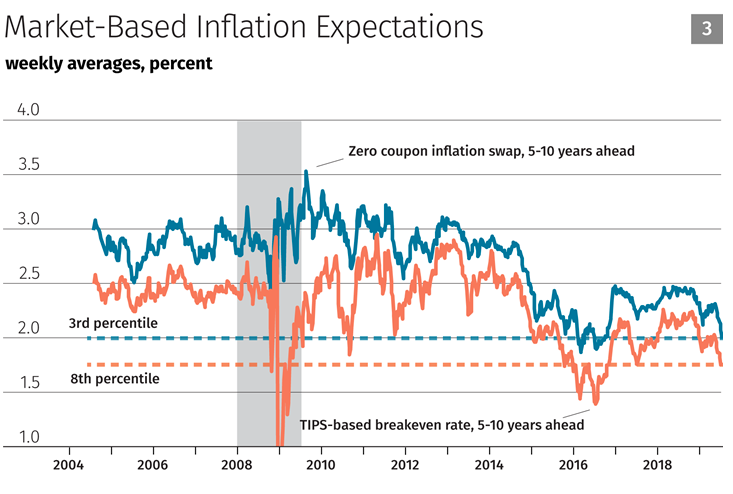

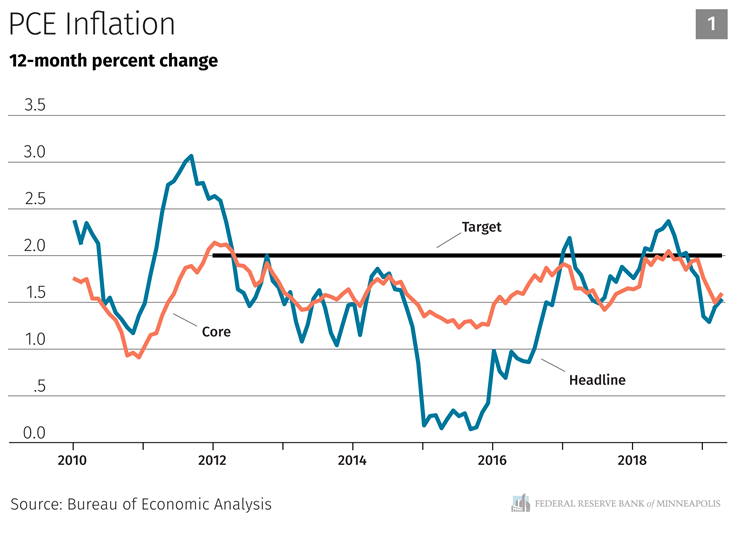

Chart 1 shows both headline and core inflation since 2010. One clearly sees that core inflation has repeatedly approached our 2 percent target only to fall back down. Currently, core inflation is at 1.6 percent year over year and headline is at 1.5 percent, having fallen over the past six months. It is certainly possible that temporary factors are holding inflation down. But we’ve been saying that for years. Looking at this chart, it is not surprising that long-run inflation expectations are below 2 percent, since we appear to never allow core inflation to climb above 2 percent, a point I expand on below.”

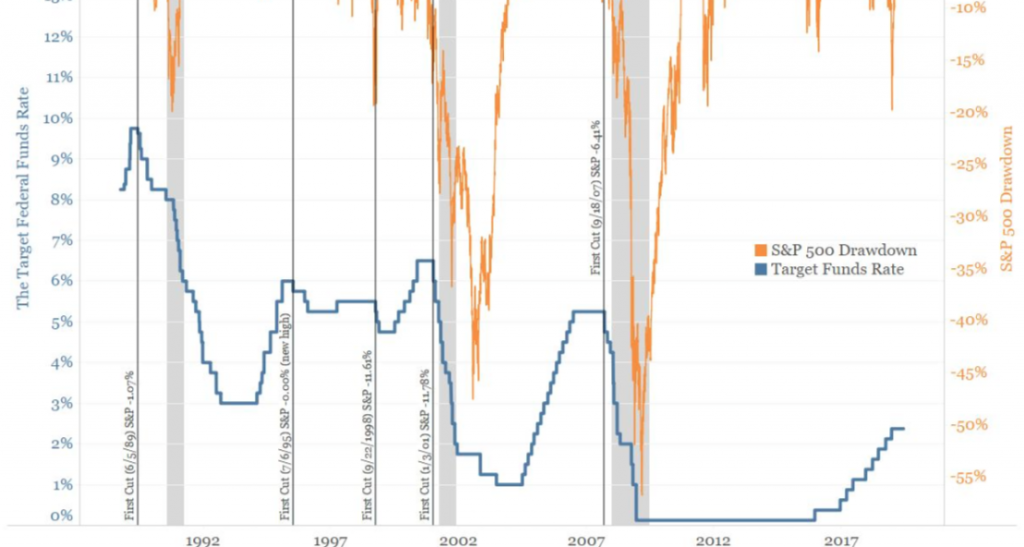

Will they or won’t they cut rates is going to be hotly contested, debated and found with uncertainty until the July FOMC meeting, but with respect to whether or not the Fed has cut previously, with the S&P 500 at all-time highs, it certainly has.

