If you’re an investor or trader, you’ve probably heard the following words dozens of times: This time is different. While you may have heard these famous words, you may not know the full context for which they were originally offered by Sir John Templeton, who wrote “16 Rules for Investment Success” in 1993. The following is the most quoted passage from his works:

“The investor who says, ‘This time is different,’ when in fact it’s virtually a repeat of an earlier situation, has uttered among the four most costly words in the annals of investing.”

The reality is most market conditions and behaviors are ever different despite the disdain cast upon those who utter the words “this time is different”. This is because markets evolve, grow and adapt over time. Let’s look at some key facts about the composition of the equity markets.

- In 1957, the S&P 500 consisted of 425 industrial stocks, 60 utilities and 15 railroads. Financial stocks were not added to the index until the 1970s. Until 1988, the composition of the S&P 500 was 400 industrial stocks, 40 utilities, 40 financials and 20 transportation stocks.

- In 1902, America’s largest company, S. Steel, employed almost 170,000 people with sales of $561 million or $3,340 of sales per employee ($90,000 in today’s dollars). Today, Facebook generates $2 million in revenue per employee.

- Fifty years ago, retail investors accounted for more than 90% of all New York Stock Exchange trading volume. Today, professional investors perform 95% of trading.

- Before the Securities and Exchange Commission deregulated the brokerage industry on May Day in 1975 and abolished fixed-rate commissions, it was extremely cost-prohibitive to trade securities on the exchanges. Trading costs, including bid-ask spreads and commissions, have fallen on the order of 80%-90% since then.

- Mutual fund sales loads averaged 8%-10% in the 1950s.

- The first stock market index fund wasn’t created until 1976. The first bond index fund didn’t come around until late-1986.

- The 401(k) is roughly 30 years old. IRAs aren’t much older. The entire concept of retirement is largely a 20th-century phenomenon. In the past, people didn’t really save for retirement because the concept didn’t really exist until World War II. People typically worked until they died.

It’s different every time and as the markets evolve to fit societal evolution. New products are created, which in turn create new opportunities, advantages and disadvantages. There’s quite literally no time in the future that won’t be different. Having said that, historical context of the financial markets is critical to investor/trader success. Approaching investments and trades with the appropriate data, due diligence and general perspective are critical to returns on capital invested.

The reality of Sir John Templeton’s message was more about education than it was meant to breed contempt from those who fail to appreciate history. As such, here is the broader context of what Sir John Templeton wrote:

“The only way to avoid mistakes is not to invest — which is the biggest mistake of all. So forgive yourself for your errors. Don’t become discouraged, and certainly don’t try to recoup your losses by taking bigger risks. Instead, turn each mistake into a learning experience. Determine exactly what went wrong and how you can avoid the same mistake in the future.”

It’s really all about human psychology, which dictates human behaviors. Templeton was warning of human behaviors that often become habitual and lacking for corrective behaviors of what was learned.

The 2008 Financial Crisis was different and as such it demanded a different response from central bankers around the globe. Such actions have created an elongated global, economic recovery. In the United States, we have what has come to be the 2nd longest economic expansion in U.S. history. May marks the 107th month of the current expansion, surpassing the 106-month expansion of the 1960s. Most professional forecasters have become increasingly confident that the current expansion will set a longevity record by extending into the second half of 2019. Moreover, the 2nd longest expansionary cycle has also given rise to a bull market that is seemingly the most hated bull market in U.S. history for the reasons that created it, continue to support it and its’ general unique characteristics that some find unbelievable. Given the aforementioned, the only question the begs to be answered is, “When will this economic expansion end and a bear market begin?”

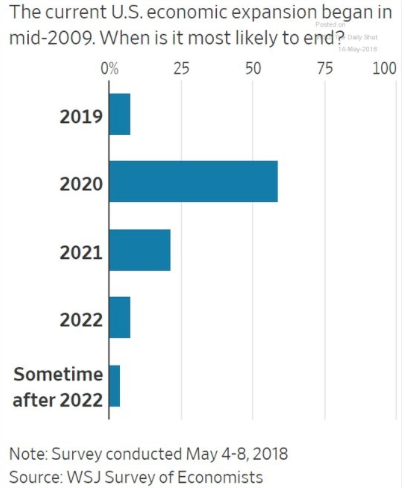

A recent Wall Street Journal survey polled economists in search of an answer to the aforementioned question about the economic expansion. Some 59% of private-sector economists surveyed said the expansion was most likely to end in 2020. In other words, the current economic cycle still has plenty of legs according to most economists.

So what might cause the end of the economic expansion? According to the Wall Street Journal survey, the most likely primary cause of the next downturn, 62% selected an overheating economy leading to Fed tightening. The Fed has almost always been blamed for ending economic expansionary cycles. It’s very contradictory to believe this theory about the Fed, seeing how the Fed typically is the respondent to the economy, not the underlying fundamentals of the U.S. economy. However, many will argue that since the Fed seemingly saved the U.S. economy through enacting Quantitative Easing in response to the Financial Crisis, it will be the undoing of the economy through its Quantitative Tightening practices that began in late 2015. It comes down to perspective and many have a different perspective of the Fed’s activity and its weighting in the current bull market, let alone economy.

The colloquialism, “Don’t fight the Fed”, has never been more evidenced than in the current market cycle. The colloquialism gives far too much credit to the Fed than is probably deserved and reinforces the theory of Fed induced bear markets.

When the economy is expanding/growing, corporate earnings grow and thus the stock market trends higher. These are known as the “fundamentals”. Before we talk a bit more about the fundamentals let’s now look briefly at another market investing colloquialism.

