While the U.S. Government is shutdown, corporate earnings will still continue to roll in as the tech sector begins reporting this week. Later in this report, we will discuss one of the most famed tech sector companies reporting on Monday after the closing bell, Netflix Incorporated.

Month-to-date through Jan. 18, 2018, the S&P 500 is outperforming the S&P 500 Bond Index by 3.8%, the most since Dec. 2016, when the monthly outperformance was 4.5%. The comparison between the stocks and bonds of the S&P 500 shows market sentiment by calculating the equity risk premium or discount as they are more commonly referred.

Through history, equity market discounts are observed before big stock market declines.

- In 1998, the S&P 500 Bonds outperformed the stocks in May before the S&P 500 top in June.

- Similarly in 2000, there was an equity risk discount in July before the August top.

- Again in July 2007 before the Oct top that year.

- Also this pattern was observed in March and April 2011, June and July of 2015 as well as in Sep. and Nov. that year.

The Real Estate, Telecommunications Services and Utilities are all expressing pessimism presently. Normally this wouldn’t be terribly concerning, but there is an identifiable and justifiable reasoning for the shift in the sentiment for these three sectors.

The benchmark U.S. 10-year Treasury yield rose to the highest level in more than three years, extending a selloff in the world’s largest-debt market that began in September of last year. The 10-year yield climbed to as high as 2.6567% Friday, a level unseen since September 2014.

Inflationary concerns are creeping into the U.S. economy as the Federal Reserve is set to enact at least 3 rate hikes in 2018. Additionally, a rally in oil prices to a three-year high has also boosted growth and inflation expectations.

But even with rising rates and inflationary concerns, the corporate earnings front has yielded greater returns from equity exposure as the major averages trend higher in the 1st three trading weeks of 2018. Noted below is the current estimate for Q4 2017 earnings and the projected earnings growth for Q1 2018.

Aggregate Estimates

- Fourth quarter earnings are expected to increase 4% from Q4 2016. Excluding the Energy sector, the earnings growth estimate declines to 9.9%.

- Fourth quarter revenue is expected to increase 1% from Q4 2016. Excluding the Energy sector, the revenue growth estimate declines to 5.9%.

- The forward four-quarter (1Q18 – 4Q18) P/E ratio for the S&P 500 is 18.4.

- During the week of Jan. 22, 83 S&P 500 companies are expected to report quarterly earnings.

Earnings season really heats up this week with major reports out of every sector. Netflix and Halliburton on January 22; Johnson & Johnson, Texas Instruments, Verizon, Procter & Gamble, United Continental, Capital One Financial and Kimberly-Clark on Jan 23. Ford, General Electric, Las Vegas Sands, Comcast, United Technologies on Jan. 24; Intel, Starbucks, Wynn Resorts and Western Digital on Jan. 25; Honeywell, AbbieVie and Colgate-Palmolive on Jan. 26.

The weekly economic data calendar is light in the beginning of the week and largely dependent on whether or not the government shutdown persists through the week’s end and when both GPD and Durable Goods Orders are expected to be released. If the government shutdown remains come Friday, GDP figures will not be released and delayed until further notice. A shutdown would cause statistic-keeping agencies to furlough most of their workers, stop collecting economic data and leave their work unfinished.

Most economists suggest that Wall Street won’t be troubled much due to the shutdown because the recently passed tax cuts are set to kick in next month, easily offsetting the damaged caused by the latest Washington angst and disorder. Having said that, past economic shutdowns didn’t coincide similarly frothy markets with recognizably stretched PE ratios.

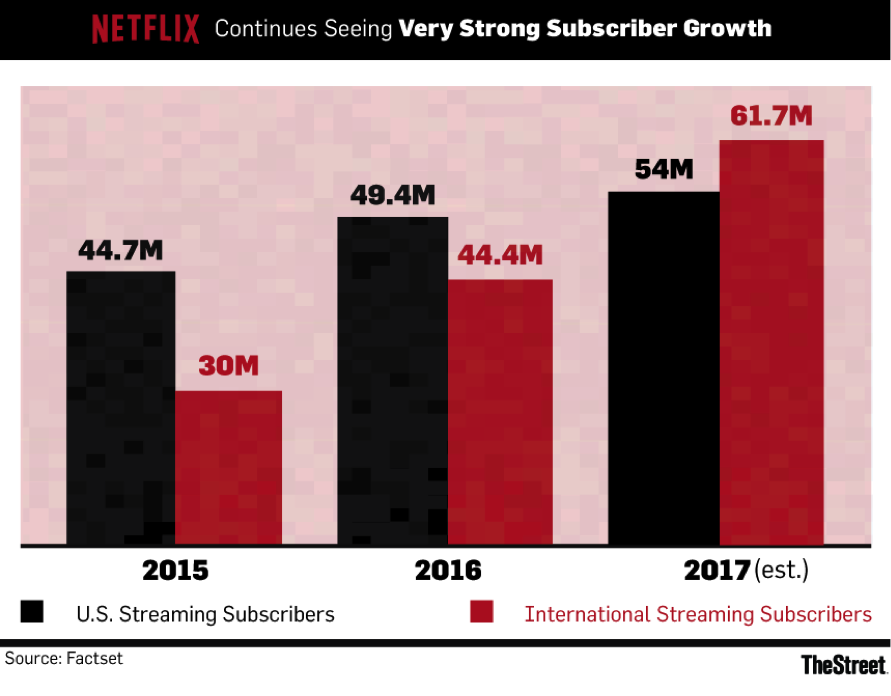

With the government shutdown more than likely persisting through the weekend and into the Jan 22nd trading week, investors should still monitor earnings reports. The first major tech sector & media report will come after the closing bell on Monday from Netflix Inc.

Analysts polled by FactSet expect Q4 revenue of $3.28 billion (up 32% annually) and GAAP EPS of $0.41. Those numbers roughly match Netflix’s own guidance. The revenue expectations would represent a 32% improvement compared with the same quarter a year ago, and up nearly 10% from the most recent quarter. Analysts’ revenue expectations break down to $1.62 billion from domestic streaming, $1.54 billion from international streaming, and $105 million from the company’s domestic DVD business. Netflix has missed FactSet’s consensus on revenue in six of the last 10 quarters. Analysts following the stock expect Netflix to report net additions of 1.27 million subscribers in the quarter.

That’s down from an estimated 1.35 million additions analysts were expecting at the end of October, but it’s slightly above the 1.25 million subscriber additions guidance from Netflix.

Tags: NFLX SPY QQQ

{kind=link}