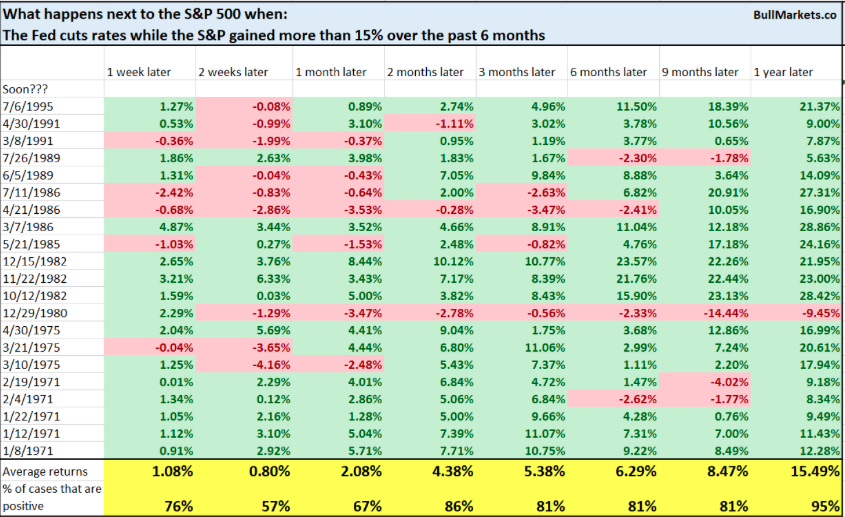

In 1995, the S&P 500 was at an all-time high when the Fed first cut rates. What this further identifies is that equity prices and market levels don’t play the role in Fed decision making and activity that the media would have one believe. The Fed’s dual mandate is the main consideration, as further evidenced in Kashhari’s chronicles. But what about the S&P 500 already being up so much in 2019, does that play a role in Fed rate decisions? Well, since 1975, there have been 26 times they cut rates with the S&P 500 YTD return >15 percent. A year later stocks were up 13.4% on average and higher 23 out of 26 times. It’s all about the economy and support the Fed’s dual mandate achievement.

Here’s every case in which the Fed cut rates while the S&P 500 rallied more than 15% over the past 6 months, and what the S&P 500 did next:

As David Moenning mentioned earlier, but to paraphrase more succinctly; don’t fight the Fed! And to some degree even if the situation worsens on the geopolitical front, central banks do not lack the appetite to support the economy should it worsen. The positive feedback loop from central bank to support the economy and asset prices is one that investors may be latching onto already. Recent investor repositioning/exposure and re-leveraging may be an early sign of not just moving in favor of the Fed, but also the hunt for yield.

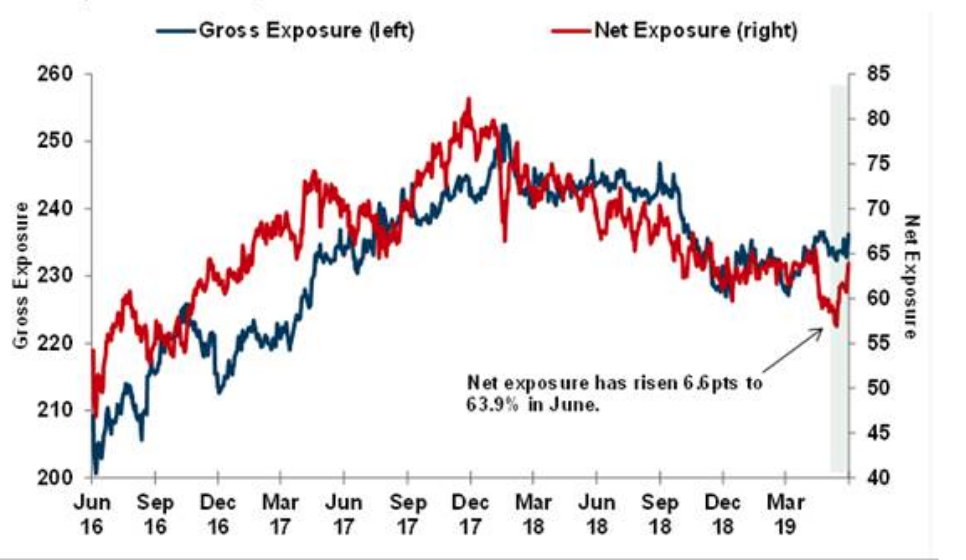

The latest positioning data from Goldman Sachs shows material re-risking as Net exposure sees largest weekly increase in 5 months. Net exposure began the month at 57.3%, the lowest level since Nov 2016, and has increased 6.6 points to 63.9 percent. The 6.6 point increase is on track to be the largest monthly increase in nets in three years.

{kind=link}