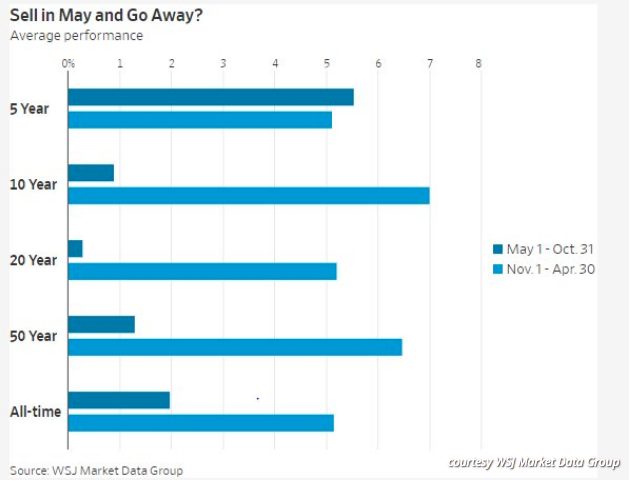

I know you’ve heard this one if you’re an investor/trader: Sell in May and go away. It’s not that May is always a bad month for the stock market, but rather historically it produces lesser market returns than most any other month. Because June is only slightly better than May for equity returns, it further supports the notion of another common phrase “the summer doldrums”. Per the Almanac, the Dow has seen a 0.02% average decline in May, while the S&P has seen an average rise of 0.2%, with the Nasdaq rising an average 0.9 percent.

What “sell in May and go away” really means is that the stretch between the start of May and the end of October has been a seasonally weak period for markets. While this has been true over the long term, as seen in the following table that looks at S&P 500 performance, the trend hasn’t held over the past five years, according to the WSJ Market Data Group.

As the economic cycle advances in age it tends to bring with it more market angst or volatility. We’ve seen that already in 2018. It also brings with it more top calling. “But the Fed is tightening, Household debt is at its highest levels in history and inflation is upon us”. Those bearish cries warrant greater perspective.

The Fed is inarguably tightening, but the Fed is tightening from historically low levels. More importantly, the Fed is tightening at an extremely slow pace, a pace that is unlikely to find itself with the ability to curb economic growth. The following chart demonstrates that the Fed is tightening monetary policy very slowly.

Of more recent significance, the Fed has stated that it will allow for inflation to run slightly above its 2% goal in the near term. The Fed’s recent statements concerning it’s rationalizing of inflation have thrown cold water on some bear market participants. It’s even gone so far as reducing expectations for a 4th rate hike in 2018 as measured by the CME’s FedWatch Tool. Prior to the Fed stating that it would allow for inflation to rise and stay above its 2% mandate for a brief period, Fed Fund futures were pricing in a nearly 45% chance of a December/4th rate hike. Since then, a December/4th rate hike has declined to a probability of less than 20 percent.

It’s of such great importance to investors that when they consider rising rates and bond yields, they consider levels and historical context. Prior to the 2008 Financial Crisis, the 10-yr. Treasury yield was in the 5% range. At present, the 10-yr. Treasury yield is barely 3 percent. So if an investor is bearish on the equity markets, wouldn’t there still be a significant amount of time needed to pass before yields and rates were impactful to the economy and corporate profits on the whole, assuming rates and yields are a primary causation for equity market declines?

Those whom are suggesting a bear market is imminent may simply be counting on this time being… the same, even as everything around us has changed. No matter where you look the majority of economists suggests that the current economic cycle is strong and gaining strength. The Fed can tighten, rates can rise from historically low levels, oil can rise and still be cheaper when adjusted for the same inflation that bears consider the “canary in the coal mine” and all the while equity markets can climb higher.

If there was one economist, just one that I was to rely on more than the masses and when it came to forecasting the economy, it would be Dr. Ed Yardeni. Dr. Yardeni is one of the most respected, popular and accurate forecasters of the modern U.S. economy. In his most recent blog post from Yardeni Research, he offered the following thoughts about the U.S. economy and potential for a recession:

“Since I don’t see a recession in the foreseeable future, I continue to focus on the forward P/E, which isn’t alarmingly high, in my opinion. The further out that a recession is perceived as likely to happen, the more sustainable are above-average P/Es. That’s because long expansions give investors the time to see earnings grow, as predicted by industry analysts.

I currently don’t expect a recession over the rest of this year or in 2019. What about 2020? Ask me again in 2019. As long as inflation remains subdued, as I expect, odds are that the expansion will go on and on—until further notice.”

We’ve mentioned a great many market colloquialisms in this research report. Most colloquialisms exist with misunderstandings as to their context or meaning and are thus responded to with error. Did you “sell in May and go away”. Maybe that will prove the right thing to do; we won’t know until we know. And remember, the context for that colloquialism resides in a more elongated period consisting of May through October. Anything can happen to the markets between now and then and what can happen may not even relate to the U.S. economy or corporate earnings. We saw that in Tuesday’s trading session as angst over Italy’s political strife took down global equity markets. Nonetheless and to recapture the overarching point of this latest research report from Finom Group, markets follow the economy over time because the economy produces earnings growth or earnings declines. For the foreseeable future, earnings are expected to grow. So if you are bearish on the markets, maybe you do have to believe that this time is different… and the market simply won’t follow the economy and corporate earnings growth. Colloquialisms can be confusing.

Tags: SPX VIX SPY DJIA IWM QQQ TLT

{kind=link}